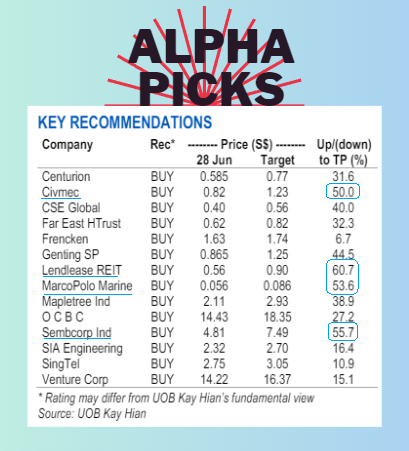

• UOB Kay Hian's alpha picks portfolio has consistently done well. • UOB Kay Hian's alpha picks portfolio has consistently done well. Its top performers in June 24 were Frencken (+12.4% mom), Singtel (+10.9% mom) and Centurion (+10.4% mom). • What are its stock picks with the highest upside potential? There are 4 with target prices with an upside exceeding 50%: Civmec, Landlease REIT, Marco Polo Marine and Sembcorp Industries. • Marco Polo's stock reached a high of 7.1 cents in mid-May 2024, and has corrected to 5.6 cents. But its story continues to be robust: demand for its offshore support vessels is hot while industry supply of such vessels is not growing.  Photo: Marco Polo• Marco Polo's support vessels have been transporting, and supporting the installation of, large wind turbine components during the construction of offshore wind farms in Taiwan. Photo: Marco Polo• Marco Polo's support vessels have been transporting, and supporting the installation of, large wind turbine components during the construction of offshore wind farms in Taiwan. • The fleet also provides support for the operations and maintenance (O&M) of wind farms. • It's not just Taiwan where Marco Polo has gained a foothold. Marco Polo is seeking business also from Japan and South Korea owners of offshore wind farms. Read more about this from UOB Kay Hian's latest report .... |

Excerpts from UOB KH report

Analysts: Heidi Mo & John Cheong

| Marco Polo Marine – BUY |

• Charter and utilisation rates for OSVs continue upward momentum. In 1HFY24, Marco Polo Marine’s (MPM) ship chartering revenue soared 34.3% yoy to S$32.9m.

According to Clarksons Research, global offshore support vessel (OSV) utilisation stood at 73% in 2023, while day rates have surpassed previous peaks in 2013-14. |

||||

• CSOV to be key contributor from FY25. MPM's new CSOV is around 69% complete as of 31 Mar 24, and scheduled to begin operations in Oct 24.

This CSOV will be deployed over three years at an agreed utilisation rate per annum under its Vestas Framework Agreement, with its first stop being Taiwan.

|

Key drivers |

|

“Due to limited investments since the oil price crash in 2016 and the lack of bank financing, the supply of vessels have been unable to keep up with the surge in demand, due to competition from the renewable energy sector.” |

According to 4C Offshore Market Intelligence, there are 14 CSOVs and 29 service operation vessels (SOV) in operation worldwide as of 8 Mar 24, with the majority contracted in Europe.

In line with larger capacity turbines furthering offshore, such vessels with larger capacity are seeing increasing demand.

As the cost of building such vessels rises, the limited supply points to better day rates and utilisation for MPM's CSOV moving forward.

• Maiden deployment of new CTV in FY25 may unlock more opportunities. Having successfully entered the Taiwan offshore wind market, MPM is also drawing on its expertise to serve the Korea market this year.

In Mar 24, MPM announced its Asia-Pacific Crew Transfer Vessel (CTV) framework agreement with Siemens Gamesa for projects across Taiwan and Korea.

Its maiden CTV charter in Korea will start in 4Q24, marking MPM's successful entry into a new market.

We think that this partnership will further boost MPM's track record and potentially provide more opportunities to accelerate its growth.

We value MPM at 11x FY24F PE, based on +2SD above its historical three-year average PE range on the back of improving charter rates and vessel utilisation rates. MPM trades at an attractive 9x FY24F PE. SHARE PRICE CATALYSTS • Events:

• Timeline: 3-6 months. |

Full report here