Republished with permission from ThumbTackInvestor

|

• Dutech Holdings Investing Thesis • Dutech Holdings – What’s Next? Realize $117k Profit, Hold Or Add More? (Part I) • Dutech Holdings – What Lies Ahead? Part III

For the uninitiated, a very quick summary. |

![]() When: 26 Apr 2018

When: 26 Apr 2018

Where: M Hotel Singapore

Anyway, here are my notes from the AGM. For the sake of brevity, I’d cut to the chase and just put everything down in point form.

- Turn around for their most recent acquisitions, Almex and Metric, is guided to be in 2018 or 2019.

Of course, I’d expect someone to ask about their M&A strategy. Dutech has very cleverly bought these businesses when they were failing and going into bankruptcy. Everyone wants to buy successful businesses but nobody’s selling a successful business for cheap.

The key question when buying failing businesses for a song then is…. “WHAT NEXT?”

I have full faith the integration is progressing nicely. Each piece of the business is complementary to the others.

Someone asked about the 7.9mil RMB impairment loss. Management’s answer is that the loss recorded is due to an impairment of Almex’s loss of a contract when they declared insolvency and Dutech bought them out. It is a valuation loss, not an actual operational loss. Management feels the impairment is reasonable and extraordinary.

- “Long tail” decline in ATM business

Johnny candidly stated his view is that the traditional ATM business is in a long term secular decline, dropping a bit every year. When pressed, he mentioned perhaps a 10% drop every year for the next decade.

But this doesn’t mean that there’s no money to be made in this sector anymore. ATMs will likely move from the traditional money dispensing functions into intelligent machines which can provide a variety of functions.

And this is a major reason for Dutech’s acquisitions. The acquisitions allow Dutech to move from being just involved in the assembly portion into a player along the entire value chain, from planning to assembly to even software management.

- Still on the acquisitions….

Johnny indicated that the acquisitions are to buy the customer base of Metric and Almex, as well as their know-how and intellectual property, patents etc. It is not based on the companies’ assets. (I’d add my own DD at the end later, so more on this later)

- Margins

Someone queried about Dutech’s declining margins. In FY17, Dutech’s margins for the High Security segment was affected by the drop in the USD vs SGD exchange, and the massive rise in steel prices. Dutech is trying to pass on some of the increased material costs to clients, but it takes some months for the variations in their contracts to materialize.

- Administrative costs

Johnny pointed out that the spike in administrative costs is due to the acquisitions. The core business of Dutech, less the acquisitions, has no change and in fact, a drop in administrative costs.

Also, because the acquisitions were completed in FY16Q3, from a y-o-y perspective, the administrative costs seem to have spiked up because the costs of the acquisitions have had only 3 months impact in FY16 but we see the full impact in FY17.

Management also guided that administrative costs will not increase any further in FY18, and that they’re working on cutting it.

(My own DD says that they’ve cut jobs by 25% at Almex and, at the same time, reassigning personnel within the subsidiaries.)

“Of the original 400 employees, Almex still has 120 employees – another 170 jobs have been retained at the British sister company.”

Source:

- Dividends

This question gets asked every year. Really.

Why does Dutech NOT pay a year-end dividend but only pays 1 after Q1?

This is because Dutech’s funds are in China. After the year-end closing of the books, and after auditors have gone through the accounts, they can then declare a dividend and move funds from China to SG. So it’s always just in time for an interim dividend after Q1, never after Q4. If the company is headquartered in SG and their funds are in SG, they’d be able to pay a year-end dividend.

- Cash buybacks, increase dividends

Seeing that the share price has declined substantially over the past 12 months, it’s inevitable that there’d be some disgruntled shareholders.

And there were.

1 shareholder pressed on (aggressively) about why the company doesn’t do share buybacks, giving data on its utilization of its cash holdings and the ROE to substantiate. Mr Graham Bell took the question, gave some background details on what the BOD deliberates when considering capital requirements. Personally (his view, not the BOD’s), is that the company needs to hold sufficient capital when dealing with turning around companies. In this aspect, it’s better to be conservative.

