Republished from ThumbtackInvestor's blog with permission. ThumbtackInvestor, a Singaporean in his mid-30s, whose portfolio is valued at just over S$1 million, holds 630,000 shares of Dutech Holdings.

|

This is a continuation of the earlier posts: Dutech Holdings – What’s Next? Realize $117k Profit, Hold Or Add More? (Part I) In Part III, I will be sharing mainly on what are the happenings in the industry that would affect Dutech Holdings’ immediate – mid term prospects, as well as some of the potential risks/headwinds that the company may face. (Yes, every investment must be prospective. Only focusing on the good news and ignoring the potentially bad news, reminds me of the old radio advertisement “Hear only the good stuff”) As with all trilogies, the best part is always the last installment… Most of this stuff is new, as in I don’t think anybody has noticed or discussed it in detail, particularly in relation to Dutech’s prospects. Yet, if anything at all, this post is going to illustrate the major catalysts for Dutech going forward. It is, IMHO, revolutionary and illuminating. Do tell me if you agree or disagree after reading. |

Merger Of Diebold And Wincor

In late Nov, Diebold and Wincor Nixdorf, the 2nd and 3rd largest safe manufacturers globally, combined in a $1.8-billion deal to form the largest player in the industry.

Prior to the merger, Dutech supplied >50% of the safe orders from Diebold and Wincor. Hence, this merger is of great significance to Dutech.

The merger has many synergies, the most obvious of which is geographical. Diebold dominates the US markets, while Wincor dominates the European markets. Post-merger, Diebold Nixdorf will have a 35% share of the global ATM market, while what used to be the largest player, NCR Corporation, will now have around 25% of the market.

Since Diebold and Wincor are 2 major clients of Dutech, I thought it’d be good to understand more about their merger, the happenings of the company and what the future plans are post-merger.

Global Move Away From Hardware Towards Software And Services

Following the merger, Diebold Nixdorf has indicated that the company’s future direction would be towards providing the software and services, with less emphasis on the actual hardware.

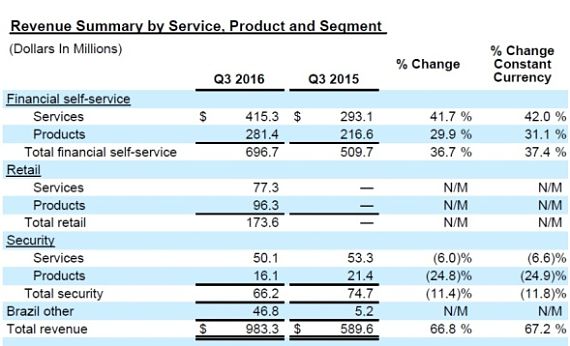

This is reflected in their financials as well:

Here are Diebold Nixdorf’s latest financials. As we can see, under the financial self-service division, revenue from services has risen 41.7%, far exceeding the growth in products. The company has also recently announced new service contracts with several major banks in US to provide servicing and maintenance for their ATMs, including many ATMs that were not manufactured or installed by Diebold Nixdorf.

The retail division is something new, following the merger. Diebold Nixdorf now works with retail businesses to provide information machines in malls that enhance the retail experience.

This push into software related businesses is, on a net basis, good for Dutech as this means that Diebold Nixdorf will increasingly rely on Dutech to work on the hardware part.

Dutech’s low cost and efficient manufacturing facilities in China will thus likely be kept even more busy as Diebold Nixdorf subcontracts out more of the hardware manufacturing parts to them.

With Dutech being the main supplier for both Diebold and Wincor before their merger, it is highly likely that as the new company sub-cons out the hardware manufacturing part, Dutech will be the 1st in line to win new contracts.

Afterall, there are currently no other large players with Dutech’s UEL and UN certification, as well as Dutech’s low cost production facilities situated in China.

Increasingly, Diebold Nixdorf will focus more on the software that goes into operating the ATMs. This article describes how the company intends to make ATMs even more “high tech”. Expect retinal scans and smartphones linked ATMs in future.

https://www.ft.com/content/621f0f12-f738-11e5-803c-d27c7117d132

As retail space gets more expensive and valuable, Diebold Nixdorf is also focusing on making the actual ATMs or retail information machines smaller and smaller.

