Translated by Andrew Vanburen from 中國中冶: 值得關注 (中文翻譯, 請閱讀下面)

DIRECTION IN Hong Kong’s capital markets has been hard to get a bead on these days, with speculation frequently blamed for the lack of any solid visibility.

But one thing is for certain: the growing emphasis in the PRC to raise living standards is helping to offset much of the downside from speculation, and MCC (HK: 1618) may be a diamond in the rough.

The sheer number of industries that prosper in a construction-friendly environment is reason for cheer, as nearly all companies benefit from higher wages, an uptick in homebuilding and road construction, and an overall emphasis on investing in a country’s infrastructure.

As expected, recent investment activity has been focused around real estate developers and construction firms, cement plays, as well as electronics – the latter being items that nouveau riche are most likely to snap up with higher paychecks or even a stronger yuan.

But I would argue that shareholders ignore at their peril some of the unrealized talent in the market outside these dedicated themes, and they would do very well to shop around for bargains.

When all eyes are focused like a collective laser beam on a single sector, that is when the phenomenon of diamonds in the rough sitting neglected on the shelf is most likely to occur.

The secret to finding them is concocting a way to divorce yourself from the mass hysteria and hype surrounding the sector du jour, and go off on a solo reconnaissance mission to find less trumpeted treasures.

I would point to a particular case to demonstrate how following the herd does not always work to your advantage.

Over the past three years, Metallurgical Corp of China Ltd (HK: 1618) has both scraped bottom and ascended to lofty heights.

On the surface, MCC is perceived by casual investors to be a pure metallurgical equipment manufacturing play, with its hand also in mineral development. But it also has a key unit that is a big player in the real estate construction business.

Therefore, when the housing bubble looks ready to burst, some have erroneously sought shelter in MCC... to their detriment.

But compared to traditional property developers who must wait an average of three years for projects to progress from groundbreaking to optimal occupancy, the housing construction sector cycle is relatively shorter, typically 18-24 months.

This means the latter enjoys a faster rate of capital circulation, which allows for a more flexible and real-time capability to respond to developments in the broader market.

And of course, this means that investors can enjoy higher potential returns with more jumping off points available.

MCC is therefore somewhat concealed within the residential property building sector in that its activities in this area are not evident from its namesake marquis.

Therefore, I believe that MCC is worthy of a closer look, and offers the potential of supra-par performance for investors going forward.

The fact that 37 cities in the PRC are being targeted by economic regulators to have steel mills located in downtown areas removed far to the outskirts offers tremendous opportunities for MCC, allowing the company’s core metallurgical machine manufacturing business to greatly broaden its lebensraum.

And considering that MCC is planning to expand its resource development operations, this will help add a more high-return albeit slower-cycle aspect to the company’s revenue stream, and facilitate more sustainable growth for the firm via earnings diversification.

MCC is also in bargain territory.

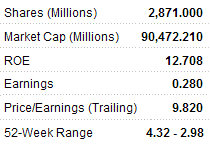

The past three years have seen its share price suffer chronic downturns, even into the beginning of this year until it began to show evidence of a bounceback.

Recently, MCC’s share price has been flirting with the 3.55 hkd level but has once again settled at around 3.3.

See also: PROPERTY: 5 Reasons To Invest In It

中國中冶: 值得關注

(文: 估你唔知)

最近港股表現牛皮,市場尚有明確方向之前,已經見到市場內出現按行業炒賣的局面。

隨著內地近期著重民生,愈益著重國民居住條件,正落實建設大量保障房。

近期投資者正圍繞保障房及周邊的概念,物色到水泥、建築及電器概念股作為主題,但是尚有更多的滄海遺珠,有待投資者發掘。

例如以過往三年股價持續向下的中國中冶(1618),便是一例。

表面上,中冶予外間的感覺,主要以從事冶金設備製造、工程承包、開發礦產資源業務為主,但是原來旗下的房地產部門,亦早已經涉足保障房建設。

由於相比一般房地產發展項目所需周期平均最少三年而言,保障房建設的周期會較短,一般只需18個月至24個月便完成發展,因此這意味資金回籠速度較快,有利中冶的資本運作。

在芸芸保障房概念股中,中冶的潛能,至今仍然未被市場發掘出來。

將來若被人發現的話,這已經足以讓投資者取得較大增值。

況且內地還計劃將37個城市中心的鋼鐵廠遷離核心區域,這亦有助本身在內地幾近處於壟斷地位的中冶,在本業冶金設備製造業務方面獲得更大空間發展。

計及該公司本身亦有參與資源業開發,雖然需時較長才會對中冶帶來較大的貢獻,但是透過在不同業務本身的長、中、短期布局,為往後持續增長,建立較佳的業務模型。

一向以來,中國企業「走出去」已經成為既定方向,中冶亦不例外。

就算最近北非國家因為茉莉花革命,引致當中的主要國家利比亞爆發內戰,致多間中國工程公司在當地承接的工程要叫停,中冶亦屬受影響企業其中之一。這叫人聯想起中冶會否重蹈中國鐵建(1186)在阿拉伯地區面對的問題之覆轍。

不過在當地中冶已經完成工程價值涉資約4.55億元人民幣,但是其按完成進度收款下,實際面對的損失不算太大。

這亦未有影響到中冶在海外的發展大計,將來還要在立足於巴西、印度及澳洲市場,向亞洲、拉丁美洲及非洲等地輻射。

事實上,將來中冶還會參與更多海外項目,爭取回報率須10%以上,加上其亦擬參與澳洲礦商源庫日後來港招股的計劃,這均有助該集團取得更大增值。

中冶在礦業開發方面,據了解回報會更佳,然而開發時間動輒需時四至六年發展。因此需要以長遠的眼光,去看待礦業開發。

該公司的股價在過去三年持續下跌,直至進入今年,其股價終於略為反彈。到最近其股價逼近3.5至3.55元一至三個月高位,到最近稍為回軟。

請閱讀: PROPERTY: 5 Reasons To Invest In It