SHENZHEN INVESTMENT Ltd (HK: 604) is fully aware of the pitfalls of overextending debt to ratchet up land banks in China’s property sector, saying it has a much more prudent expansion plan than financially distraught Greentown Holdings.

An SZI official said the developer currently has a net gearing of 51% which “will never be allowed to exceed 70%.”

The residential property-focused developer hopes this financial discipline will help to turn around its Hong Kong shares, which are near 52-week lows.

Shenzhen Investment Senior Manager of Investor Relations Nicole Zhou told investors in Shenzhen that the company was intent on balancing its books and keeping its borrowings within a tolerable level.

“We think that any gearing rate over 70% is unhealthy and unsustainable. We put a premium on maintaining good, safe balance sheets,” Ms. Zhou said at the conference sponsored by China Merchants Bank.

In addition, she said that the property developer, which listed in Hong Kong in 1997, has seen healthy top-line contributions, but that the first half of this year saw sales volume somewhat hampered by macroeconomic restrictions from Beijing targeting the housing sector.

“For several years, our revenue has witnessed steady growth. But we are currently exposed at an over 95% rate to the residential property sector so we are striving to boost our commercial property holdings.”

She said management had five primary targets over the next few years: property sales will reach 10 bln yuan in two years and 25 bln yuan in five years, with sales in Shenzhen and the Pearl River Delta to account for 70% of the total; an over 305 gross margin by 2012; a "steady" land bank of 10 mln square meters with 60-70% in Shenzhen and the Pearl River Delta; a "stable" dividend payout ratio, and most importantly... a net gearing ratio under 70%.

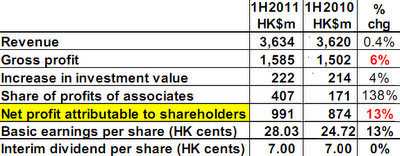

In the first six months of this year, Shenzhen Investment’s top line ended flat on a year-on-year basis at around 3.6 bln hkd.

However, net profit rose a respectable 13% to 991 mln hkd, realizing a net profit margin of 27.3%, up 3.2 percentage points from a year earlier.

How did the Hong Kong-based developer with an 18,000-strong workforce manage to boost profitability in such a policy-unfriendly climate?

“Good assets,” was Ms. Zhou’s reply.

Contracted sales for the January-June period fetched three bln yuan, or an encouraging 64% of the full-year contracted sales target, which prompted the company’s board to declare an interim dividend of seven HK cents per share.

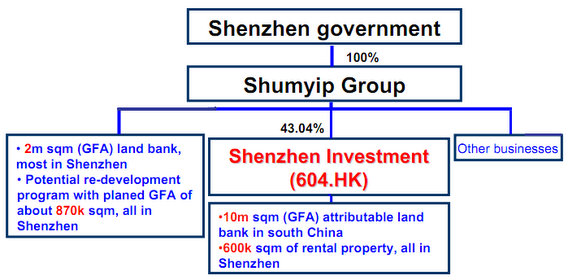

A mid-market property developer in southern China, Shenzhen Investment is 43.1%-owned by Shenzhen’s city government.

However, at least ostensibly, the company did not derive any policy-side benefits from its close association with City Hall in its namesake town.

“We don’t enjoy any special treatment because of this relationship. All property developers are required to comply with sector adjustments from Beijing,” Ms. Zhou said.

Shenzhen Investment's current land reserves totaled around 10 mln square meters (GFA), of which 1.6 mln are classed as under construction.

The Hong Kong-listed developer also holds approximately 600,000 square meters (GFA) of investment properties at prime locations in Shenzhen, with the remainder primarily in surrounding Guangdong Province.

“In addition to providing stable rental income, these investment properties also have potential for redevelopment.”

Ms. Zhou added that as Shenzhen Investment is heavily exposed to the residential property sector, it is not immune from the series of measures targeting the sector passed down from market regulators in Beijing.

“Regulations targeting the housing sector, including the one-per-customer limit and the rule on having a certain percentage of a development of a smaller, cheaper square meterage, naturally do impact our operations like everyone else. However, we do manage each property and regulatory shift on a case-by-case basis,” she said.

When asked if Shenzhen Investment looked to some of its more leveraged rivals as warning signs of how not to do business, she said the firm followed its own path, but also kept a close eye on telling trends in the sector.

“We’re no Greentown (Holdings) as we believe developers with some state-owned structure are inherently more stable.”

Shenzhen Investment also provides passenger & freight transportation services, automobile maintenance and other related services. In addition, it manufactures and sells industrial, commercial, and steel products, as well as aluminum alloys, and also operates warehouses.

But it would remain fundamentally a property developer going forward.

And how did Shenzhen Investment see the property market – housing and commercial – down the road?

“We expect the first half of 2012 to be somewhat difficult for the property sector with prices seeing little upside drivers. However, there may be some loosening policies in the second half which will both help boost prices and ease up credit availability,” Ms. Zhou said.

Mr. Lu Hua, President of Shenzhen Investment, said earlier this year: “During the first half the central government regarded consumer price stability as the primary task of its austerity measure and exerted escalating stringent measures to regulate the property market. Facing an unfavorable market environment, we focused our efforts on accelerating property sales, ensuring safety of funds and strengthening internal controls, thereby being able to maintain a steady development momentum.”

He added that as of the end of July, the amount of sales income contracted but not booked was approximately 2.8 bln yuan.

“Our diversified land reserves are sufficient to meet the development needs in the next five to six years,” Mr. Lu said.

See also:

OCT ASIA, SUNAC CHINA: Chasing Hot Properties

HOUSE OF CARDS? Spring Long Way Off For China Property Market

GREENTOWN Chairman, How Can You Face Shareholders?