• Two research houses have taken new interest in covering Geo Energy Resources which has a major project getting into full swing in Indonesia. • Reports by Phillip Securities and KGI both express confidence in the game-changing nature of the project -- a 92-km hauling road and a jetty to facilitate the transport of coal from not just Geo Energy's mine but also several third party mines.  Artist's impression of trucks delivering coal to the new jetty. Source: Company Artist's impression of trucks delivering coal to the new jetty. Source: Company• Phillip and KGI analysts have crunched the numbers and set price targets for Geo’s stock way above what it’s trading at now (32 cents). Phillip says 47 cents, while KGI shoots for 64 cents. Same method (Discounted Cash Flow), but different assumptions, so the targets vary. • Even for this year, Phillip and KGI aren't on the same page. On a ~40% increase in Geo's guidance for 2025 coal production, Phillip has Geo earning US$46.2 million while KGI, US$89.7 million (which looks overly optimistic unless coal prices jump). Earnings in 2024 amounted to US$37.1 million, in comparison. One thing’s clear—they’re both betting big on Geo’s future when the infrastructure project is completed mid-2026. • Read more below what Phillip says ... |

Excerpts from Phillip Securities report

Analyst: Paul Chew

Geo Energy Resources Ltd

Buying multi-bagger optionality

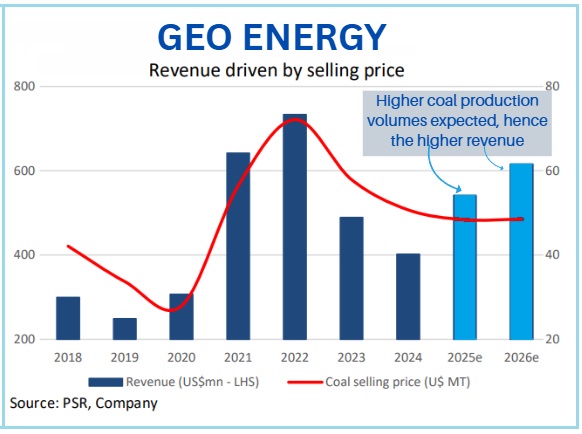

| ▪ The completion of a 92km road and jetty in South Sumatera Indonesia, will triple Geo’s thermal coal production to 25mn MT by FY29e. There will be additional capacity from this infrastructure to generate lucrative recurring toll revenue from other mining coal producers, potentially exceeding US$200mn per annum. ▪ Demand for thermal coal globally remains stable, driven by emerging countries China, India, and SE Asia. Indonesia remains the largest thermal coal exporter, with a market share of 47%. We are forecasting stable coal prices in FY25e/FY26e. Geo’s production is expected to increase 43% YoY in FY25e, recovering from the poor weather conditions and accelerated pre-stripping last year. ▪ We initiate Geo Energy with a BUY recommendation and a DCF target price of S$0.47. |

With the hauling road only 10% complete and 50% of the land cleared, we offer a 70% discount on the value of the increased coal production and toll revenue resulting from the new road.

|

GEO ENERGY |

|

|

Share price: |

Target: |

The completion of the hauling road and jetty will triple the current production volume plus generate lucrative road toll revenue for Geo.

The road and port infrastructure are being built for US$150mn and will be completed in 1H26.

Of the four existing mining concessions, two mines are expected to be closed by FY28/29e.

| Highlights |

• Production spike from new mines and infrastructure. In Aug24, Geo agreed with China Communications Construction Company to construct a hauling road and jetty (integrated Infrastructure) in South Sumatera.

The contract price is US$150mn.

Geo shall pay US$21mn first, with the remainder to be paid progressively over the next 2 years.

The infrastructure will increase MBJ road and jetty capacity to transport coal by 25mn MT in 1H26.

"The two largest markets for Geo are China and Indonesia with 62% and 32% of market share respectively in FY24. Despite its substantial market share, there is no significant volume or counterparty risk because its export sales of coal are made to international offtakers." -- Phillip Securities |

The next phase will boost the capacity to 50mn in 2028.

With the new infrastructure, production from TRA is expected to jump 20-fold from the current 1.2mn MT in 2024 to 25mn MT by 2029.

• Another more profitable revenue stream. With a road and jetty capacity of 50mn MT p.a., Geo can lease out the remaining 25mn MT not required by TRA to other coal companies.

In Mar24, Geo entered into term sheets with two mining companies to lease 25mn MT of the integrated infrastructure.

The current road hauling and jetty fee is US$7 per MT.

With the improvement in road conditions and delivery speed, a US$10 per MT leasing fee is warranted.

|

See also: GEO ENERGY: Big Money Flowing into Sumatran Coal -- and This Company's New Road to Riches