Excerpts from analysts' reports

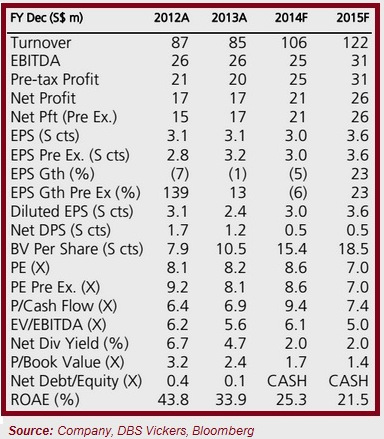

DBS Vickers: "Stay cautious on Yongnam" Entrance to Yongnam's office block and sprawling factory in Tuas South St 5. NextInsight file photoYongnam has won two structural steel subcontracts worth S$54.3m. The two contracts involve work at Changi Airport Terminal 4 and UIC Building along Shenton Way. Entrance to Yongnam's office block and sprawling factory in Tuas South St 5. NextInsight file photoYongnam has won two structural steel subcontracts worth S$54.3m. The two contracts involve work at Changi Airport Terminal 4 and UIC Building along Shenton Way. Our analyst has a project win assumption of S$200m for FY14F and S$300m in FY15F. The contract wins are within our estimate. While management expects the projects to have an impact on FY14F's financials, we maintain our negative stance on the stock.

Revenue growth is expected to decline this year on smaller quantum of order book draw down. Margins are also expected to be relatively lower due to higher proportion of lower margin structural steelworks in the pipeline. Valuation is currently above 10x PE, a premium to peers' 7-8x. No change to Fully Valued recommendation and S$0.20 TP. Recent story: Analyst ratings: 'Neutral' for SIIC, 'Reduce' for YONGNAM |

DBS Vickers initiates coverage of Kim Heng with 33-c target price

Analyst: Ho Pei Hwa

A pioneer in Singapore’s O&M industry. With over 40 years of track record and long-standing relationships with global blue-chip names like Transocean, Noble, Seadrill and McDermott, Kim Heng is a leading integrated O&M service provider that offers comprehensive services including offshore rig repair & maintenance, reactivation/refurbishment of old rigs, block fabrications, newbuilding of piplelay /accommodation vessels and supply chain management.

M&A and conversion/newbuild projects to boost growth further. We forecast 23% net profit CAGR in FY13-15F, driven by:

1) Buoyant E&P activities and high rig utilisation; and

1) Buoyant E&P activities and high rig utilisation; and

2) 38% increase in yearly rig deliveries.

We see room for an earnings upgrade, stemming from:

1) The securing of high value projects like jackup conversions and newbuild orders, which may boost bottomline by up to 24% per project if executed well; and

2) Earnings accretions from acquisitions of subsea equipment servicing & engineering businesses or other assets such as OSVs, on the back of fortified balance sheet post-listing.

Time to bottom fish. Value emerges as the stock has fallen 22% from its high of 32.5 Scts and near its IPO price of 25 Scts.

Despite recent rebound from 22.5 Scts, it is still a bargain at 8.6x FY14 PE and 1.7x P/BV for a niche player with >20% ROE and earnings growth with imminent re-rating catalysts.

Initiate with a BUY and TP at S$0.33 based on 11x FY14 PE, in line with average valuation of small/mid cap O&M peers listed on SGX.