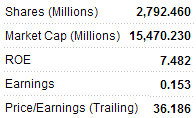

Daiwa upgrades CHINA FOODS to ‘Buy” on more potent wine margins

Daiwa Capital Markets has upgraded China Foods (HK: 506), a major PRC-based supplier of wine, edible oils and confectionary, to ‘Buy’ from ‘Hold’ and hiked the target price to 6.00 hkd from 4.75 on expected strong performance in the wine retailing sector.

Daiwa expects China Foods -- which has the Great Wall wine brand under its umbrella and is one of three bottling partners of Coca-Cola in China – to enjoy wine business EBIT margins of 18.5% in 2011 versus 11.7% in 2010.

The brokerage said it upgraded China Foods for three reasons: 1) profitability of the wine business is expected to recover in 2011, 2) the new managing director has a good track record in the beverage business, and 3) the negative factors weighing on the company have already been reflected in the price.

“Our new target price equates to a PER of 20x on our revised 2012 EPS forecast. We have revised up our 2011-12 EPS forecasts by 8-23% to reflect our reduced operating-expense forecasts for the wine segment. We forecast EPS to rise at a CAGR of 31% for 2011-13,” Daiwa added.

See recent: SUPER, BIOSENSORS, COSCO: What Analysts Now Say...

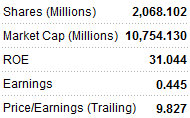

Haitong says ‘Buy’ TRINITY on stronger profitability expectations

Haitong says it is maintaining its ‘Buy’ on Trinity Ltd (HK: 891) and keeping the target price at 9.52 hkd after the up-market menswear retailer announced strong results, with solid growth expected going forward.

Given the strong FY10 results and pleasant growth prospects, it is raising is earnings forecasts by 8% and 7% for FY11-12 and now expects a 20% top line and 28% bottom-line CAGR for FY10-13.

The moderate valuation premium compared to other menswear retailers is justified by Trinity’s well-positioned brand equity, transparent strategies in China’s luxury market and proven management capability.

Trinity’s FY10 bottom line surged 90% to 341 mln hkd, 8% ahead of Haitong's estimate. Revenue experienced 22% growth to 2.0 bln, owing to the remarkable 21% same-store-sales growth.

Hong Kong and Macau continued to be primarily driven by increased sales to tourists from the mainland. An improving economic backdrop in the greater China region also bolstered consumer spending on luxury goods.

The company’s four core brands, Kent & Curwen, Cerrutti 1881, Gieves & Hawkes and D’URBAN, also saw solid development in FY10. Margins significantly improved with outstanding execution, higher store productivity and enhanced operating leverage.

Going forward, Trinity will continue to penetrate second, third and fourth-tier mainland cities at a moderate pace, with second-tier cities having more stores, but third and fourth-tier cities in greater abundance. China is expected to become the world's largest consumer of luxury goods by 2015, accounting for more than 20% globally.

See recent: CHINA HONGXING: Things Are Not As Bad As They Appear?

BOCOM ‘Buy’ on INTIME on strong 1Q

BOCOM said it is staying ‘Buy’ on Intime Department Store (HK: 1833) with a 13.9 hkd target price (25.2% upside) thanks to 1Q same store sales growth (SSSG) of 27.2%.

First quarter gross sales proceeds were up 38.4%, surpassing BOCOM'S expectations. Intime delivered a strong set of 1Q11 sales figures which beat expectations and management’s indication of 25%+ SSSG in FY10.

Not only young stores opened in 2008 and 2009 showed strong SSSG momentum. For example, the Hangzhou Qingchun Store was up 47.6%, Jinhua Intime World rose 100.1%, Yiwu Yimei Store was up 72.7% and Jinhua Futailong Store jumped 52.1%. The mature stores also delivered impressive high-teen SSSG, with Hangzhou Wulin Store up 18% and Ningbo twin stores up 18.6%.

Raise FY11F/FY12F EPS by 1.4%/1.8%, respectively Major changes: (1) upward revision of FY11F and FY12F SSSG and GSP; (2) upward revision of share option expense in FY11F and FY12F. BOCOM expects Intime to deliver 36.3% CAGR of FD Core EPS from FY10F to FY12F. Such a growth rate is the highest among peers under its coverage.

BOCOM likes Intime’s young store portfolio (average store age is 3.8 years at the end of 2010) and its less risky expansion strategy by new store openings, cooperation with local players and M&As to increase market share in Beijing, Hubei and Anhui markets.

See recent: POST-CRISIS: Short-Term Investing Mindset, Understating Opportunities

Hani says ‘Buy’ 361 DEGREES, 5.7 hkd target

Hani Securities is staying ‘Buy’ on athletic footwear and apparel firm 361 Degrees (HK: 1361).

361 hopes to recoup its recent retracement, and is poised to resume an upward trend.

Retailers are gaining strength on buying interest from Chinese investment institutions.

Hani says near-term resistance is at the 5.27 hkd level and support at the 4.93 level.

361 Degrees International reported July-December 2010 revenue rose 29.5% year-on-year to 2.28 bln yuan, modestly faster than the overall growth trends of the sportswear segment and the overall retail sector in China.

Net profit was 422.78 mln yuan or 20.4 cents per diluted share compared to 356.75 mln or 17.3 cents per basic and diluted share the year earlier.

361 Degrees designs, manufactures and distributes sporting goods in the PRC.

Its sporting goods include athletic footwear, apparel and accessories, distributing its products through nearly 6,000 authorized retailers that are owned and managed by 30 distributors.

The firm was established in 2002, and 361 Degrees was the official sportswear of the Chinese Men's and Women's Olympic curling teams during the 2010 Vancouver Olympics.

361 is headquartered in Jinjiang City, Fujian Province, and has exclusive sponsorships with a wide range of well-known athletes.

See recent: XTEP 2010 Net Up 25.7%: What Analysts Now Say...