NCR Corporation was the largest player in the ATM space prior to the merger of Diebold and Wincor, and post merger, they are now the 2nd largest globally.

A quick look at NCR Corporation’s results tells me that they too, are focusing on services and software, with less emphasis on hardware.

Why are they all moving towards software?

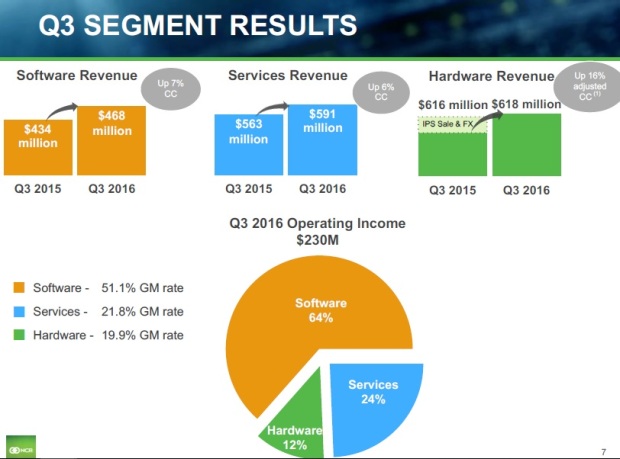

A slide in NCR Corporation’s latest FS tells us the answer:

As we can see, the software division has a 51.1% (what!!) GM rate, followed by services with 21.8%, and finally hardware with 19.9%.

Consequently, software accounts for 64% of NCR Corp’s Q3 2016 Operating Income.

Dutech seems to have taken a leaf out of their playbook, and is growing in the same segment as well.

We can see revenue from the “High Security” segment falling gradually, while the revenue from the “Business Solutions” has grown >6 times in the past 3 years.

Their recent acquisition, Metric, will contribute further to the “Business Solutions” division via the Metric UK branch, which supplies and maintains carpark ticketing and management systems.

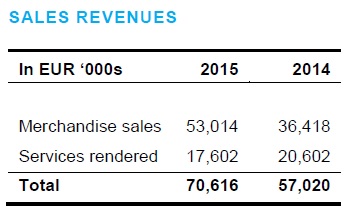

I’ve previously in Part II, spoken fondly of the services aspect of Metric UK. This is taken from Metric Group AR15, page 106:

Of total income generated on the performance of services, the UK subgroup earned a share of EUR 12,392 k (previous year: EUR 10,623 k). Essentially, this comprises repairs and maintenance work on car park ticketing terminals. Of total income generated on the performance of services, the UK subgroup earned a share of EUR 12,392 k (previous year: EUR 10,623 k). Essentially, this comprises repairs and maintenance work on car park ticketing terminals. |

Despite revenue from services rendered for the entire group dropping from 2014 to 2015, Metric UK’s share of revenue under services rendered rose from EUR 10.6mil to EUR 12.4mil.

If Dutech can successfuly win more contracts, the benefits are magnified as they take care of the entire value chain for their clients: from manufacturing of the ticketing machines, to the software that controls the ticketing machines to the maintenance contracts, which provide a nice recurring income.

Currently, Dutech’s “High Security” segment still has higher margins than their “Business Solutions” segment, but a large reason for that is the depressed domestic coiled steel prices. I’m expecting Dutech’s overall margins to come down from these lofty levels, particularly so in the “High Security” segment such that “Business Solutions” will eventually enjoy higher margins than the “High Security” segment.

Death Of Cash?

The other concern that some readers have brought up to me is that the world seems to be going cashless. The newer generation seems to prefer credit and other cashless way of making transactions. Will this mean that ATMs will become obsolete in the future?

I don’t think so.

There may be, probably will be in fact, reduced usage of cash in transactions, but ATMs will always be around. I’m guess they’ll evolve to be points of transactions and not just merely for cash related transactions.

It’s kinda like how they said that the dawn of the internet era would put retailers out of business, and that all businesses in future will be conducted online. Since then, sure some retailers are badly affected, but many have continued to succeed. Bricks and mortar malls continue to pop up.

