SEVERAL LARGE CAP PRC listcos have managed to shake off the collective blow to investor confidence ushered in after the world’s three leading rating agencies all issued warnings about questionable management and auditing irregularities in Mainland Chinese firms.

To what extent is the resilience market-based versus psychological?

A Chinese language report in Sinafinance said that Fitch this week joined S&P and Moody’s as the latest global ratings agency to issue either a warning or downgrade on Mainland China’s currency outlook or its listed firms.

Fitch, following the lead of Moody’s earlier this month, said that three heavy hitters among a list of 35 “at risk” PRC listcos were of particular concern due to questionable practices and policies by senior management.

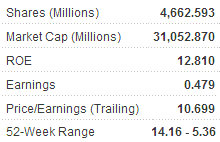

They are Asia’s largest containerboard manufacturer Nine Dragons Paper Holdings Ltd (HK: 2689), GCL-Poly Energy Holdings Ltd (HK: 3800) and China Medical Technologies Inc (Nasdaq: CMED).

The ratings agency added that the three may come to find capital markets unwilling to support them due to “escalating corporate governance concerns.”

Moody’s got the ball rolling last week, issuing a warning on 61 “red flag” companies it judged as practicing “risky or opaque” operating models, poor quality earnings and cash flow, and concern over the accuracy and transparency of recent earnings statements

This was piggybacked by Fitch this week in the form of a risk alert on the 35 listcos.

John Hatton, Asia-Pacific corporates group credit officer at Fitch, said: "International investor interest in Chinese companies, driven by high levels of growth and the search for yield, is coinciding with limited access to information at key issuing entities," adding that access to funds is stressed when investor confidence is compromised.

Fitch went on to say in its report this week: “When reviewing a company's corporate governance practices, investors should be alert to concentrated private ownership and independent directors staying on boards for longer than five years.”

Despite Mainland China now being the world’s second biggest economy and claims that it is still a “developing country” are somewhat laughable, Fitch said that the country's capital markets remained far behind the industrialized world in terms of corporate governance and auditing authenticity.

“Therefore, in such areas as accounting and transparency, enterprises will exhibit various weaknesses, and boards of directors will inevitably have a wide range of shortcomings -- both financial and accounting-related. These are likely to continue in the short term, thereby affecting parts of corporate financing.”

Among the 35 PRC-based companies “named and shamed” by Fitch, 27 are H-shares – Chinese firms selling shares in Hong Kong.

Counted within their ranks are a good number of large-cap blue chip firms in critically important sectors like petrochemicals and telecommunications.

On Thursday, key companies on Fitch’s list performed relatively in line with the market.

While CNOOC Ltd (HK: 883) fell 3.55% to 16.86 hkd, other heavy hitters seemed to shake off the latest bad news from foreign ratings agencies.

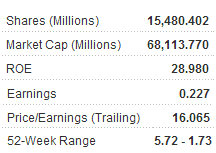

China’s top aluminum producer Chalco (HK: 2600) shed 1.45% to 6.12 hkd, major electricity generator Huaneng Power International Inc (HK: 902) edged down 0.25% to 3.94, Datang International Power Generation Co Ltd (HK: 991) fell 1.15% to 2.57, IT network infrastructure giant ZTE Corp (HK: 763) lost 1.95% to 25.1 and China Telecom Corp Ltd (HK: 728) closed down 1.73% at 5.12.

These are hardly the reactions of psychologically devasted firms.

An earlier warning on local debt accumulation and currency ratings re-rating possibilities by global agency S&P also failed to significantly shake the market.

Despite the deluge of “blacklists” and warnings directed at PRC-based firms either selling A shares in Mainland China or listed in Hong Kong as “red chips,” even a cursory look at the share performance of the companies named by the rating agencies reveals that the post-report downside is far less drastic than would ordinarily be expected.

And concerns voiced recently by Deutsche Bank and Morgan Stanley in separate reports on property and financial sectors in Mainland China also failed to ruin the party.

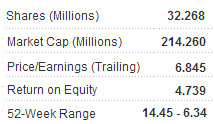

Major lender China Merchants Bank Ltd (HK: 3968) added 0.11% yesterday to close at 18.46 hkd despite the two new reports.

What all this means in terms of the "real versus perceived" importance of re-ratings or warnings by foreign rating agencies has yet to be proven convincingly.

But one thing is for sure. The days of old when a bad report or a downgrade meant curtains (whether short or long term) for Chinese firms seems to be increasingly a thing of the past.

That being said, investors would be ill advised to ignore such reports and re-ratings outright, but instead should closely monitor newsflows and share price movements immediately after the release of such reports.

YANGZIJIANG, PRC INTERNET STOCKS, CHINA FLOORING: What Analysts Now Say...

CHINA HIGH PRECISION: HK Listco’s 1H Off Charts On Indicator Sales