The company is in a period of change, as the High Security business of manufacturing safes is likely to be in a secular downtrend. The BOD has long identified that they need to move up the value chain, and hence, the timely acquisitions. All this would not be possible if they did not have adequate capital to capitalize on the bankruptcy of other companies.

There was a moment of awkwardness when Mr Bell took offence at a strong word the aggressive shareholder used to describe the board. Ah well, it’s all in a day’s work being on the BOD of a publicly listed company.

- Someone asked a question comparing the business dynamics of the Business Solutions segment vs the High Security segment

Business Solutions has not much bigger competition, unlike in the High Security segment. Also, for smaller sized orders, their competitors are either too slow to respond, or are unable to handle sudden orders due to various limitations. Johnny gave an example based on the manpower requirements. Some companies are unable to handle sudden changes in volume, as they would have to suddenly ramp up manpower to meet the demand, but when the project is over, they’d be stuck with excessive manpower.

Dutech has its own manufacturing facilities in China and hence, more control over production. On top of that, they do hire several contract staff.

(Can’t rem if he actually said this or is it from my own deduction, but in my notes, I wrote that their European competitors have stricter labour laws that make it difficult to hire contract staff in deals that make sense for the company)

- Large drop in margins in Business Solutions segment in Q4 of 2017

Quarterly, the margins in this segment range in the 20++ %. In Q4 of 2017, it dropped to 14% (or so), with the reason given as “a change in product mix”.

Johnny clarified that some projects utilize middlemen. If they manage to go to the end clients directly, the margins are higher. Longer term, they expect GPM of this segment to be 25-30% and NPM to be 8-12%, without the middlemen.

- General discussion on the company’s prospects

Johnny gave some color on what they’re working on and his experience in the industry.

Dutech is no longer a hardware company, neither are they just a mere safe manufacturer. All the talk about the society going cashless is missing the whole point.

Every human transaction, even without the use of actual cash, requires recording. Dutech’s business is the business of recording these transactions.

Johnny described Almex and Metric’s products, such as the validating machines and the SmartQube machines (not a spelling error ok!)

Also, their clients require the software to analyze commuter patterns for eg, and Dutech is able to provide these services. Johnny reiterated that the acquisitions are done with the IP and knowhow in mind, and these have morphed the company into a player along the whole chain.

Alright. Those are my notes from the AGM. The important ones at least.

There are several other questions that I don’t bother to type out here, as I think they are not very useful, and in fact, some are a bit…. hmmm….. uninformed. For eg, 1 not-so-happy shareholder asked why can’t the company write off the entire goodwill in the acquired Almex, instead of just writing down 7.9mil RMB related to the loss of the contract. Johnny replied that the write down is dependent on accounting rules, and verified by their auditors. (But of course.)

Now for TTI’s enlightenment.

I’ve really heard many folks think of Dutech as an “S-chip”. It’s not difficult to see why ppl think of that. Superficially, they do look like an S-chip. No real operations in SG, no office even, with management hailing from China, and manufacturing operations in China too.

But if Dutech is an S-chip, then so is Capitaland.

To illustrate this, perhaps I’d have to give a history lesson of sorts.

Dutech’s most recent acquisitions: Metric and Almex were bought at bankruptcy for a song. Prior to that, their predecessor is the famed Höft & Wessel, which is recognized as the leader in the field.

https://en.wikipedia.org/wiki/Hoeft_%26_Wessel_AG

Data on wikipedia is a bit outdated though, but u get the idea.

The business solutions segment of Dutech is where the focus is right now.

This table compiles the revenue and margins of the segments over the years:

|

REVENUE (RMB MILLION) |

||||||

|

YEAR |

HIGH SECURITY |

BUSINESS SOLUTIONS |

TOTAL |

|||

|

2013 |

968.1 |

59.5 |

1,027.6 |

|||

|

2014 |

859.6 |

191.3 |

1.050.9 |

|||

|

2015 |

821.3 |

32.1% |

372.4 |

21.0% |

1.193.7 |

28.6% |

|

2016 |

849.7 |

32.0% |

540.5 |

24.7% |

1,390.2 |

29.2% |

|

2017 |

795.4 |

28.8% |

861.1 |

21.8% |

1,656.5 |

25.2% |

The trend is obvious.

