The business segment has improved utilization rates to 57% with stable gross profit margin of 19%. • That is part of ASL's strong 1HFY26 results, with a net profit of $17.1 million, cementing a comeback story after years in the doldrums when it slogged through debt issues and a tough industry cycle. • For more, read excerpts of UOB Kay Hian's report below ... |

Excerpts from UOB Kay Hian report

Analyst: Heidi Mo

Highlights • ASL’s 1HFY26 PATMI of S$17.1m formed 57% of our full-year estimates, beating our expectations due to stronger repair margins and sharply lower finance costs.

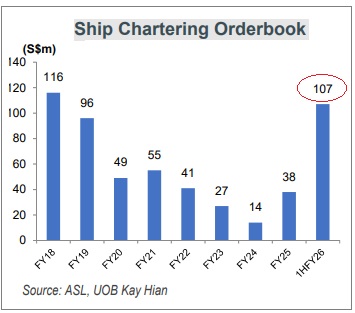

• A 30% qoq rise in ship chartering orderbook to S$107m and continued deleveraging (net gearing of 0.77x from 1.35x) supports stronger cash flow. |

|||||

Analysis

• Results above expectations. ASL Marine (ASL) reported 1HFY26 PATMI of S$17.1m (+1,076.1% yoy), forming 57% of our full-year forecast and exceeding expectations.

Excluding non-cash amortisation of bank loans and bonds, underlying profit rose 64% yoy, reflecting operating improvement.  Ang Kok Tian, Executive Chairman & CEO.The revenue of S$181.6m (+5.5% yoy) was in line with our expectations, while gross profit surged 24% yoy to S$35.1m as gross margin expanded to 19.3% (+2.9ppt yoy).

Ang Kok Tian, Executive Chairman & CEO.The revenue of S$181.6m (+5.5% yoy) was in line with our expectations, while gross profit surged 24% yoy to S$35.1m as gross margin expanded to 19.3% (+2.9ppt yoy).

Finance costs declined sharply by 72.8% yoy to S$4m following continued deleveraging.

• Interim dividend declared. ASL declared an interim dividend of 0.13 S cents per share (8% payout), reflecting confidence in sustainable cash flow generation.

• Ship repair: Core earnings anchor. Ship repair revenue rose 9.7% yoy to S$93.3m (51% of revenue), driven by higher-value repair projects and engineering product sales.

This segment continues to anchor earnings, benefitting from resilient demand from regulatory drydockings and fleet ageing.

• Ship chartering: Infrastructure support offset fleet rationalisation.

Ship chartering revenue increased 2.5% yoy to S$51.6m, supported by local infrastructure projects.

Fleet utilisation improved to 57% (+6ppt hoh).

This offset lower income from vessels held for sale under ASL’s optimisation strategy.

As at 31 Dec 25, order book stood at S$107m (+30% qoq), providing earnings visibility.

• Shipbuilding: Moderating pipeline; higher-value focus. Shipbuilding revenue remained flat yoy at S$36.8m.

Orderbook declined to S$49m (-40% qoq) as at 31 Dec 25, reflecting saturation in Indonesia’s barge market and softer coal demand.

Management is pivoting toward more complex, highervalue barges and workboats, which should support margins despite lower volume.

• Strengthening balance sheet and cash flow. Operating cash flow remained healthy at S$31.7m in 1HFY26. Cash more than doubled to S$48m, while net gearing improved significantly to 0.77x (from 1.32x in FY25).

The S$132m Club Deal 2 has been pared down to S$86.5m, with further S$35m prepayments expected in 2HFY26 (by Jun 26).

• Pivot toward repairs and chartering improves earnings quality. The 30% qoq increase in chartering orderbook, alongside the 40% qoq decline in shipbuilding orders signals a continued pivot toward infrastructure-linked chartering and recurring repair activity.

We expect shipbuilding to form a smaller share of group revenue going forward, reducing revenue lumpiness and working capital needs.

With repair margins holding above 20% and chartering supported by infrastructure demand (including Singapore’s S$100b coastal protection initiatives), earnings quality and cash flow visibility should continue to improve into 2HFY26

• Maintain BUY with a 23% higher target price of S$0.43 (S$0.35 previously), after raising our earnings forecasts and rolling our valuation base year to FY27.  Heidi Mo, analyst• Our target price is pegged to 12x FY27F PE, a slight discount to peers. Heidi Mo, analyst• Our target price is pegged to 12x FY27F PE, a slight discount to peers. ASL trades at an undemanding 9x FY27F PE despite its improving profitability and strengthening balance sheet. In our view, the market has yet to fully reflect the repair tailwinds and ongoing shift toward recurring repair and infrastructure-linked chartering, which reduces cyclicality. • As deleveraging continues and dividend headroom grows, we see scope for further re-rating toward its peers’ average of 13x PE. Earnings Revision • We raise our FY26-28 earnings forecasts by 4-9%, following the strongerthan-expected 1HFY26 performance. This reflects higher gross margins and reduced interest expense as debt continues to be pared down. |

Share Price Catalyst

• Higher contract wins across business segments.

• Expansion of dry-dock capacity in early-FY27.

• Higher dividend payout. → See the full UOB KH report.

→ See the full UOB KH report.

→ See also:NAM CHEONG: Touches 2-year high following CGS' and DBS' bullish notes