Soo Jin Hou contributed this article to Nextinsight

|

In Dec last year, 2 weeks after I wrote about CW Group (HKEX: 1322), it went into trading halt for a week before trading is resumed with the announcement of a very significant acquisition. See: CW GROUP: At distressed valuation, upside potential significant if...

Upon resumption of trading, the market took the news well, and the share price soared to an intra-day high of HKD 1.76 before closing at HKD 1.48. |

||||||||||||||||

Zuse Hüller-Hille

According to the CW announcement, the brand Zuse Hüller-Hille “has a long operating history in the machine tools industry and can be traced back to 1923, when it was founded by Dr. Karl Hüller in Germany. It focuses on the development and manufacture of premium quality machine tools with a product portfolio which includes horizontal 4 and 5-axis machining centers, as well as the vertical center NBV 700 in modular design.”

That statement is misleading because Zuse Automation was only founded in 2016 by the current CEO Ralph Christnacht. Hüller-Hille is the brand with a long history and it was acquired by Zuse in May 2017 from Fair Friend Group and combined with Zuse Automation. Why is Ralph Christnarcht so important that CW deemed it fit to emphasize that Mr Christnacht will continue to lead for at least 3 years after the acquisition?

Mr Christnacht is no lightweight in the machine tool business. He was the CEO of DMG Mori AG from Aug 2013 to Dec 2015. DMG Mori AG is the German subsidiary of DMG Mori, one of the largest machine tool manufacturer in the world.

CW has until 31/9/18 to complete their due diligence, but it is almost certain that this deal will go through. That’s because CW and Zuse have a working relationship since at least 26/8/16, where both parties signed a MOU to secure turnkey automotive and precision engineering projects in Germany. Apparently, that relationship worked out well, because in an interview in June 2017, Mr Christnacht called CW Group his longtime business partner. The interview can be found here.

The same paragraph sheds much light on why CW’s growth has slowed since 2015, and the Google translated version says: “CW has represented many brands in Southeast Asia over the past few years. Due to the change in the strategy of the producers to direct sales, they suddenly had no more products to sell. Two years ago, they approached me and said they need a German machine tool brand to do something themselves. My idea was that we would need a good brand name.”

It is quite clear from CW’s disclosures that they act as consultant to their customers and distributor on behalf of other brands. Their manufacturing capability is not extensive because the value of plant and equipment in their book is merely HKD 8.2m. This acquisition, if successful, will likely be a game changer for them because they will be acquiring manufacturing capability through Zuse Hüller-Hille’s manufacturing plant in Mosbach, Germany. Zuse Hüller-Hille’s manufacturing plant in Mosbach

Zuse Hüller-Hille’s manufacturing plant in Mosbach

A potential proxy to Asian aerospace?

Zuse Hüller-Hille took part in EMO (Exposition Mondiale de la Machine-Outil) 2017 in Hanover. EMO is an European trade show for the manufacturing industries. In the company blog (http://blog.zuseautomation.com/ ), the company showcased its capability in manufacturing the casing of an aircraft engine.

Watch video of the exhibition -->

For keen readers of Singaporean and Malaysian business news, the exhibit should stir some excitement because aerospace is a sector both governments are trying to stimulate. Singapore is particularly successful in attracting aerospace majors to its Seletar Aerospace Park. At the same time, many aerospace majors are moving closer to where their customers are, notably China and South East Asia.

There are two companies in Malaysia that manufacture engine casing -- SAM, which supplies to GE Aviation and Pratt And Whitney; and UMW, which supplies to Rolls Royce. It is not easy to make these parts. UMW, in particular, spent RM750m over a span of 2 years to build a dedicated facility. It is challenging to manufacture these parts because 1) they are large and very precise and 2) titanium/titanium alloy are hard to machine.

Aerospace is a discipline requiring a high degree of precision. Unlike other engineering disciplines, over designing is not a virtue, but a vice because it results in unnecessary weight, weight that costs airlines money through fuel burnt over the 20 years or so of service life to haul the extra weight. As a result of that, aircrafts are designed to perform within a narrow band, and hence the high degree of precision.

Among others, the engine/casing is one of the most precise parts of an aircraft. The efficiency of the engine/turbine is a function of the clearance between the tip of the blade and the casing. The ability to machine the casing to a very high precision enables this clearance to be minimized. If titanium alloy is chosen, it compounds the difficulty in achieving the needed precision.

