|

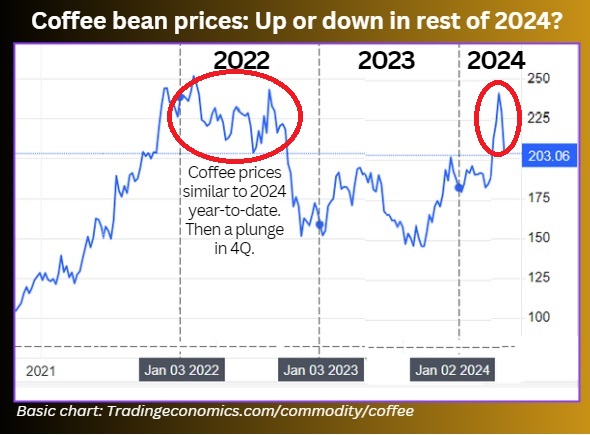

• While it was the spike in coffee prices that likely cooled investor sentiment towards Food Empire stock, the trajectory of coffee prices is uncertain. |

But first, take a look at Food Empire's 10-year profit trend which suggests it can overcome headwinds such as raw material price increases:  Note: FY2022 profit of US$45 m excludes one-off property divestment gain.

Note: FY2022 profit of US$45 m excludes one-off property divestment gain.

Excerpts from UOB KH report

Analysts: John Cheong & Heidi Mo

Food Empire Holdings (FEH SP)

FEH reported 1Q24 revenue of US$117.5m (+14.5% yoy), forming 26% of our full-year estimate. |

RESULTS

| Revenue in line with expectations; no profit figures disclosed |

• Food Empire (FEH) reported top-line of US$117.5m (+14.5% yoy) for 1Q24, which accounts for 26% of our full-year forecast, in line with expectations. Unlike prior quarterly updates, no other figures were disclosed.

|

Food Empire |

|

|

Share price: |

Target: |

• Higher yoy revenue from robust growth in Southeast Asia market. Revenue from Russia rose 3.2% yoy and 16% qoq to US$39.2m despite the currency depreciation of the Russian ruble against the US dollar.

In local currency terms, FEH reported a substantial 27.4% yoy growth in revenue from Russia, signalling sustained strong demand in its largest operating market. Most of its other markets also recorded double-digit growth during the quarter.

Notably, Southeast Asia revenue grew 35.3% yoy to US$29.9m, boosted by FEH's brand-building efforts in Vietnam.

Vietnam has become FEH's fastest growing market, aided by the restructuring of its local sales team, newly-launched marketing tactics and promotions in line with festivities like Tet (8-14 Feb 24).

| Expansion of non-dairy creamer production capacity completed ... |

• ... and construction of new snack factory begins. FEH's newly added non-dairy creamer (NDC) production facility in Malaysia has commenced commercial production on 1 Apr 24.  Food Empire operates a non-diary creamer factory in Johor. Some of the output is used internally and the rest is sold to third parties.

Food Empire operates a non-diary creamer factory in Johor. Some of the output is used internally and the rest is sold to third parties.

This expansion will ensure FEH has ample capacity to support its current and future customers' needs, and is expected to reach full utilisation in the next two to three years.

Additionally, FEH has begun construction of a second snack manufacturing plant adjacent to its existing one in Malaysia. This is expected to expand production capacity for its snack business from 2025.

STOCK IMPACT

| Record-high coffee prices to impact margins |

• International robusta coffee bean prices have surged to new highs on unfavourable weather, rallying to US$246/lb in April.

The recent poor harvests and continued drought in Vietnam, the world's largest robusta producer, have led to concerns for the next harvest and hoarding of beans.

FEH is thus likely to face profit margin compression, as robusta is the main ingredient of its instant coffee blends. We have cut our 2024-26 gross profit margin forecasts by around 4ppt to 29-30%.

| Top-line growth driven by strong consumer demand |

• With the strong levels of demand sustained amid inflationary pressures and currency volatility from geopolitical uncertainties, our forecast incorporates a 6-7% increase in 2024-26 revenue.

Furthermore, management expects higher revenues from:

a) Malaysia, with its newly added NDC facility, and

b) Vietnam, as active advertising and promotions continue to drive growth.

| Frequent share buybacks to date reflect confidence |

• FEH has bought back 3.4m shares at up to S$1.40 ytd, demonstrating management's confidence in the company's future growth outlook.

| EARNINGS REVISION/RISK |

• We lower our 2024-26 earnings estimates by 22-23% to S$46m/S$50m/S$54m respectively, down from S$60m/S$64m/S$69m.

This is a result of the expected gross profit margin compression during the period from rising raw material costs.

We have cut 2024-26 gross profit margins by around 4ppt to 29-30%, based on 2021-22 company performance when coffee prices were at similar levels.

VALUATION/RECOMMENDATION John Cheong, analyst• Maintain BUY with a 23% lower PE-based target price of S$1.30 (S$1.69 previously), pegged to 11x 2024F EPS, or its long-term historical mean. John Cheong, analyst• Maintain BUY with a 23% lower PE-based target price of S$1.30 (S$1.69 previously), pegged to 11x 2024F EPS, or its long-term historical mean. While rising coffee bean prices are likely to impact margins moving forward, FEH continues to record revenue growth during the period, illustrating its strong brand equity. We therefore still like FEH for its growth prospects. SHARE PRICE CATALYST • Dividend surprise from robust financials. • Better-than-expected sales volumes across all business segments. • Improving net margin from higher ASPs and effective cost management. |

Full report here.