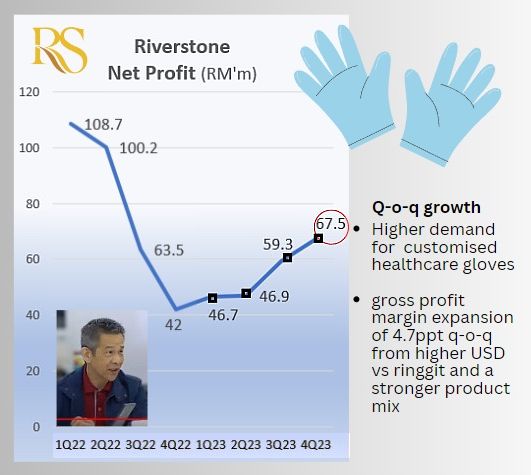

Inset: Executive Chairman & CEO Wong Teek Son Inset: Executive Chairman & CEO Wong Teek SonAs the chart shows, a profit recovery was underway for Riverstone Holdings for 4 consecutive quarters in 2023. Question is, will the trajectory continue to be upward in 2024? (More on this later) Meanwhile, after a look at the chart, the uninitiated may wonder (as will readers who have not tracked Riverstone closely) why there was a profit plunge in 2022. 2022 was the year after the super peak in demand for healthcare gloves during the Covid pandemic (see chart below). Earnings for Riverstone in 2020 was also driven by the pandemic, which means it was not going to be sustainable.

|

|

What factors will drive Riverstone's (continued) profitability this year?

Why have its Bursa Malaysia-listed peers continued to report losses?

The key differentiating factor is Riverstone, aside from healthcare gloves used in homes and medical settings, also produces gloves for use in electronics and semiconductor cleanrooms.

These require higher specifications and customisation than healthcare gloves, and Riverstone has been doing R&D and producing for a long time.

1. Riverstone's sales of cleanrooms gloves are expected to rise with a recovery in the semiconductor industry.

This plus new clients will be more than offset a likely reduction by Riverstone in the selling prices of certain types of its cleanroom gloves which are of lower specifications.

Riverstone seeks to protect its market share against regional players who are building up production capacity.

Typically, cleanroom gloves bring in the lion's share of Riverstone's profits -- in terms of absolute dollars and profit margin.

Consider the large disparity in pricing: In 4Q23, for example, Riverstone's cleanroom gloves and healthcare gloves fetched an average US$90 per 1,000 pieces and US$28.50, respectively.

2. Riverstone is edging towards greater emphasis on customised healthcare gloves, instead of generic ones, for better margins.

That started in 2023, resulting in better gross margin for healthcare gloves, and will gain more traction in the years to come, according to management.

At a cost of about RM70 million, several production lines for generic gloves are being replaced with newer lines that can produce customised glove offerings. The new lines will start operations in 3Q24.

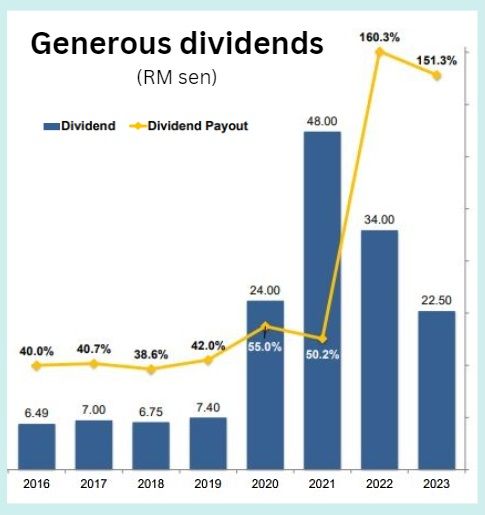

Riverstone recommended a special interim dividend of 5.0 sen per share and proposed a final dividend of 7.5 sen per share for FY2023. These bring the total for FY23 to 22.5 sen per share for a yield of 9-10%. Looking at the chart, you may think there's a error but no, the payout ratios in 2023 and 2022 amount to 151% and 160%, respectively. That is, the dividends exceeded the earnings for those years as Riverstone distributed from its cashpile which soared during the Covid period. With contined strong operating cashflow in 2023, Riverstone ended 2023 with a large cashpile of RM875 million. |

| Potential challenges: 1. Raw material price increases: While Riverstone regularly negotiates transaction prices with its glove buyers, it may not be able to pass on all of a hike in raw material prices.  Chart: Yahoo!2. USD-ringgit fluctuations: Riverstone reports its financial statements in ringgit, which will suffer if the USD weakens. Chart: Yahoo!2. USD-ringgit fluctuations: Riverstone reports its financial statements in ringgit, which will suffer if the USD weakens. Riverstone sells its gloves in USD. In 2023, the forex was favourable to Riverstone as the ringgit weakened slightly, continuing its long-term decline. |