|

Excerpts from Phillip Securities report

Analyst: Paul Chew

Pacific Radiance Ltd (PACRA) -- The Revival

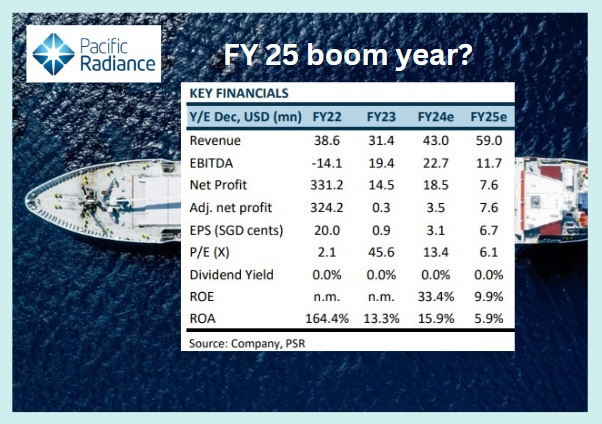

| ▪ We expect earnings to jump in FY25e, backed by more than US$40mn of charter contracts, the construction of crew transfer vehicles, and increased scale in ship management operations. The restructuring of associate Logindo will further enhance the company's valuation. ▪ Following the debt forgiveness exercise, vessel disposal, and rights issue, the company's net debt has shrunk from US$365mn to US$24mn net cash. Funds have been used to expand shipbuilding, reduce interest expenses and re-activate laid-up vessels for charter. ▪ We initiate coverage with a BUY recommendation and target price of S$0.06. Valuations pegged to the industry average of 8x PE. |

The offshore support vessel industry is enjoying a resurgence in charter rates from rising demand as global offshore capex recovers.

Supply is constrained by an ageing fleet and a decline in shipyard capacity where vessel orders are only 3% of the existing fleet.

Pacific Radiance is riding on higher charter rates as it rebuilds its fleet and expands shipyard capabilities.

Stock is trading at a 40% discount to book.

| SHIP MANAGEMENT |

For its Ship Management revenue, PACRA charges a fixed monthly fee per vessel it manages, with fees increasing for each add-on service, such as procurement, agency services, marketing, and chartering.

|

Pacific Radiance |

|

|

Share price: |

Target: |

This asset-light and easily scalable business model allows the company to avoid additional costs. Pacific Radiance currently manages 30 vessels, some of which it previously owned.

We expect the number of vessels they manage to increase by 5- 10 per year as more fragmented owners buy distressed ships and lack the skills to manage them.

As the operations scale up, we expect a stronger contribution to earnings.

| SHIP CHARTERING |

In 2023, PACRA only owned one 60 men utility vessel Crest Radiance 5.

"The outlook for OSVs is positive, driven by rising demand in global offshore capex. Supply is constrained by an aging active and laid up fleet, decline in global shipyard capacity and limited new orders (less than 5% of AHTS fleet on order), There are around 1,850 AHTS globally, with an average age of almost 19 years." "The outlook for OSVs is positive, driven by rising demand in global offshore capex. Supply is constrained by an aging active and laid up fleet, decline in global shipyard capacity and limited new orders (less than 5% of AHTS fleet on order), There are around 1,850 AHTS globally, with an average age of almost 19 years."-- Paul Chew, head of research, Phillip Securities |

Following the restructuring and rights issue, PACRA is reactivating three vessels (65m anchor handling tug supply vessel, 60-man workboat, and a 400 man accommodation barge) in 2H24 for lease to customers (Appendix 1).

In August 2024, the company announced US$31.6mn of ship chartering contracts for the accommodation barge (Crest Station 1) and US$9.2mn for the AHTS (Crest Mercury 2).

We believe the full-year contribution will start in FY25e.

There are also four CTVs in operation in Taiwan. Due to cabotage rules, the CTVs are owned as joint ventures.

Contribution is equity accounting associate earnings and interest income.

Charter rates for CTVs range from US$7,000 to US$8,000 per day. Mainprize Asia Ventures (49% stake) operates the Taiwan CTVs.

| HIGHLIGHTS |

• Return of OSV ship chartering earnings. In 2H24, PACRA will take delivery of three major OSVs that will provide earnings growth in FY25e.

The largest vessel is a 400-man accommodation barge Crest Station 1, to be delivered in October 2024.

This vessel has secured a US$31.6mn charter contract, including an option for extension for deployment in the Middle East.

A 60-man workboat (Crest Mas) and an AHTS (Crest Mercury) are the other vessels.

The vessels are not newly built but re-activated after being laid up for several years.

PACRA has a track record in operating and reactivating vessels.

• New shipyard activities. We expect PACRA to begin construction work on two new crew transfer vehicles (CTVs).

Upon completion in FY25e, the customer will be finalised either by sale or internal use.

Demand for CTVs is robust as Taiwan embarks on a massive rollout of offshore wind farms, from 2.1GW in 2023 to 13.1GW by 2030, a CAGR of 30%.

| • Upside from off-balance sheet operations. PACRA has a 32.4% stake in Indonesia-listed Logindo, which was written off the balance sheet in 2022. Logindo is undergoing a two-stage restructuring of its operations. Vessels will be marketed globally where charter rates are higher or disposed of to reduce gearing. PACRA also operates four flagged CTVs to maintain and install offshore wind farms in Taiwan. The contribution will be smaller due to a lower equity stake. |

Full report here.