Page 1 of 2

Below is our report on Riverstone Holdings' 2014 results briefing. Joshua Wu, a private investor, had also attended the briefing and contributed an article to NextInsight last Friday: RIVERSTONE: "A Wonderful Company At A Fair Price"

Riverstone's share price ($1.185) has tripled in value in the last two years or so.

Riverstone's share price ($1.185) has tripled in value in the last two years or so. Chart: FT.com

STRONG SALES, favourable USD/RM forex rates, and tax incentives helped Riverstone Holdings soar to a record high profit of RM71 million last year -- and it proposed a final dividend of 4.55 sen.

With record profits come record dividends.

Considering the interim dividend of 2.35 sen already paid, the total dividend of 6.90 sen a share for FY2014 is a record high for the Malaysian-based glove manufacturer.

However, because of a sharp rise in the share price over the past two years, the trailing dividend yield currently stands at only about 2.2%. (See chart)

After the results briefing: Analysts and investors speak with management or discuss among themselves. Photo by Leong Chan Teik

After the results briefing: Analysts and investors speak with management or discuss among themselves. Photo by Leong Chan TeikSeveral takeaways from the recent 2014 results briefing:

1. Trade receivables: As at end-Dec 2014, they stood at RM86.7 million, up from RM62.5 million a year earlier.

Reason: Riverstone's new factory in Taiping, Perak, started production in Nov 2014, resulting in higher sales. Credit terms of about 60 days remained unchanged.

2. Tax incentives: The income tax expense in 4Q2104 amounted to only RM46,000 (compared to RM4.2 million in 4Q2013) despite 4Q2014 profit before tax being RM22.4 million (11.1% higher year-on-year).

Reason: There was a tax incentive (known as Reinvestment Allowance) on the RM63 million capex (not including land cost) for the new 1-billion capacity factory .

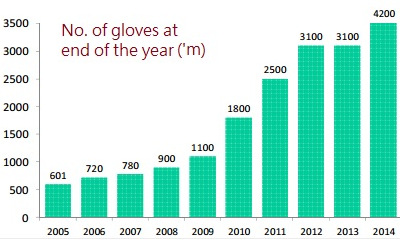

Riverstone has steadily expanded its production capacity of gloves. This year another factory with 1-billion glove capacity will come onstream. The same tax incentive will apply to another new 1-billion capacity factory which will be completed by the end of this year.

Riverstone has steadily expanded its production capacity of gloves. This year another factory with 1-billion glove capacity will come onstream. The same tax incentive will apply to another new 1-billion capacity factory which will be completed by the end of this year.The tax incentive on capex of RM50 million (not including land cost) is expected to be recognised in the 4Q of this year.

Riverstone plans to start building another factory in 3Q this year with a similar 1-billion capacity for RM80 million capex. When completed in 2016, it would raise its total production capacity to 6.2 billion gloves.

3. Selling prices: Gross profit margins have stayed constant but as raw material prices dipped, Riverstone passed on the savings to its healthcare glove customers owing to stiff competition in this business. Selling prices were adjusted on a monthly basis.

However, selling prices for cleanroom gloves were negotiated on a half-yearly, or yearly, basis.

Riverstone has benefitted from the strengthening of the USD agains the ringgit.

70-80% of its sales are recorded in USD while only 30-40% of raw material costs are paid in USD.