Excerpts from latest analyst reports.....

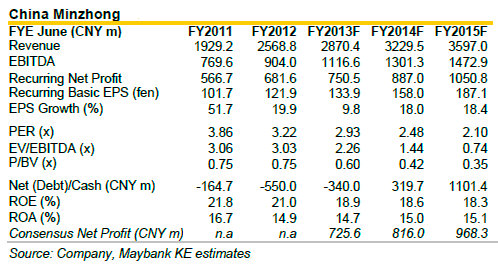

Maybank KE says 'big overhang removed' from China Minzhong

Analyst: WEI Bin

Olympus Capital, a private equity fund, has sold its entire stake of 57m shares in China Minzhong through a private placement last Thursday at SGD0.80 per share.

In our view, this placement is a positive for Minzhong as it removes a long-term share overhang on the company without adding too much selling pressure in the open market.

Ø In a show of solidarity, management took advantage of the vendor share placement to increase personal stakeholdings. This clearly signals management’s confidence in the company’s fundamentals and the attractiveness of its share price.

Ø We continue to like Minzhong for its growth prospects. We are looking at an average of 15% EPS growth for the next three years. As it stands, Minzhong’s share price is deeply undervalued at the current 2.9x FY13F PER. Reiterate BUY with the target price unchanged at SGD1.16.

Recent story: CHINA MINZHONG gets new big shareholder, AUSGROUP price is up, JEL's ex-CEO sells down

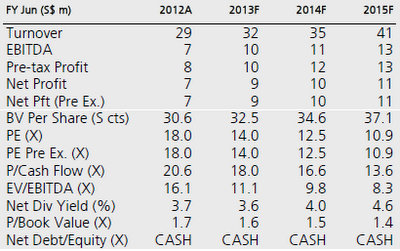

DBS Vickers highlights Cordlife's "stable recurring income"

Analysts: LING Lee Keng & Andy SIM

• Larger of only two private cord blood banks in Singapore; among the top 3 in Hong Kong

• Increasing penetration rate and awareness of cord blood banking to drive growth

• Stable recurring income; potential acquisitions in Indonesia, India and Philippines

• Fair value of S$0.65 offers 21% potential upside

Fair value S$0.65. The stock current trades at 14.0x FY13F PE.

We believe a target PE of 16x based on a slight (<10%) discount to blended forward PE of its peers is reasonable, given its shorter trading history. This translates to a fair value of S$0.65, which offers potential upside of 20% from current share price.

Key risks include reputational risk. Any problem with the quality of its cord blood banking services will be extremely detrimental to the Group.

Recent story: GLOBAL PREMIUM HOTELS, AURIC PACIFIC, CORDLIFE: What analysts now say....

Comments