Following our recent article YONGNAM: Analysts give it thumbs up but stock is stuck, a NextInsight reader and shareholder with a significant holding of Yongnam stock arranged for us to meet the Yongnam CEO for an update on the business.

As background, Yongnam Holdings (market cap: nearly $300 million) has had a significant role in the construction of many iconic projects such as the Sky Park at Marina Bay Sands Integrated Resort, the Sports Hub and Bangkok International Airport.

We met up with CEO Seow Soon Yong and the finance director, Chia Sin Cheng, at their office in faraway Tuas South. Here are the key takeaways:

1. Orderbook: As at end-2011, Yongnam had S$462 million orderbook and at end-March 2012, $469 million. It has announced S$138 million worth of new contracts clinched in the year to date.

Photo: NextInsight

Yongnam is pursuing $1.3-1.4 billion of work. Going by past perfomance, the success rate for its tenders is about 50% in Singapore and 25% overseas. Overall, it is 33%.

Yongnam hopes to secure more overseas contribution -- in HK (MRT lines and tunnels), Malaysia (MRT line in KL and mining plants) and Qatar (MRT lines ) which will host the 2022 soccer World Cup.

2. More MRT projects in Singapore: Not included in the $1.3-1.4 billion tenders is a massive project which will come up for tender, by year-end -- the Thomson Line from Marina Bay to Woodlands.

Then there is the North South Expressway, which could start to be tendered out by year-end too.

And possibly in 2014-2015, construction of the East Regional Line will start.

In short, there are mega projects for Yongnam to bid for.

3. Strutting assets: Yongnam has the largest strut inventory of 170,000 tons (with a market value of S$270 mln currently) among five suppliers.

Struts are temporary support structures for construction, and considered part of its capital equipment investment.

The struts are used and re-used for projects. How long is their lifespan? Many decades.

4. Gross margin: These are around 20% for structural steelworks and 30% for strutting projects.

5. Working capital: One salient feature is that for structural steelworks, the working capital needs shoot up in the first 6 months when Yongnam books and takes delivery of steel, fabricates it and then delivers to the work site.

It is only after the structure is erected that Yongnam gets to start collecting payment from the client.

You can imagine the intense working capital needs if two projects start at the same time.

6. New leg of business: The iconic projects Yongnam is currently involved in include the Marina Coastal Expressway, the Downtown MRT Line and the Express Rail Link in Hong Kong.

Yongnam will add offshore to its existing businesses of structural steelworks and specialist civil engineering.

"Offshore" covers oil & gas, wind and even mining industries, by Yongnam's classification.

It had a good start in March when it announced it had achieved a structural steelwork contract for the fabrication of steel components for jack-up structures in the offshore sector.

Yongnam is pursuing joint ventures in UK and Germany for steel-related jobs for the wind business. It would involve the construction of the foundation for wind turbines out at sea.

7. Warrants conversion: Yongnam warrants, which expire in Dec 2012, are currently out of the money -- their exercise price is 25 cents but the mother share is only trading at 23.5 cents.

If the stock price does go up beyond 25 cents and all the warrants are exercised, the company will have a cash inflow of about $90 million.

That would come in handy in repaying a $25-million loan coming due (which can be refinanced also), and for any expansion in business.

In particular, the money could be used for a new seafront facility in Johor to facilitate the export of its steel products -- but this would be constructed only if Yongnam clinches significant deals for its nascent offshore business.

The capex for that is estimated at $50 million.

Currently, Yongnam doesn't have a big debt load -- its gearing is a low 0.28 times.

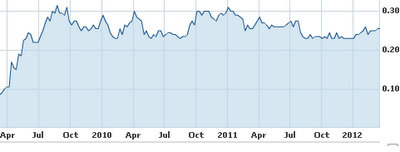

8. Stock price: Recently trading at 23.5 cents, it has been in a tight trading range for the past three years.

Despite the lack of capital gain, the stock is viewed by some investors as being safe: its NTA is 24.1 cents and PE, 4X, while supported by a dividend yield of 4%.

The stock price movement has been muted probably because investors are concerned about the potential diultion from the exercise of the warrants. There are 364.7 million warrants outstanding, a significant number compared to 1.25 billion Yongnam shares outstanding.

Citigroup had a buy call on 12 July and target price of 29 cents, noting the strong operating cashflow and a possibly higher dividend to come.

In FY11, the dividend payout was 1 c, or S$12.5m in total vs ~S$100m in operating cashflow in FY10 and FY11.

Comments

I'm betting Yongnam's trading volume will suddenly shoot up over the next few months. This will happen if those holding their near-the-money warrants decide to push up the mother share to prevent the warrants from expiring worthless.

The need for more Infrastructure projects in the pipeline will be positive for the company... Also reasonable dividend yield of 4.3% based on 23 cents.