Midas has recently announced contract after contract. In Table 1 below, it is especially evident that Midas is gaining traction (particularly from 23 Jun 2016 onwards) in winning orders, especially from its 32.5% stake in CRRC Nanjing Puzhen Rail Transport Co., Ltd. (“NPRT”).

However, investors do not seem to share this optimism as Midas has fallen approximately 12% from $0.260 on 23 Jun 2016 to $0.230 on 3 Feb 2017.

Table 1: Ernest’s compilation of contracts announced since 2015

|

Contracts clinched by Midas' Group |

|||

|

Date |

Midas/NPRT |

Amt (RMB m) |

Delivery |

|

Jan 3, 17 |

NPRT |

1,770 |

Jan 2018 - Nov 2019 |

|

Dec 1, 16 |

Midas |

232 |

2017 |

|

Nov 16, 16 |

NPRT |

2,590 |

Aug 2017 - Mar 2019 |

|

Aug 24, 16 |

Midas |

54 |

2016 - 2017 |

|

Jun 23, 16 |

NPRT |

3,300 |

2016 - 2019 |

|

Mar 17, 16 |

Midas |

248 |

2016 |

|

Jan 4, 16 |

NPRT |

1,280 |

2016 - 2017 |

|

Nov 23, 15 |

Midas |

73 |

2015 - 2016 |

|

Aug 24, 15 |

Midas |

67 |

2015 - 2016 |

|

Aug 18, 15 |

Midas |

95 |

2015 - 2016 |

|

Jun 15, 15 |

NPRT |

2,100 |

2016 - 2017 |

|

May 18, 15 |

Midas |

329 |

2015 |

|

Mar 3, 15 |

Midas |

366 |

2015 - 2020 |

|

Jan 29, 15 |

NPRT |

1,730 |

2016 - 2017 |

|

Total: 14,232 |

|||

Source: SGX; Ernest’s compilation

Patrick Chew, CEO of Midas Holdings. Is the market overly pessimistic on Midas?

Patrick Chew, CEO of Midas Holdings. Is the market overly pessimistic on Midas?

I was fortunate to meet Mr. Patrick Chew, Executive Director and Chief Executive Officer of Midas, and Mr. Liaw Kok Feng, Chief Finance Officer (collectively “Management”), on an exclusive basis, to understand more about Midas and its business prospects.

Below are some key points based on my findings. I have also drawn reference to analyst and industry reports and corroborated my findings with management.

Bright industry prospects

Spending on infrastructure, especially railway investments, continues unabated despite concerns on China’s economy and debt. At a press conference on 29 Dec 2016, China’s vice minister of transport, Yang Yudong, said China has budgeted RMB3.5t for railway construction from 2016 – 2020.

According to a Caixin article on 3 Jan 2017, China Railway Corp, China’s railway operator, plans to invest RMB800b in building railway infrastructure and purchasing trains and equipment in 2017. This underscores the bright industry prospects of Midas.

Earnings growth to continue

Earnings are likely to grow in FY16F and FY17F on several fronts, namely,

a) Contributions from Huicheng Group

Based on a DBS research note dated 18 Nov 2016, Huicheng contributed about 2 months of earnings to Midas in 3QFY16. It will contribute its full 3 months of earnings in 4QFY16F and 12 months in FY17F. Although Midas has not indicated the amount of contribution in 3QFY16, it is likely to be significant. We may be able to get more details in 4QFY16, especially if Huicheng manages to attain its “earn out target” by registering RMB80m in net profits for FY16F. (See SGX announcement HERE)

b) Potential synergistic benefits between Huicheng and Midas

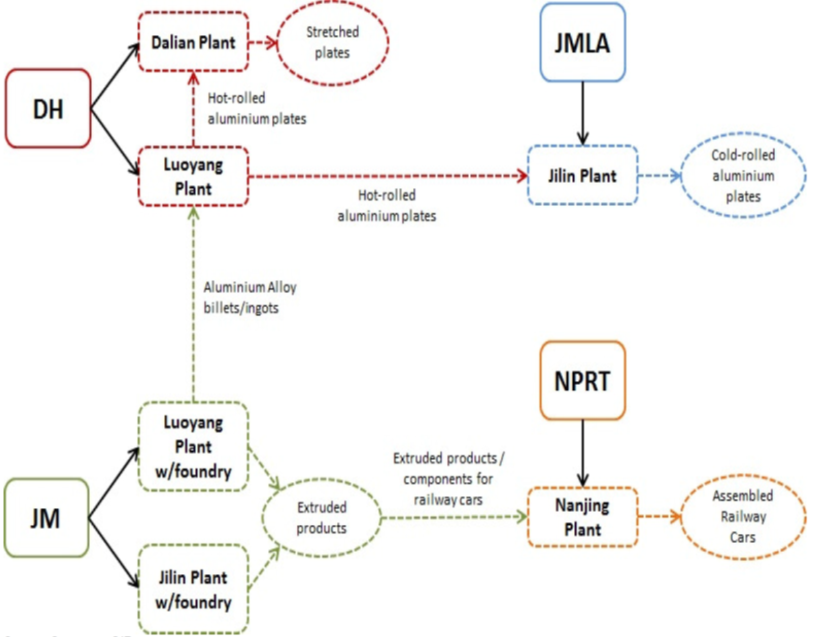

The acquisition of Huicheng brings synergistic benefits such as the hot rolled aluminium plates produced by Huicheng's Luoyang plant can be used by Midas’ Jilin plant, and the aluminium alloy billets / ingots produced by Midas' Luoyang plant can be used by Huicheng Luoyang. This allows Midas to better control its quality and cost of products. (See Figure 1 below)

