Excerpts from analyst reports Sing Holdings will recognize bulk of remaining S$182.1m from the The Laurels in FY13; potential $348.8 m from Punggol EC project over FY13‐15; and bulk of potential $357 m from the Robin site in FY14‐15.AmFraser initiates coverage of Sing Holdings with 56-c target

Sing Holdings will recognize bulk of remaining S$182.1m from the The Laurels in FY13; potential $348.8 m from Punggol EC project over FY13‐15; and bulk of potential $357 m from the Robin site in FY14‐15.AmFraser initiates coverage of Sing Holdings with 56-c target

Analyst: Sarah Wong

We initiate coverage on Sing Holdings with a BUY rating and a fair value of S$0.56, based on a 40% discount to our RNAV estimates of S$0.94.

Sing Holdings, a niche luxury developer that has recently moved into the EC segment which has strong supply-demand dynamics, currently trades at a massive 56% discount to its RNAV.  Lee Sze Hao, CEO of Sing Holdings. NextInsight file photoWith earnings visibility and huge cash inflows from pre-sold units of The Laurels and two other launches, Sing Holdings will boast of a stronger financial position and a stable dividend over FY13-15.

Lee Sze Hao, CEO of Sing Holdings. NextInsight file photoWith earnings visibility and huge cash inflows from pre-sold units of The Laurels and two other launches, Sing Holdings will boast of a stronger financial position and a stable dividend over FY13-15.

We expect its pipeline of projects to add S$0.33 to its current NAV.

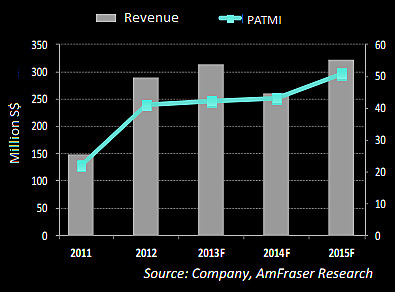

We expect PATMI to grow at 9.5% CAGR from 2013‐15, and a sustainable dividend per share of 1.6c in 2013‐15. This translates into a forward yield of 3.9%.

We also expect massive cash inflows from progress payments to strengthen Sing Holdings’ financial position and pave way for more landbank acquisitions ahead.

At current price levels, Sing Holdings offers a strong value proposition, on top of rewarding shareholders with a decent and sustainable yield of 3.9%.

Click here for the full AmFraser report

Recent story: KEVIN SCULLY: Raising target price of Sing Holdings

OSK-DMG sets 73-c target for AusGroup

Analysts: Lee Yue Jer & Jason Saw

Laurie Barlow, CEO of AusGroup. NextInsight file photoAusGroup now has a record AUD4.5bn tender book, dwarfing the AUD0.6bn of tenders at Dec-12.

Laurie Barlow, CEO of AusGroup. NextInsight file photoAusGroup now has a record AUD4.5bn tender book, dwarfing the AUD0.6bn of tenders at Dec-12.

The build-up of the tender book was due to the delays of the contract awards, and we expect AusGroup to convert about 20% of its tenders into firm contracts, providing good-margin work for 2H13 through FY15F. Further, this week Upstream noted that Ensco has been awarded the final Ichthys drilling contract.

AusGroup’s shares have come off 25% since its recent peak, and now trades at 6.9x FY13F EPS, 1.1x P/B, with an EV/EBITDA under 3.0x (based on current price of SGD0.50).

These are extremely compelling valuations for a company growing at 20% EPS CAGR to FY15F, ROE consistently above 15%, and a strong net cash position of SGD0.054 per share. We believe that the reaction to the poor 2Q13 results (which included one-off expenses and variation orders) is severely

overdone, and this is the time to enter.

Our TP of SGD0.73 is based on 9x blended FY13F/FY14F EPS. BUY.

Recent story: AUSGROUP: 1HFY2013 revenue up 12% at A$307m on increased oil & gas activities

Comments

Sing Holdings will recognize bulk of remaining S$182.1m from the The Laurels in FY13; $348.8 m from Punggol EC project over FY13‐15; and bulk of $357 m from the Robin Site in FY14‐15.

I think should add in "potential" $348.8mil from Punggol EC project and "potential" $357m from Robin site.

Can someone advice whether the other two project has been launched and sold or still pending launch?

Tks.

Yee