Excerpts from analysts' reports

AmFraser Research starts coverage of Valuetronics Analyst: Renfred Tay (left)

Analyst: Renfred Tay (left)

We initiate coverage on Valuetronics with a high conviction BUY rating with a DCF-based price target of S$0.69 (upside of 73%).

Valuetronics is an integrated electronics manufacturing service (EMS) provider based in Hong Kong, with manufacturing facilities in Guangdong, China.

Unloved by the market over the last few years, Valuetronics has demonstrated that it is rising back from the ashes.  Valuetronics chairman & CEO Tse Chong Hing owns an 18.5% stake in the company.

Valuetronics chairman & CEO Tse Chong Hing owns an 18.5% stake in the company.

Photo: CompanyRight now it is still trading at valuation levels associated with its darkest hours; this should not be the case in our view.

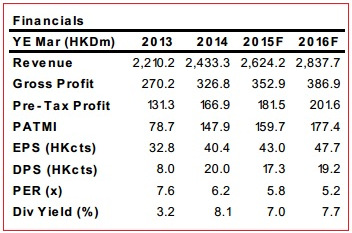

Too cheap to ignore. Trading at around 5.8x FY3/15F PE or 2.7x FY3/15F ex-cash PE, with an expected earnings growth rate of 10% in the coming years, valuations for Valuetronics looks too compelling to ignore.

Historical PE trend for this company does not count for much as its history and its current prospects are currently misaligned.

We believe our DCF-based valuation of Valuetronics (with very conservative assumptions and forecasts) properly showcase just how undervalued this stock is.

Bottom line growth with expanding margins. Driven by strong growth from its industrial and commercial electronics (ICE) segment, which commands much higher margins than its consumer electronics (CE) segment, net income is expected to continue to grow at a CAGR of 10% over the next three years. Valuetronics: Net cash makes up about half of its current total market capitalisation, a strong indication of value. Chart: Yahoo Finance

Valuetronics: Net cash makes up about half of its current total market capitalisation, a strong indication of value. Chart: Yahoo Finance

Strong balance sheet. Valuetronics has been virtually debt-free for almost all the years it was listed on the SGX. Its net cash position has also risen over the years from HKD 182m in FY3/08 to HKD 478m in FY3/14.

Strong balance sheet. Valuetronics has been virtually debt-free for almost all the years it was listed on the SGX. Its net cash position has also risen over the years from HKD 182m in FY3/08 to HKD 478m in FY3/14.

In addition, net cash is also about half of its current total market capitalisation; a strong indication of value.

Solid cash flows and dividends. Operating cash flows before working capital investments has also been increasing almost every year. Consequently, free-cash-flow-to-firm has always been positive (except for FY3/11).

Since its IPO, Valuetronics has been paying out dividends consistently. DPS announced for FY3/14 was 20 HKcts, compared to 7.8 HKcts back in FY3/08.

At the current price, and based on FY3/14’s dividend pay-out of 20 HKcts, dividend yield of 8.1% is very attractive.

Recent story: HANKORE Target $1.23; VALUETRONICS, 63.7 cents

See also NextInsight forum discussion.