Furthermore, besides expanding its range of products and services to include aluminium alloy stretched plates and hot rolled aluminium alloy plates and coils, Midas also expands its customer base and enters new industries and sectors such as aviation, aerospace, rail transportation, marine, automotive and petrochemical industries.

As the acquisition of Huicheng Group was completed on 27 Jul 2016, the potential synergistic benefits may be more apparent in FY17F and beyond.

Figure 1: Potential synergistic benefits between Huicheng and Midas

Source: Company, OCBC

c) Core aluminium extrusion segment to improve in FY17F

Midas’ aluminium alloy extrusion segment posted weaker results on slower project deliveries and on fewer high speed railway contracts. However, management believes that this segment is likely to improve in FY17 as they foresee that there are likely to be more high speed rail contracts in FY17.

d) Potential contribution from Aluminium Plates and Sheets

Midas’ aluminium plates and sheets segment is likely to commence commercial production in 1HFY17. According to management, there is some delay as management wants to be sure all the processes are running smoothly before they start production. Management mentioned that they have already lined up customers for this segment, thus it is likely to be a matter of time before this segment makes a positive contribution to Midas.

Low expectations provide room for upside surprise

At its closing price of $0.230 on 3 Feb 2017, Midas trades at 0.49x P/BV ratio. Midas has traded between 0.44x – 1.13x since 31 Jan 2012, with average P/BV ratio of 0.72x. It is reasonable to say that investors’ expectations for Midas are currently low which result in low valuations. This leaves room for potential upside surprise. A 0.72x P/BV translates to $0.343. Midas’ NAV / share is around $0.476.

Chart analysis

Based on Chart 1 below, Midas seems to be in a base formation with a potential inverted head and shoulder chart pattern since Sep 2016. 20D, 50D and 100D exponential moving averages (“EMA”) have turned higher with 20D forming golden crosses with 50D and 100D EMAs. Midas seems to be consolidating its recent gains around the neckline / support area of $0.225 – 0.230. Indicators such as OBV has been increasing steadily, signifying accumulation. Indicators such as RSI and MACD have exhibited bullish divergences during the formation of the potential inverted head and shoulders pattern. ADX closed at 21, amid positively placed directional indicators. A sustained break above $0.240 with volume expansion confirms the bullish inverted head and shoulder formation and points to an eventual measured technical target of around $0.275.

Near term supports: $0.230 / 0.225 / 0.220

Near term resistances: $0.240 / 0.245 / 0.250

Chart 1: Building a base formation

Source: Chartnexus as of 3 Feb 17

|

Risks

Below are some of the risks and it is not an exhaustive list.

Limited analyst coverage

During its heydays, Midas was covered by numerous local and foreign houses such as Merrill Lynch, Nomura, Credit Suisse etc. After years of share price underperformance, only DBS and OCBC actively cover the stock with target prices $0.380 and 0.250, respectively. It may take some time for other analysts to cover Midas as some of them are likely to wait for its commercial production in aluminium sheets and plates segment and the successful integration of Huicheng group.

Dependent on rail industry

Midas is dependent on the rail industry in China, especially the high-speed rail segment for its core aluminium extrusion segment. However, this segment registered fewer orders last year. Nevertheless, management is optimistic that this segment should see an improvement in orders in FY17F vis-à-vis FY16.

Execution risks

Midas acquired Huicheng on 27 Jul 2016 and it is commencing commercial production of its aluminium sheets and plates segment in 1HFY17. Management is cognizant of execution risks and intends to focus on their three business segments, thus they are unlikely to do any major merger and acquisitions in the near term.

Stretched balance sheet

Based on DBS research note, Midas’ gearing ratio is 0.9x as of FY15. DBS believes that the gearing should improve to 0.7x by FY17. Management is aware of this and plan to pare down the debt gradually. |

Ernest Lim, CFA, CA SingaporeConclusion

Ernest Lim, CFA, CA SingaporeConclusion

Midas seems to be an interesting company, underpinned by sanguine industry prospects, low valuations, potential earnings growth and potential bullish chart formation etc. Nevertheless, readers should be aware of the risks such as execution risks, dependence on railway industry, stretched balance sheet and limited analyst coverage. Readers can refer to Midas’ company website HERE for more information.

Disclaimer

Please refer to the disclaimer HERE

I consider that high for this stock, unless it can show earnings jump in near term.

EPS is a totally miserable 0.008. Midas' debt is massive. Are you willing to invest your own money in this counter? Do you analyse a stock based only on P/b ?