The point about the discussion on engine casing is to differentiate Zuse Hüller-Hille from other machine tool makers. I believe they serve the premium, high tech market. I do not think they are big, because in the acquisition announcement, it is revealed that their order book is just EUR 40m for 2018. To compensate for size, they need to carve a niche for themselves and I believe they are quite capable of doing so.

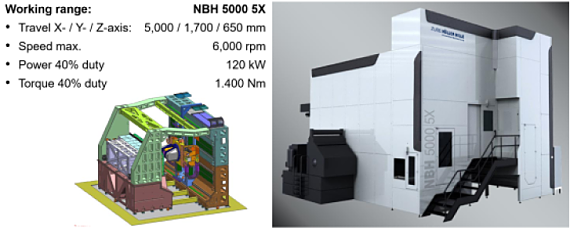

In the interview with Mr Christnarcht, he talked about a NBH 5000 that is used to machine aerospace titanium structural parts. Somehow, this tool cannot be found on their website. After some digging, I’ve managed to find it in their aerospace specific brochure through the company blog: http://blog.zuseautomation.com/built-to-fly/. The NBH 5000 looks like this and it is indeed a monster:

I have also noted 2 other evidences of CW’s link to aerospace in my first article:

- CW had placed out 15% of its share capital to Shenzhen Hua Hang Xin Investment Center Limited Partnership, an investment vehicle linked to AVIC (or Aviation Industry Corporation of China),

- iFast’s bond review report “Are CW Group’s New 7% 3Y Bonds Attractive?” revealed that CW serves well known aerospace companies such as Rolls-Royce, Honeywell and Hamilton Sundstrand.

Valuation of the acquisition

The acquisition of Zuse Hüller-Hille comes with a profit guarantee of EUR 11.5m. If that target is met, CW will shell out EUR 126.5m for the acquisition. That works out to be PE of 11. Unfortunately, there is no information on the balance sheet of the target, therefore a more sophisticated peer comparison cannot be carried out.

|

|

Share price |

PE (ttm) |

Annualised PE latest report |

Revenue (ttm) |

EV |

EV/EBIT |

|

Zuse Hüller-Hille |

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Tsugami |

JPY 1,457 |

22.7 |

23.0 |

HKD3.9 b |

HKD 5.5 b |

13.9 |

|

Makino |

JPY 1,090 |

14.3 |

13.9 |

HKD12.1b |

HKD 9.1 b |

10.11 |

|

DMG Mori |

JPY 2,140 |

18.5 |

8.1 |

HKD32.4b |

HKD 36.7b |

20.16 |

|

|

|

|

|

|

|

|

|

CW Group |

HKD 1.25 |

3.7 |

5.4* |

HKD2.5 b |

HKD 1.3 b |

6.22 |

# Market cap and EV for Tsugami, Makino and DMG Mori is converted from JPY to HKD for comparison.

* Excludes gain on repurchase of note HKD 7.7m and forex gain HKD 15.4m.

When compared to 3 machine tool manufacturers listed in Japan, the acquisition does not appear to be expensive. CW Group looks dirt cheap, although its revenue is smaller.

The acquisition price of EUR 126.5m is equivalent to HKD 1.2b, which is higher than CW’s market cap at HKD 899m. This prompted a few comments about 蛇吞象, literally "snake eat elephant", or biting off more than it can chew. I believe this is a fallacy because a close examination of CW’s balance sheet indicates that they have the financial muscle to carry out the acquisition.

On 30/6/17, it has:

|

Escrow fund |

HKD 336,402,000 |

|

Trade receivables |

HKD 2,269,740,000 |

|

Cash |

HKD 143,011,000 |

|

Less |

|

|

Trade payables |

HKD 981,971,000 |

|

Debt |

HKD 542,641,000 |

|

Net |

HKD 1,224,541 |

Of course, CW cannot deplete its working capital entirely for the acquisition, but considering its net gearing is only 0.22, there is still headroom to gear up. The acquisition appears unusually big because CW is trading at distressed valuations of 0.48 price to book and 3.7 trailing PE. If they are to trade at a valuation typical of machine tool makers shown in the table above, it would not attract such skepticism.

CW has indicated they have sufficient funds to meet the payment for tranche 1, representing 60% of the target company, but may need to tap borrowings or equity raising to meet tranche 2 for the remaining 40% of the target company. So, investors should be prepared for a rights issue should management find it necessary to call for one.

|

Risks

|

Choo Chi Fei, Nicholas Oh and Kok Li Ong contributed to this article.