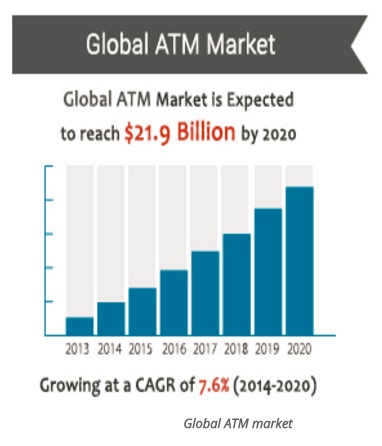

So contrary to such opinion, I think the global ATM market will continue to expand, particularly in some of the less developed countries.

This study agrees with me.

http://www.paymentscardsandmobile.com/atm-market-expected-to-reach-21-9-billion-by-2020/

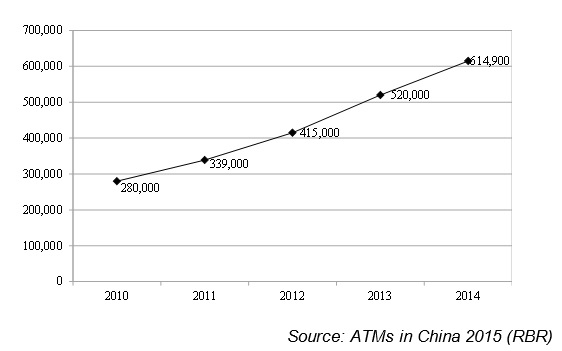

China, which is one of the fastest growing markets for ATM penetration, has seen a rapid increase in installed ATMs:

Large, New Order Contracts For Dutech Soon

OK, this is where it gets exciting for Dutech’s shareholders. There have been some of you who have indicated you’re worried about Dutech’s declining “High Security” revenue.

So was I. “was”.

So I did what I do when I’m worried: I start digging deeper. Otherwise I can’t sleep.

Aside from the fact that it is part of Dutech’s plans to focus on the “Business Solutions”, which by itself is an important point, I am also highly confident that Dutech will soon see new, large orders for ATMs and safes, now that the Diebold and Wincor merger is completed. (well, it's not 100% completed because I think there’s still some anti-trust issues to be cleared, but it’s pretty much taken as it is)

Skeptical? Don’t take it from TTI, take it from Diebold Nixdorf’s CEO himself.

This is his response to an analyst’s question during 3Q16 earnings call:

And I quote:

“….. customers were holding off just to make sure that they have a full appreciation of who is their account manager and who they are dealing with…”

“And you can see that a lot of that will come through as orders in Q4 and Q1….”

“…. product side alone, we are currently sitting on a backlog that is substantially north of $1 billion…”

“… I believe that the regional banks in the US will join the party towards the end of 2017, going into 2018…”

Note that this is in his response to a specific question about the ATM business.

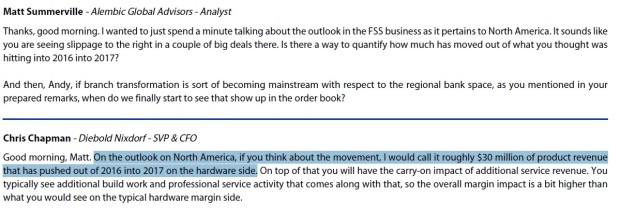

How about this other reply from the CFO, also in relation to the most recent earnings call:

“… I would call it roughly $30 million of product revenue that has pushed out of 2016 into 2017 on the hardware side“

“… I would call it roughly $30 million of product revenue that has pushed out of 2016 into 2017 on the hardware side“

Note that this is in response to the North America business only, which is the largest revenue contributor as of 9M16, contributing about 40% of total revenues.

Europe, Middle East and Africa is the next largest component of revenues as of 9M16, accounting for 27%, Latin America accounted for approximately 18%, and Asia Pacific (which includes China), accounted for 15%.

New Orders For NuVinci CVP Transmissions & Further Investments In R&D

Dutech is currently in the midst of securing new orders for manufacturing NuVinci CVP transmissions. The manufacturing is done for Fallbrook Technologies, and the client is reportedly a major European automobile company.

This is what the technology is about, roughly:

http://www.fallbrooktech.com/nuvinci-technology

Dutech’s collaboration with Fallbrook goes back to 2010, when Fallbrook chose Dutech as it’s manufacturer for this transmissions:

These niche areas provide Dutech with a know-how competitive moat. It is unlikely that lesser manufacturers in China without the engineering know-how can dislodge Dutech. Without the know-how, Dutech’s Chinese peers can only compete on price, which is moot as Dutech enjoys the same conditions as them.

