| Goldman Sachs has initiated coverage on Yangzijiang Shipbuilding with a "Buy" rating and a 12-month target price of S$4.00. The stock rose 6.53% to S$3.10 yesterday (1 Sept). The 26-page report underscores the company's superior margins and returns amid an ongoing industry upcycle, alongside an attractive valuation.

The company, which has been listed in Singapore since April 2007, is described as having "superior efficiency and profitability" as demonstrated by its 13% average net margin over the past 10 years, which is the highest among global peers, largely attributable to its significant cost advantage. Chinese shipyards, including Yangzijiang, benefit from unit operating costs approximately 50% lower than Korean and Japanese peers, a factor driven by lower labour costs and steel price (40% lower) since 2021. Among Chinese listed shipyards, Yangzijiang has consistently recorded the lowest operating costs. |

||||

| Financial Tides Turning: Margins, Orders, and Outlook |

Goldman Sachs anticipates an "earnings boom" stage for the shipbuilding industry from 2025-2028E.

| Best positioned |

| "Best positioned with cost advantages and superior returns: We categorize the ongoing upcycle into two stages: 1) earnings booming in 2025-28E; shipyards to see higher earnings driven by high-ASP orderbooks and lower steel prices; 2) orderbook regaining in 2029-32E; pick up in new ship orders on replacement and stricter decarbonization. "We believe Yangzijiang, the largest non-SOE shipyard in China, is well placed to benefit in the earnings booming stage; we expect 20% EPS CAGR in 2024-28E (peak), with margins (EBIT margin >30%) and ROE (>25%) benefiting from higher-value containership orders and efficiency/cost advantage." -- Goldman Sachs |

This marks a significant increase from its 13% average ROE for the shipbuilding business over the past decade.

New orders for Yangzijiang are expected to "pick up significantly" from 2026.

The company experienced a market share loss in 1H 2025, which the report attributes to its "tighter capacity (3.9-year orderbook)" compared to roughly 3 years for its Korean and Japanese counterparts.

This capacity is expected to free up following its 2025 deliveries, with the new Hongyuan Shipyard projected to add 20% to its current capacity from mid-2026E.

| Navigating Challenges: Trade, Steel, and LNG |

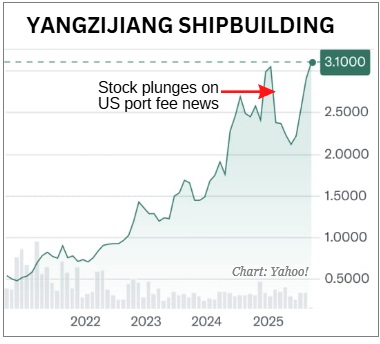

The report addresses concerns surrounding global trade policies, particularly the potential impact of higher USTR port service fees on China-built vessels.

Goldman Sachs believes this impact will be "likely limited", as "non-China shipping operators have the flexibility to redeploy China-built vessels out of the US".

Data from 2024 shows that only 4% of the international fleet calls at the US port were China-built or operated.

Steel prices, which typically account for around 30% of total operating cost in shipbuilding, are a critical factor.

Strategically, Yangzijiang's expansion includes its 51% stake in the JV Yangzi Mitsui (YAMIC), which manufactures high-end gas carriers and has "recorded strong profitability".

Strategically, Yangzijiang's expansion includes its 51% stake in the JV Yangzi Mitsui (YAMIC), which manufactures high-end gas carriers and has "recorded strong profitability".

| Goldman’s Verdict: Upside Potential and Risks |

Goldman Sachs maintains a "Buy" rating for Yangzijiang, citing its attractive valuation.

The S$4.00 target price is derived using a P/B vs ROE valuation, applying a target P/B multiple of 2.2x to its end-2026 book value per share.

The broker asserts that "a higher P/B valuation compared to historical ranges is justified" given the company's strategic pivot from lower-return debt investments towards its core shipbuilding business, focusing on capacity expansion and enhanced shareholder returns.

Key catalysts for potential share price appreciation include "earnings beat & new orders share gain".

However, identified risks encompass higher-than-expected steel prices, more stringent regulations from USTR targeting Chinese-built vessels, larger-than-expected ASP decline, and faster-than-expected capacity expansion from other shipyards.

Despite underperforming its Chinese and Korean peers over the past 12 months, largely due to muted new orders year-to-date in 2025 and market jitters over US policy impacts, Goldman Sachs remains optimistic.

Market cap: S$12.2 billionThe report suggests that market share loss was a consequence of "tight capacity" rather than regulatory pressures. Market cap: S$12.2 billionThe report suggests that market share loss was a consequence of "tight capacity" rather than regulatory pressures. With anticipated capacity normalisation and the new Hongyuan shipyard becoming operational, Yangzijiang is "poised to regain market share from 2026E". Goldman Sachs' earnings estimates for 2026E and 2027E are notably "26-39% above consensus", indicating a strong belief in future performance.

The current share price is seen as "largely pricing in the cash flows from the current orderbook + net cash", implying that "any potential pick-up of new ship orders would bring incremental upside". This robust outlook, coupled with strategic positioning and attractive valuation, suggests a potential rebound in Yangzijiang Shipbuilding’s stock performance. |

See also: YANGZIJIANG: Its ship orders will recover. Why wouldn't they? But how soon?