Excerpts from UK-based broker SP Angel's recently-released 148-page report on Rex International. (The report can be accessed after registration at http://www.spangel.co.uk/research-area.html)

Analyst: John Meyer

With a well balanced portfolio, adequate cash resources to meet its near to medium term obligations and a potentially game changing technology in Rex Virtual Drilling, Rex International Holdings (RIH) is well positioned.

With an unrisked valuation >10x the current valuation, we believe that our Target Price of S$1.19 is a fair reflection of the risks within the portfolio. Consequently, we are initiating coverage with a BUY recommendation.

Rex Virtual Drilling

Rex Virtual Drilling (“RVD”) is a proprietary technology that enables the visualisation of hydrocarbons using seismic data. By using a proprietary algorithm, RVD is able to identify differing liquids, and in respect of oil.

Analyst: John Meyer

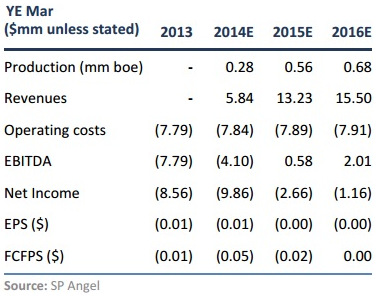

| We have valued RIH’s assets at $1,029mm (S$1.19) using DCF valuation methodology; the un‐ risked valuation is $9,915mm (S$11.50). |

With an unrisked valuation >10x the current valuation, we believe that our Target Price of S$1.19 is a fair reflection of the risks within the portfolio. Consequently, we are initiating coverage with a BUY recommendation.

Rex Virtual Drilling

Rex Virtual Drilling (“RVD”) is a proprietary technology that enables the visualisation of hydrocarbons using seismic data. By using a proprietary algorithm, RVD is able to identify differing liquids, and in respect of oil.

In excess of 41 tests have been carried out, with RIH reporting an 85 – 100% success rate at identifying whether the targeted accumulation contains oil, and more importantly, whether it will be a dry hole.

The most recent active test has resulted in a discovery in Oman, which opened up an entirely new basin hitherto believed to be unproductive.

Balanced Portfolio & Active Drilling Programme

The Company’s portfolio is well balanced, in terms of position in the exploration lifecycle, geographical diversity and play type. While the near term drilling programme focused on appraisal and exploration in Trinidad, Norway’s high impact exploration programme starts in 2H’14, and the Omani appraisal and Australian exploration programme kick off in 1H’15.

Cash Needs Covered

Cash Needs Covered

With a cash and available liquid cash resources of ~$79mm, we believe that the Company is fully covered for its near to medium term investment programme.

With a cash and available liquid cash resources of ~$79mm, we believe that the Company is fully covered for its near to medium term investment programme. This also excludes the cash positive effects of any revenues that it generates from its appraisal programmes in Trinidad & Tobago, due to start imminently, and Oman, which is scheduled to start in 2015.

Our outlook also excludes any cash flows arising from the development of a successful appraisal programme in Trinidad & Tobago, which in theory could follow swiftly from the appraisal programme given the location of the assets, and in the case the Omani appraisal well, the availability of a suitable rig.

Valuation $1,029mm (S$1.19)

We have valued RIH’s assets at $1,029mm (S$1.19) using DCF valuation methodology, and adjusting for exploration risk using EMV analysis; the unrisked valuation is $9,915mm (S$11.50).

With an active exploration and appraisal programme underway, we believe that there are numerous near term opportunities for the Company to be revaluated.

We initiate coverage with a BUY recommendation and a S$1.19 target price.

Recent story: REX -- this is a very busy year; MARCO POLO is new alpha pick

With an active exploration and appraisal programme underway, we believe that there are numerous near term opportunities for the Company to be revaluated.

We initiate coverage with a BUY recommendation and a S$1.19 target price.

Recent story: REX -- this is a very busy year; MARCO POLO is new alpha pick