And the company is not resting on its laurels. Dutech continues to invest heavily in R&D to be at the forefront of new technologies. Aside from investing in R&D, Dutech has shown that they’re willing to use their cashflows to buy patents that have potential.

This link shows their application to construct a new R&D facility:

(credit to wangnx in Investing Note for bringing this to my attention)

The facility is situated in the proximity of Dutech’s existing 2 production plants, just outside of Shanghai.

Risks

I’m not oblivious to potential headwinds that Dutech may encounter. Thus far, there are almost zero instances where the outlook for a company that I have analyzed is so rosy that I can’t find any potential headwinds.

Life always prepares some curve balls around the corner for us.

Some of the more obvious ones have already been described in CIMB’s report, so I’ll just mention them in passing.

Forex is potentially a headache for Dutech, although the consensus currently is that it’ll be favorable. A strong USD and weak RMB is beneficial to Dutech, as it’s revenues are collected in USD while production costs are in RMB.

We all know Trump’s threat to label China as a currency manipulator. Trump wants a stronger RMB. I am not sure if he’d be successful. I don’t think the Chinese really allow any outsider to dictate what they want to do with the RMB. But it’s still a potential threat to note. If RMB appreciates substantially against the USD, that’d be a drag on earnings for Dutech.

On top of that, with their recent acquisition, the company will have increased exposure to the pound and euros, although I suspect the impact is still likely to be very minimal.

The other potential risk that’s been mentioned is the rising domestic rolled steel coil prices, which is a major component cost in the manufacturing of Dutech’s products.

As we can see above, particularly in 4Q16, China’s domestic hot rolled coil steel price has been on a tear and, as of the time of writing, is still rising. Since steel is a major cost component for Dutech, Dutech’s margins for the safes and ATMs will likely come under pressure.

On a bigger picture though, China’s coil steel price is still relatively moderate when you look at the multi-year data. I can see how forward quarters in 2017 will show stagnant or reduced GPMs due to this, though.

I don’t know if the company hedges its steel purchases. Someone on Investing Note told me that they do, but there’s no data that I can find. The company doesn’t announce its hedging strategies, if any, in the AR either. And that someone who told me couldn’t substantiate it either, except to say that he read it somewhere.

So I’ll just assess their material costs at spot prices. Anyway, all these prices, even if they are hedged, eventually flow down to their costs so for a long term investor, it doesn’t really matter.

What I will spend more time discussing here, and this is something that hasn’t been brought up thus far, is the negative impact of China as a risk factor.

Negative Impact Of China’s Regulations On Global ATM Manufacturers

In 2016, China introduced new regulations that prohibit foreign ATM vendors from operating in the country, unless it’s done in collaboration with a domestic partner.

Yup, essentially the Chinese government supported domestic ATM vendors by putting insurmountable obstacles to foreign vendors.

This is taken from one of the articles I found regarding the regulations:

New state guidelines influence deployer choices

Domestic suppliers also had a strong year in the wake of guidance from the China Banking Regulatory Commission (CBRC) regarding “controllable IT”. Controllable IT means that a machine’s parts must be manufactured in China and data must be contained within the country at all times. The 2014 guidelines state that banks should increase the share of “controllable” IT equipment by at least 15% annually from 2015, to account for at least 75% of all IT equipment by 2019.

Gotta love the euphemism: “guidelines”

All these had a substantial impact on all the major ATM vendors: Diebold, Wincor and NCR Corporation.

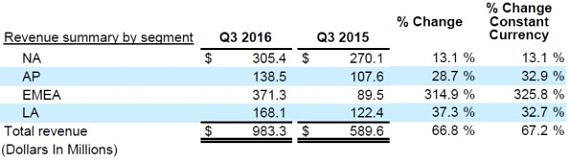

This is taken from Diebold Nixdorf (the merged entity)’s latest 3Q16 results:

As we can see, growth in revenue in Asia Pacific is 28.7%, which looks like it’s not too bad, but it’s a substantial drop from previously. Previously, AP used to be the largest growth centre, with China showing the most rapid growth in ATM penetration.

