Photo: Andrew Vanburen

Cinda Research: BAOFENG Still ‘Buy’ on 2011 results

Cinda International Research said it is reaffirming its ‘Buy’ recommendation on Baofeng Modern (HK: 1121) thanks to its strong full-year 2011 results, and it's maintaining the casual footwear maker’s target price at 2.2 hkd.

“We recently met Baofeng Modern’s management after the results announcement and they gave color on the expansion strategy as well as their FY12 outlook. Their FY11 results showed a growth strategy on track. The results confirm the company’s right direction,” Cinda said.

Branded products accounted for 51.7% of overall sales, up from 37.7% in FY10.

Meanwhile, overall GPM edged up to 33.4% from 33% a year earlier, with Boree and Baofeng branded products both recording a rise of 0.5-0.8 ppt.

Baofeng’s distribution network rose impressively to 908 by end-2011, up from 520 as of end-2010.

“The only surprise to us is the reduction of OEM volume by 17% y-o-y (but sales volume rose by 5.6%), which is nevertheless consistent with the company’s growth strategy. Its rapidly rising distribution network will drive sales of branded products,” Cinda added.

Management told the research house that the newly increased network includes major supermarket chain stores that were signed up during late-2010 to 2011, such as Carrefour, Tesco, RT Mart and Xinhuadao.

“These led to an 83% rise in volume sold of branded products. Furthermore, the Hong Kong shop has just opened, likely followed by The Philippines and Indonesia by end-1H12, all focusing on the sale of branded products.“

Management indicated the cost of high-end EVA plastics rose by 10-20% during FY11 (accounted for 30% of COGS, by Cinda’s estimates).

“Yet GPM in the two branded lines still rose, reasons being the optimization among different kinds of plastics and product mixes, management indicated. Also, they are confident that GPM would continue edging up in FY12 driven by ASP hikes.”

The NBA branded products were rolled out in 2011, backed by their sole official authorization rights in China.

“The selling of SpongeBob, Swarovski, and FashionTV featured products in FY12 will also help the company to reach out to different consumer groups which in turn will likely stimulate the expansion of its distribution network,” Cinda said.

See also:

OSK Stays ‘Buy’ On BAOFENG; BOCI Cuts CHOW SANG SANG Target

MISS ASIA Contestants Lend ‘Hand’ To China’s Top Slipper Play

BAOFENG: Aiming To Crystallize New Orders With Swarovski

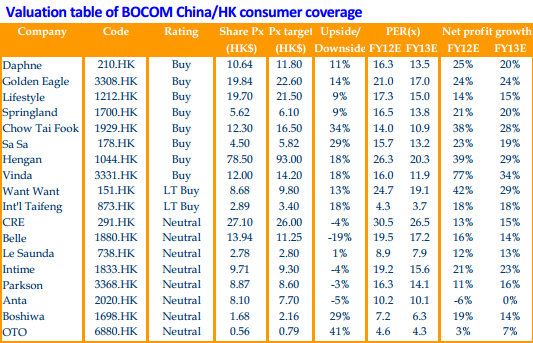

Bocom: PRC CONSUMER stocks 2011 results ‘mixed bag’

Bocom says PRC consumer stocks listed in Hong Kong are a “mixed bag” after a wide range of 2011 earnings.

“The FY11 results of the China consumer sector were a mixed bag. Among the key segments, ladies’ footwear and department stores in general reported in-line earnings, while supermarkets were disappointing due to the higher margin squeeze,” Bocom said.

The research house added that for consumer staples, F&B was below expectations while the household & personal care segment was above.

“Among key stocks, Daphne (Buy) beat most, followed by Want Want.

"On the contrary, PCD Stores missed the most, followed by Sun Art, Intime and Tingyi.”

Overall, the FY11 net profit growth of the retail sector was 34% (or 30% ex-sportswear) and staples were flat.

“We kept our recommendations unchanged, except for earnings upgrade on Daphne and Vinda, and an earnings downgrade on Anta. We continue to have a divided view on the different sub-segments due to the sector's reducing resilience amid the slowing consumption growth outlook.”

Bocom added that its “key buys” in the consumer sector are Daphne, Golden Eagle, Want Want, Hengan, Chow Tai Fook, SaSa, Lifestyle, Vinda and Springland.

“Daphne remains our footwear top pick due to its more resilient growth story, with margins continuing to serve as the key upside surprise as its stringent operating revamp efforts increasingly pay off.

As for consumer staples, Bocom said the sector results were mixed, with net profit ranging from 28% growth (Mengniu) to a 40% decline (Uni-president) and a net loss (BaWang).

“Hengan remains our top sector pick due to its best-in-class track record and accelerating margin expansion along with enhanced market leadership. We also favor Vinda, which is a direct beneficiary of capacity building and cheaper pulp prices in 2012E.”

See also:

Houses Hike XTEP To ‘Outperform’, 'Buy'; GIORDANO Target 15% Upside

XTEP Orders Lead Sector

XTEP: In It For The Long Run With Marathon, Social Media

Sorry for the side track but maybe someone should do a proper in depth study or investigations into the complex transactions involving the Yoma "web of triangle". On the surface, there appears to be some parrallel to the Pan-El affair in the eighties, cross dealings between companies in the same grouping which inflated the value of some assets during intra-transfers, etc. I don't know whether MAS or SGX or any other relevant authorities have noticed the trend, and if they did, whether detailed in depth analysis have been done. One particular area being Land Development Rights or so called LDRs (which does not bear any title to the land) - what do they really mean. Technically, it appears there can be more than one "owner" of a particular piece of land at any given time. It looks like the purchasers and individual owners of the finished product (the strata equivalent)may end up owning only the building and not the lot of land that it sits on (just like our HDB owners). Amidst this muddled cloak of web, speculators are jumping in at full steam, not knowing what LDRs really are and who actually has title to the land. At one point Serge Pun's SPA is implied to be owing the LDRs, at other time owning the plots of land, and yet at another time said to be the managing agents of the land/projects, etc. As for me, I am staying clear of this counter !