This article was published recently on Ernest Lim's blog and is reproduced with permission. IN FEBRUARY, I wrote on China Sunsine (CHINA SUNSINE: Expect positive results going forward!), pointing that it may be on the cusp of a recovery.

IN FEBRUARY, I wrote on China Sunsine (CHINA SUNSINE: Expect positive results going forward!), pointing that it may be on the cusp of a recovery.

Since then (Sunsine closed at $0.255 on 21 Feb), it has surged 36.7% (inclusive of a dividend of $0.01 during the period) to touch an intraday high of $0.335. It closed at $0.310 last Friday.

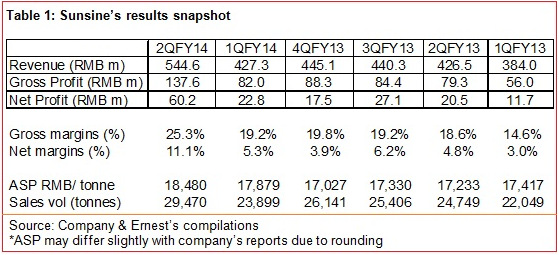

Sunsine’s 1HFY14 net profit exceeds the entire net profit earned in FY13

Based on Table 1 below, Sunsine seems to be turning around with 2QFY14 sales and net profit up significantly from the previous few quarters and on a year-on-year comparison.

What is interesting is that 1HFY14 net profit has exceeded the net profit earned in the entire 2013. This good set of results is on the back of an increase in ASP as well as sales volume.

3QFY14F looks bright on several aspects

The upcoming 3QFY14F looks bright in several aspects.

Firstly, according to brokerage 中信建投证券, the supply of MBT, an intermediate product necessary for the production of MBT-based accelerators, dropped more than 30% as some MBT producers were forced to close down or suspend production due to their inability to meet the environment standards set up by the Chinese authorities.

As MBT prices rise, so do MBT-based accelerators. China Sunsine has its own factory for producing MBT, and has been compliant with the environment standards, hence its production is not affected.

Secondly, the accelerators’ inventory levels in China have been reduced due to an increase in the export of accelerators.

The trend of relatively high prices of accelerators is unlikely to ease in the near term as companies need time to rebuild / improve their production facilities and comply with environment standards. In addition, China is likely to maintain its resolve in reducing pollution, especially with the upcoming APEC meeting in November.

Thirdly, raw material prices for producing accelerators continue to be stable, hence they are unlikely to have a significant adverse impact on its upcoming 3Q results.

Sunsine has paid $0.01 / share as dividends for seven consecutive years

For seven consecutive years, Sunsine has paid $0.01 / share as dividends. At Friday’s closing price of $0.310, this represents a dividend yield of 3.2%. There may be scope for higher dividends as Sunsine's 1HFY14 net profit has already eclipse that of FY13.

Stark discount to its Chinese peer

Sunsine trades at 0.8x P/BV and annualised 2014F PE of around 4.3x. Net asset value per share is around $0.380. On a historical basis, Sunsine trades at an average P/BV and P/E of around 1.0x and 7.3x, respectively.

With reference to Figure 1 below, it is noteworthy that its peer, Shandong Yanggu Huatai Chemical (“YGHT”), trades at 35x FY14F PE and 4.6x FY14F P/BV. Furthermore, YGHT’s estimated FY14F revenue and net profit are lower than Sunsine’s 1HFY14 figures.

Figure 1: Analysts’ estimates of YGHT’s financials in the next 3 years

Note the strong growth in sales and profit that analysts are forecasting for Shandong Yanggu Huatai Chemical in FY2014 through to FY2016. Source: Bloomberg as of 25 Aug 14.

Note the strong growth in sales and profit that analysts are forecasting for Shandong Yanggu Huatai Chemical in FY2014 through to FY2016. Source: Bloomberg as of 25 Aug 14.

|

Investment risks Illiquidity Average 30D and 100D volume amount to 1.3m and 557K shares, respectively. Although this is still pretty illiquid, it has improved from my last writeup when the average 30D and 100D volumes amounted to 1.19m shares and 422K shares, respectively. This is a Chinese company helmed by Chinese management, hence the usual S chip risk applies. No analyst coverage According to Bloomberg, there is currently no rated analyst coverage on this stock. It is reasonable to say that the investment community is not familiar with Sunsine yet. However, there seems to be more interest in this counter as I have started seeing unrated reports on Sunsine and online forums where they talk more about Sunsine than before. Exposed to the vagaries of the automotive industry cycle As Sunsine’s products are used mainly by tyre manufacturers, Sunsine is exposed to the vagaries of the automotive industry cycle in China. For 1H2014, China’s auto sales rose 11% year-on-year to 9.1m. A significant slowdown in China’s automotive market is likely to have an adverse impact on Sunsine. Margins dependent on raw material cost Most of its cost of sales come from direct raw material costs, namely aniline. According to Sunsine’s AR2013, ceteris paribus, every 10% increase / decrease in the price of aniline would have decreased / increased net profit by RMB30.1m in FY13. As such, raw material costs do play a significant aspect in Sunsine’s profitability. As mentioned above, aniline prices have remained pretty stable since the start of the year. |

Other developments

Sunsine is on track to complete its new heating plant by 3QFY2014. This may incur additional costs but it is likely to be an interesting cash flow generating investment over the medium term. See my previous writeup for more information on this.

Sunsine’s chart analysis

China Sunsine (31 cents) has a trailing PE of 5.6X, dividend yield of 3.23% and a market cap of S$149 million. Chart: Bloomberg.Since my writeup (Sunsine closed at $0.255 on 21 Feb), it has surged 36.7% (inclusive of a dividend of $0.01 during the period) to touch an intraday high of $0.335. It closed at $0.310 on last Friday.

China Sunsine (31 cents) has a trailing PE of 5.6X, dividend yield of 3.23% and a market cap of S$149 million. Chart: Bloomberg.Since my writeup (Sunsine closed at $0.255 on 21 Feb), it has surged 36.7% (inclusive of a dividend of $0.01 during the period) to touch an intraday high of $0.335. It closed at $0.310 on last Friday.

Sunsine has closed the gap around $0.290 – 0.310 as it weakens from $0.335 on 7 Aug. It seems to have just formed an upside break in the flag formation.

However, we have to monitor how the price performs in the next few days. A sustainable upside breakout above $0.305 with volume points to a measured eventual technical target of around $0.365.

Supports and resistances are as follows:

Supports: $0.300 / 0.290 / 0.275

Resistances: $0.320 / 0.330 - 0.335 / 0.350

Conclusion – FY14 likely to be a record year for Sunsine

Sunsine seems to be in a sweet spot and FY14F may well be a record year for it. Nevertheless, as there is no rated analyst coverage on this stock, it may take time for the market to appreciate it.

Notwithstanding the positive points about Sunsine, readers should note that this is an S chip which is subject to S-chip risk, fluctuations in raw material prices and the vagaries of the automotive industry cycle in China. Readers who are interested should take a look at the company's website and email me at

Recent story: CHINA SUNSINE to benefit from long-term pollution clampdown