High Security revenue will continue to trend down, with declining margins.

Business Solutions’ revenue grew in 2017, but mostly from the acquisitions.

Going forward, it’s obvious that BS will increasingly form the core of the company’s business, specifically its operations in Europe.

Johnny wasn’t kidding when he said that BS has less real competition. The only real major competitor that Dutech faces in this segment is Scheidt & Bachmann.

https://www.scheidt-bachmann.de/en/

They’re the number 1 player in the ticketing and parking machines sector, followed closely by the integrated Dutech, in terms of market share.

Unfortunately, since they’re privately held, there’s no published financials for me to do a comparison. That’d be so nice. And in fact, I think if their financials are public, it’d immediately correct what I think is the mispricing of Dutech currently, since everyone can do a simple comparison of their financials.

The other smaller competitors include Parkeon Transportation, VIX technology and Ridango, none of which is listed. In fact, I can’t find any single player in this field that’s listed. (Anyone who knows, pls kindly let me know!)

So how large is the European market currently?

The Europe smart ticketing market revenue is estimated to be $1.74 billion in 2017 and is expected to reach $5.38 billion by 2023, growing at a CAGR of 20.69% during the forecast period 2017-2023.

In this growing market, the players are mostly still smaller, fragmented outfits, fighting for market share. By buying Almex, Dutech already has direct access to certain major clients that otherwise, would never consider Dutech.

For example, in end 2017, Dutech won a contract with the all-important Deutsche Bahn (DB), to redesign DB’s software for all ticketing machines to make them more flexible in integrating with all future hardware modules:

(DB Vertrieb is a wholly owned subsidiary of DB)

This project has just begun, and is slated to last until the beginning of 2019.

But it’s just upgrading the software to provide more flexibility right? No mention of contract value too, doesn’t sound like a big project?

“The new DB machine platform will be used on all DB existing vending machines as well as on new video machines, which ALMEX GmbH will also supply to DB Vertrieb for a first project next year.”

Now, DB is a helluva important client. If Almex is winning contracts to supply new ticketing and validation machines, it’s certainly very good news, and they’re likely winning market share.

(Travellers who have used Europe’s train system will understand that in Europe, you can buy a ticket, but you need to validate it to prove that it’s being used during that certain time period. So every station has multiple validating machines along the platform)

In fact, Almex already has a long term working relationship with DB, and this relationship is set to deepen as DB continues to refresh their equipment, and ticketing solutions.

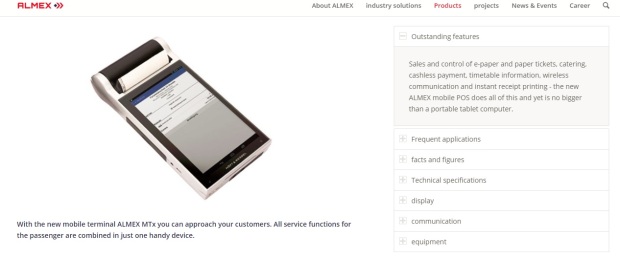

For example, currently, DB’s train attendants utilize handheld mobile devices for ticketing, and guess who supplies these devices for DB?

Hmm... look at the picture of the mobile ticketing device from DB.

Yup, that’s in Almex’s product catalog:

Aside from ticketing and car parking solutions, both the hardware and software side, Dutech also supplies inventory management solutions, through skyeye.com, for logistics companies. (Again, both hardware and software)

I guess this would be self explanatory:

|

TTI’s Thoughts Actually, currently, I don’t think Dutech currently has any real, indisputable economic moat so it isn’t a Buffett type of company. But I do think the business is currently completely misunderstood by the market, and hence, completely mispriced. |