Excerpts from a monthly investment outlook by Financial Alliance (FA) sent to its clients recently.

In November 2008, Financial Alliance (www.fa.com.sg) became the first and only Financial Adviser Firm in Singapore to achieve both the Singapore Quality Class and the People Developer status

• We believe that the fiscal cliff debacle could have an impact on markets.

As we approach the deadline in early January, we could see markets slide lower as investors adopt a neutral position going into the event with the thin yearend market conditions potentially aggravating the swings.

But overall, our view remains the same – any decline, even due to the fiscal cliff, will merely be part of the Stage 3 consolidation that is taking place.

• The world has moved into a period of slow and low growth with the risk of an outright global recession still very much on the cards.

Nevertheless, we continue to believe the present period to be the best time to accumulate equities or to increase one’s exposure to equities. History has shown us that markets have traditionally found a bottom during the most unlikely of times: when the economy is at its worst.

• We believe that we are getting closer and closer to an exit from Stage 3 to Stage 4, which would represent a strong rally to the upside.

So far, the strategy we have adopted to move back into the market via a dollar cost averaging method has worked very well. We are confident that our strategy to “accumulate now ahead of a breakout in late 2013 onwards” is on track.

Q. So the view that we are in Stage 3 of your 4-Stage Recovery Model is intact?

FA: Yes, absolutely. The second half of 2012 has turned out to be exactly as we had anticipated: markets continuing to be in consolidation but with sentiment waning as economic data turn from bad to worse.

For example, the euro zone economy is now on course for its deepest downturn since early 2009 and as such will remain a major drag on the world economy next year. Separately, Singapore recently cut its growth forecast for this year to around 1.5 percent and warned of a subdued 2013. In short, the world, as expected, has moved into a period of slow and low growth with the risk of an outright global recession still very much on the cards.

Nevertheless, we continue to believe the present period to be the best time to accumulate equities or to increase one’s exposure to equities. History has shown us that markets have traditionally found a bottom during the most unlikely of times: when the economy is at its worst.

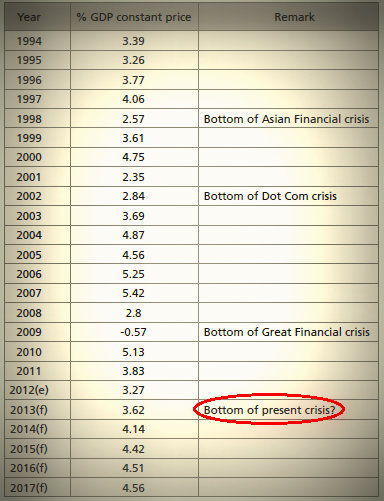

This is highlighted in the table on the right, which tracks the percentage year-on-year growth in Gross Domestic Product, adjusted for inflation, from 1994 to 2017 based on actual and IMF projected data.

Note that for the past 3 major crises (the Asian, Dot-com and Sub-prime crises), bottoms in the equity markets have often come in the year in which growth rates have been the lowest relative to the previous few years.

As such, with growth rates expected to be relatively slow

this year and next compared to those that we have seen in

recent years, we could see a bottom next year, if we haven’t

already seen one this year.

Q. Given the year is coming to an end, can you give your assessment of how it has been?

FA: It has not been an easy year for investors. There was a huge run-up in the first 8 weeks of the year to end-February, which lured many into jumping onto the bandwagon.

However, this gave way to an equally sharp downturn over the subsequent 10-weeks to mid-June, leaving markets basically back at square one by mid-year with confidence badly battered. Fortunately we sat through the whole episode, remaining sheltered by our very defensive position, which we had undertaken since August 2011.

It was only after this that we strategized to re-enter the markets as there was a sense of despondency among investors by mid-year. This made us comfortable to start our accumulation strategy given that all three indicators we look at: sentiment, fundamentals (excess liquidity and low growth) and technicals, were all aligned.

So far, the second half of the year has been a lot more investor-friendly as, from July onwards, markets have gradually moved up. This has worked really well for us as the five tranches for our Market Accumulation Portfolio were deployed during this period. So, in essence, our advice for clients at this point would be to stay the course – so far, so good.

Recent article: SANI HAMID: "Market consolidation in near term is healthy"