Goldman Sachs: CHOW SANG SANG Initiated with ‘Neutral’ Call

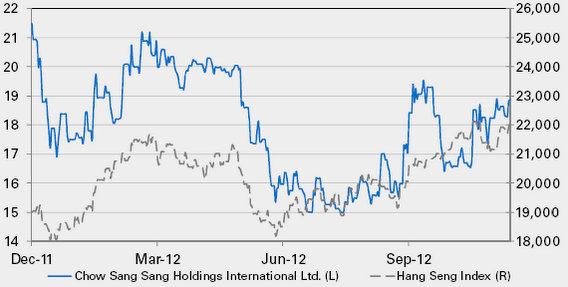

Goldman Sachs said it is beginning coverage of Hong Kong’s No.2 jewelry retailer Chow Sang Sang (HK: 116) with a “Neutral” call and target price of 20.4 hkd, which implies a 2013E P/E of 12.3x (recent share price: 18.18 hkd).

“Chow Sang Sang is a Hong Kong heritage jewelry brand with over 70 years of history and a 10.5% market share in Hong Kong -- the second largest player.

“We believe that as the cyclical headwinds on hard luxury consumption (macro slowdown/political uncertainty/tough comp base in 2011) gradually lapse, Chow Sang Sang’s growth and profitability are poised to recover together with the sector,” Goldman Sachs said.

The research house said it currently estimates that Chow Sang Sang will deliver SSSG of 12% in 2013E and generate over HK$500mn free cash flow; if SSSG rebounded more robustly to +22% (i.e, 10ppt more than our base case) in 2013E, CSS would swing into negative free cash flow of more than HK$400mn.

“We think its 2012E cash position of around HK$700mn could barely fund such rapid growth, and the company’s net gearing would rise to 31% by 2013E end (from 23% at 1H2012), a level much higher than peers and than its own history.”

Core growth drivers

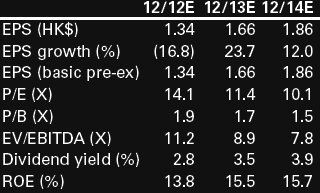

Goldman Sachs said it forecasts a 17% OP decline in 2012E followed by +18% OP CAGR in 2013E/14E.

“In 1H12 the company’s OP slid by 17% yoy and we don’t expect significant improvement in the 2H as 3Q SSSG run rate (negative low single digit group-wide) was worse than the low teens positive SSSG recorded in 1H.”

The research house said its recovery view on 2013E/14E is driven by (1) 16% retail sales CAGR based on 9-12% SSSG in 2013E/14E and network expansion of 12% p.a., and (2) retail OP margin expansion from the cyclical trough of 7.8% in 2012E to 8.1% in 2014E.

“Our 2013E/14E SSSG expectation is in line with our industry forecast of high single digit p.a. volume growth on gold jewelry demand and mid single digit gold price appreciation p.a. by 2015E.”

Goldman Sachs said an upside risk to its “Neutral” call are sales/earnings/returns possibly rising faster than it forecast if consumption recovery/commodity price appreciation comes in stronger than expected.

Another is if improvement in gem-set inventory turnover creates more free cash to fund further growth opportunities.

Goldman Sachs coverage view on Chow Sang Sang’s industry is “Attractive.”

See also:

GOLDEN OPPORTUNITIES? CHOW SANG SANG Jewelry ‘Outperform’; RETAIL Upbeat

CHOW SANG SANG Target Hiked

CHOW SANG SANG’S Sparkling Review; LENOVO Aiming For Clouds

Credit Suisse: PRC Malls Outperforming Department Stores

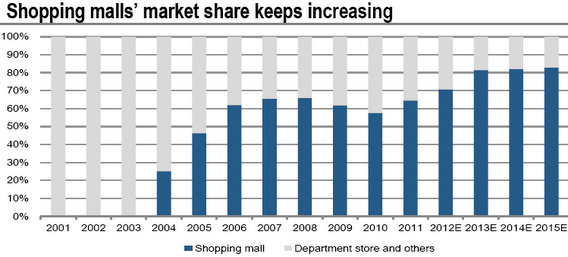

Credit Suisse said that based on a survey of Chengdu, a city with an urban area of over 14 million residents, listed shopping malls are outperforming established department stores in the retail sector.

“Our recent visit to Chengdu confirmed our view that shopping malls are taking over market share from department stores in Tier 2 cities.

“YTD, Chengdu’s retail sales were up 15% YoY, but industry experts said many department stores’ sales declined around 10% YoY as malls took market share from department stores,” Credit Suisse said.

The research house conducted a detailed study of the four new malls in Chengdu -- three of them opened just this year, and one is scheduled to open end-2013 but is already 77% pre-leased.

“Raffles City Chengdu by Singapore-listed CapitaMalls Asia and MIXc by CR Land have managed a near 100% occupancy quickly, with relatively strong foot traffic and sales, even though MIXc’s location is not well-developed yet,” Credit Suisse said.

The broker call said it was most upbeat on CR Land and CMA.

“By achieving a satisfying rental growth in Chengdu and strong sales in Nanning MIXc, we believe CR Land deserves a re-rating as its shopping mall assets are still undervalued.

"The success of Raffles City Chengdu is also an example that 2013 may be the harvesting period for CMA.”

The strong pipeline of retail space (mostly shopping malls) may lead to potential oversupply and thus put pressure on existing department stores and shopping malls, Credit Suisse added.

“However, most of the new supply is in the north, central and south of Chengdu.

"CR Land’s MIXc Mall, in the east, should be less affected by the upcoming pipeline. Historical data tell us that many of the malls’ openings may be delayed significantly.”

See also:

XTEP's Rating Kept At ‘Buy’, Sportswear On Ascent

XTEP: Overperforming In Overcrowded, Overstocked PRC Sportswear

TWO LEFT FEET: China Sneaker Play Li Ning Sees Dire Year