This article was first published on http://value-edge.com/ and is reproduced with permission.

Sinwa Limited, with a history dating back to the 1960s, is Asia Pacific’s leading marine, offshore supply and logistics company servicing the marine and offshore industry in Singapore, China and Australia. With a network spanning 12 major locations and delivering premium service to more than 100 key ports, it operates on a motto of ‘Right On Time, At Any Time’. It is this solid reputation for reliability that 90% of its revenue is repeat business.

Fundamental Analysis:

(I) Earnings:

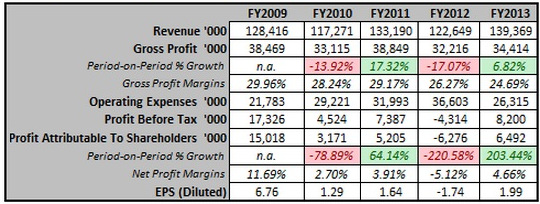

While gross profit margins have remained roughly constant over the years – within a band of 25% to 30% -- we can see that the growth in gross profits has fluctuated greatly.

Furthermore, its net profit margin (NPM) has been declining since 2009 and even entering the negative region in 2012. We only see an improvement in the margins from FY2012 to FY2013.

In this industry, one thing we have to understand is, chartering is a high margin business while supply is a low margin business. The high NPM in FY2009 is explained by the business split mainly into chartering and supply.

The decline is due to the company starting to deviate away from the chartering business and into engineering. As the company continued to reduce its chartering business and increase its engineering business, we observe the company’s profits being affected greatly as engineering was never its expertise.

However, in FY2013, we see a recovery due to the CEO changing the direction of the company by divesting all non-core businesses and focusing on the core business which is supply.

This also explains the lower margins comparing 2009 and 2013, despite most of the non-core businesses being divested in FY2013.

It is my belief that 4.66% is not the normalized NPM level yet as we see margins in the latest quarterly results being approximately 10%, of which approximately 2% is attributable to the sale of the tugboat.

Also, after talking to their IR, it is difficult to ascertain the industry’s average for NPM as most competitors are small and non-listed players.

Moreover, Sinwa being a market leader in Singapore is well-armed with robust infrastructure. As such, it is able to operate with higher efficiency (cost savings) as well as the ability to order in larger bulk (lower cost price from suppliers).

This allows Sinwa to enjoy higher margins.

Lastly, we see that EPS has been increasing, where EPS in the latest quarter alone was 1.12 cents. However, we have to bear in mind that it was partly due to the sale of the tugboat.

Going forward, we should also expect another one-off improvement in margins and EPS after the settlement of the dispute over the Nordic Vessel.

(II) Balance Sheet & Cash Flows:

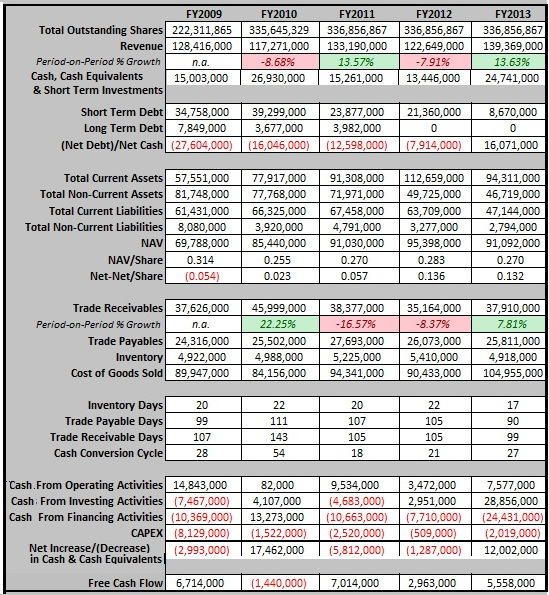

What started out as a net debt company, the new CEO has been able to turn this around and in FY2013 the company was in net cash.

Furthermore, it has been reducing debt every year; it has effectively paid off its long term debt.

While NAV has decreased, this is not a cause of for concern as it is mainly due to management divesting away its non-core business; hence, a decrease in NAV is not surprising.

Furthermore, the company’s cash conversion cycle has always been positive, which is another positive sign. That said, Sinwa’s customers are mainly reputable customers such as Sodexo and BP, further decreasing concerns of clients not paying on time, or the need to write off bad debts. Furthermore, given how the business operates on repeat customers, on the perspective of their customers, it would be ideal for them to build up a good working relationship with Sinwa too.

Looking at the company’s cash flows, we can see cash decreasing for several years, attributable to the non-core business burning cash. However, with the change in the company’s direction, we see cash levels increasing in FY2013 and a positive Free Cash Flow (FCF). In the latest quarterly results, cash levels have increased by approximately SGD8million. However, the increase is attributable to one-off gains from the disposals of assets from the non-core business.