Figures from the People’s Bank of China show a total of 866,700 ATMs online in 2015, up 41 percent from 2014. Since 2013, China has claimed first place as the world’s largest market for payment cards and ATMs, according to People’s Bank data.

Market share of the global ATM manufacturers in the China market was growing at a health clip as well before these new regulations halted their growth. In fact, they were all in the top 5 vendor list except in 2015 and 2016, when these new regulations came into play.

I’ll digress a bit. China is behaving like a big bully these days. Am I the only one who can see that in the various business I have analyzed that have exposure to China? They can terrex anything they like, ignore international court rulings on the South China Sea and whatever obligations they may have signed with WTO regarding free markets.

This move sure doesn’t look like a free market move to me.

The top vendors in terms of market share in China as of 2015 are:

- GRGBanking (27.85 percent);

- Hitachi (13.35 percent);

- Cashway (11.49 percent);

- King Teller (10.94 percent); and

- Yihua (10.82 percent)

I found out about these new regulations as I was looking at China as one of the growth areas, and this pie chart just didn’t make sense to me.

You’re telling me that Diebold, Wincor and NCR, the global leading players who have a relatively large portion of their profits put into R&D annually, with their experience and know how, can only garner 3.65%, 1.91% and 1.99% of China’s domestic market?!

It’s essentially an uneven playing field.

GRGBanking is the dominant player with 27.85%. So I dug deeper. Who exactly is GRGBanking?

From wikipedia:“GRG Banking is a Chinese listed state-owned enterprise, specialized in the financial self-service industry. GRG Banking is engaged in R&D, manufacturing, sales and service, software development for ATMs, AFCs and other currency recognition and processing equipment.”

State-owned enterprise. Right. No wonder. Talk about an uneven playing field.

It’s like a Man U vs Liverpool match… where the referee and linesmen are all Man U diehard fans.

BTW, since I’ve compared Dutech’s valuations to Gunnebo’s in Part I, I thought it’d be interesting to take a look at GRGBanking’s as well.

GRGBanking: PER (on 3rd Jan 2017) is 21.11, it’s P/B is 6.16 times.

Here’s the FSs to substantiate the figures above:

Crazily high valuations compared to Dutech’s. And they may have the Chinese government’s backing, but it’s hard to see how they can succeed outside of China whereas Dutech has a fast growing global footprint, with valuations that’s a fraction of the above figures. (P/B is 6.16x !)

Anyway, in response to these Chinese regulations, the global players started forming joint ventures with local Chinese companies so that they can continue to expand in China. These global players take a minority stake in a JV, hence putting the control of the JV in the hands of their Chinese counterparts.

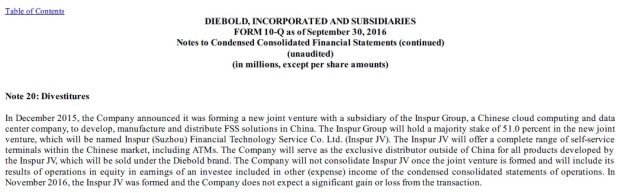

Diebold formed a JV with Chinese tech company Inspur Group:

Wincor formed a JV with Aisino Corporation:

http://www.wincor-nixdorf.com/internet/EN/WincorNixdorf/Press/pressreleases/2016/aisinoen.html

This means that the merged entity Diebold Nixdorf, now has 2 JVs with 2 separate Chinese groups, in both of which they are the minority shareholder.

This sucks for Dutech, as it means that at least with respect to China, Diebold Nixdorf will have to send manufacturing orders to their respective JVs and not utilize Dutech.

From what I’ve read about the details and structure of the JVs, and trust me I have read it all, it basically confirms to me that Dutech will not be seeing new orders from Diebold Nixdorf’s expansion in China.

Digging deeper, this basically confirms my suspicions:

This does not mean that I’m expecting Dutech’s China business to decline. It means that Dutech will not win NEW orders in relation to the growth of Diebold Nixdorf’s ATMs in China.

Most of Dutech’s current sales in China are done in the Free Trade Zone, and the bulk of these are exported eventually anyway.

So in this regard, I’m not predicting a Chinese headwind. I’m predicting the absence of a Chinese tailwind.

|

CONCLUSION I intend for Dutech to be a long term core holding, and am not expecting to divest anything anytime soon. |