Excerpts from RHB report

Analysts: Jarick Seet & Lee Cai Ling

♦ Reiterate BUY with a lower SGD0.17 TP, from SGD0.19, 52% upside. GSS reported a lower than expected NPAT of SGD2.31m due to one off impairment expenses from its O&G segment and amortisation expense associated with the approved corporate share option scheme.

As a result, we shift the timing of gas income to 3Q19 and lower our FY19F and FY20F PATMI by 6% and 8%, resulting in a lower DCF-backed TP of SGD0.17. |

||||

Watch 2-minute video of visit to Batam factory -->

Watch 2-minute video of visit to Batam factory -->

♦ New incoming projects to further drive PE growth. Despite ongoing trade war issues, precision engineering (PE) segment registered healthy growth; the bulk of its revenue is mainly generated from its Batam factory which is undergoing expansion due to increased orders from new and existing customers.  GSS Energy's CEO, Sydney Yeung.

GSS Energy's CEO, Sydney Yeung.

NextInsight file photo With increased lines of operations from factories in Batam and China, it will likely be able to accept large scale projects immediately.

GSS will also be involved in the manufacturing and assembling of both gasoline and electric models in the 125cc and 150cc categories and three-wheelers (“tuktuk”) in South-East Asia markets, India and Taiwan of the iconic ISOMOTO model.

We expect its PE segment to continue to grow 10-15% in FY19F.

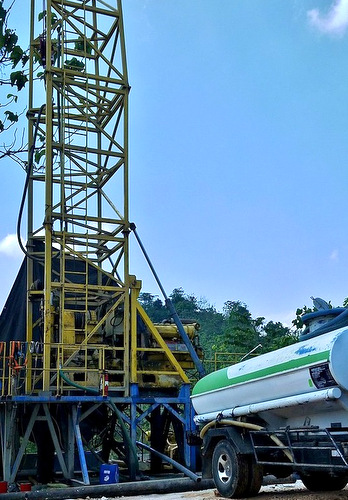

GSS Energy will start producing gas in Indonesia in 2H19. Photo: Company♦ O&G segment likely to bear fruit in FY19F. Its O&G segment suffered several setbacks and delays throughout the year. GSS Energy will start producing gas in Indonesia in 2H19. Photo: Company♦ O&G segment likely to bear fruit in FY19F. Its O&G segment suffered several setbacks and delays throughout the year.However, we estimate this business will bear fruit in FY19F. GSS will likely be able to monetize the two gas wells it discovered earlier this year as the company is at an advanced stage of regulatory approvals to monetise the two proven wells. In addition, management is also exploring the option of farming out part of the oil field, which will enable GSS to get a lump sum cash injection and also peg a value on its O&G assets, which are currently not reflected in its market capitalization. |

Jarick Seet♦ A better FY19F ahead. We like GSS’ prospects and expect both twin drivers to contribute positively to the business in FY19F. We believe the group is close to securing an off-taker for its O&G assets, and think the current weakness represents a good opportunity to accumulate.

Jarick Seet♦ A better FY19F ahead. We like GSS’ prospects and expect both twin drivers to contribute positively to the business in FY19F. We believe the group is close to securing an off-taker for its O&G assets, and think the current weakness represents a good opportunity to accumulate.

GSS also expects the monetisation of the two gas wells to happen in 2H19. As a result, we shift the timing of the gas income to 3Q19 and lower 6% and 8% our FY19F and FY20F PATMI, resulting in a lower DCF-backed TP of SGD0.17.

Key Risks: Decrease in oil price, trade war worsening and delay in monetisation of O&G assets.

RHB is the only broker covering this counter.

Full report here.