(III) Financial Ratios:

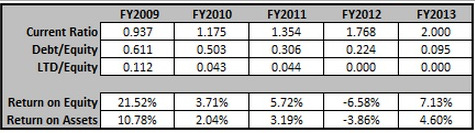

Increasing Current Ratios, decreasing Debt/Equity and LTD/Equity reaching 0 are all positive signs. Furthermore, Return on Equity and Assets has been improving, but once again we have to understand the difference between FY2009 and FY2013 is due to the change in business as explained before.

Qualitative Analysis:

(I) Understanding the Industry: Bruce Rann, CEO of Sinwa. NextInsight file photoWithin the ship chandling industry, there are 5 major players that dominate approximately 65% of the Asia Pacific market, with Sinwa being the largest. The other 4 are Fuji Trading, Wrist, HMS Group and EMS Seven Seas. Within this industry in Singapore, we can observe consolidation of market share by the bigger players as vessel owners prefer working with the bigger companies.

Bruce Rann, CEO of Sinwa. NextInsight file photoWithin the ship chandling industry, there are 5 major players that dominate approximately 65% of the Asia Pacific market, with Sinwa being the largest. The other 4 are Fuji Trading, Wrist, HMS Group and EMS Seven Seas. Within this industry in Singapore, we can observe consolidation of market share by the bigger players as vessel owners prefer working with the bigger companies.

With regards to the nature of this industry, it requires companies like Sinwa to be ready at any point in time. To quote Bruce Rann, “As a case in point, just last week, one of Sinwa’s largest clients placed an order worth SGD185,000 and wanted it by 10am the following day. Sinwa filled the order on time”. Evidently, we can see the competitive nature of this industry, where new and smaller entrants would definitely find it difficult to compete with these larger players.

(II) Key Elements in their Supply Business:

Their clients want guaranteed, timely, and quality supplies and services, which Sinwa is able to provide. This is evident from 90% of their revenue being made up of repeat businesses. Furthermore, their No. 1 client, Sodexo, is a global company and is thelargest catering company in the world. As Sodexo continues to grow within the Asia Pacific region, it is definitely advantageous for Sinwa.

(III) Going Forward:

It is planning to enter into the Thailand market, where the oil and gas industry is growing. Expectations are the demand for marine, offshore supply and logistical services would outstrip the local supply, hence, making it ideal for Sinwa to grab this opportunity. I had my concerns with regards to this, given Thailand’s political situation. Also, assuming that the company does enter into the Thailand market, we would not expect a huge increase in CAPEX, as the company will be resorting to renting until it has a steady customer base.

Also, the company has plans to expand its warehouse so that it is able to directly import chilled food such as Australian meat. By doing so, it is able to cut out the middleman, reduce operating cost and buy in bulk, which would further decrease operating costs. The company expects to spend SGD10.5 – 11million on building the bigger warehouse which, in my opinion, it is able to do so comfortably without taking excessive loans.

I feel that management has learnt from its past mistakes and is taking more prudent steps going forward in expanding its business.

Valuation:

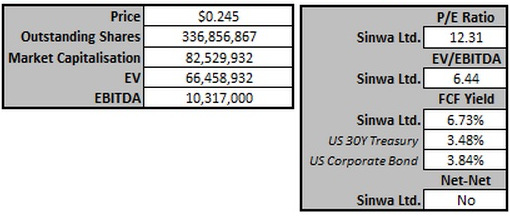

In terms of P/E, it is definitely not cheap especially based on empirical research on the Singapore market. In terms of EV/EBITDA of 6.44 it can be considered relatively fairly valued.

In terms of FCF yield, it is somewhat undervalued given that it has a FCF yield of 6.7% which is significantly above the benchmarks, even after applying a 33% discount for errors. Lastly, the company is definitely not a net-net based on Graham’s Net Working Capital formula.

Conclusion:

At the current price of SGD0.245, Sinwa is not an undervalued company in my opinion. Most of the indicators suggest that Sinwa is nearing being fairly valued.

Assessing Sinwa qualitatively, it is evident that management has been taking decisive steps in changing the company’s direction, which has proven successful for the time being, bringing the company back into the ‘green’.

Going forward, it would really depend on how successfully the management ‘steers this ship’, especially if they were to enter the Thai market. Overall, my view is that other than the fact that management has been able to turn the company around it still lacks a fair margin of safety for investors.

Disclosure: The author has no vested interest in Sinwa shares

Recent story: SINWA enters Thai offshore sector; AUSGROUP secures Barrick Gold contract