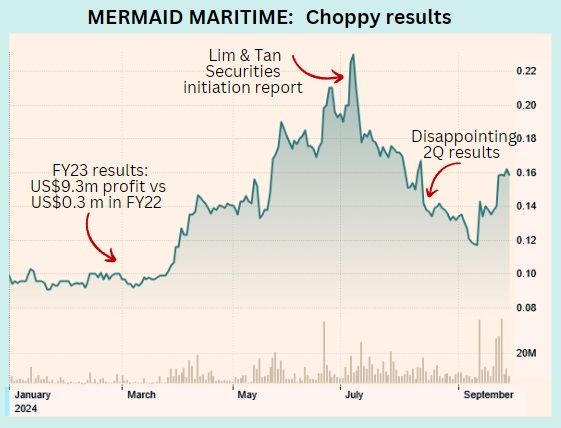

• Mermaid Maritime's stock had done well with a 100+% rise, from 9.9 cents to 23 cents, its peak following an initiation report by Lim & Tan Securities. • Then aggressive profit-taking set in, sending it down a whopping 50%. The gloom deepened when Mermaid released its 2QFY24 (ended June 2024) results, with profit coming in at only US$2.9 million (-12.7% y-o-y). •What was stark and dark was the fall in profitability despite a 155% jump in revenue. The decommissioning contracts which accounted for a big jump in revenue was barely making money. This has moderated investors' expectations of the record orderbook, which had been boosted by decommissioning projects.  • In decommissioning, Mermaid (market cap: S$234 million) engages in, among otherthings, the removal and disposal of platforms and pipelines, etc ensuring that the site is left in an environmentally acceptable condition. Offshore decommissioning is at an infancy stage across the world with Asia-Pacific forecasted to be the fastest-growing region. Don't expect Mermaid's decommissioning work to deliver great margins. CGS International, in its initiation report today, forecasts 8.2% gross margin only in FY2025 for the T&I and Decommissioning segment where the decommissioning work falls under. • Following Lim & Tan's initiation report with a bullish target price of 30 cents, CGI's report sets a target that is modest at 20 cents. Read excerpts below... |

Excerpts from CGS International report

Analysts: Meghana KANDE & LIM Siew Khee

Mermaid Maritime (MMT SP)

| ■ MMT’s orderbook (OB) of US$976m, as of 2Q24, is at an 11-year high due to new decommissioning orders and renewal of IRM contracts at higher values. ■ Limited newbuilds over the past decade have kept global vessel supply tight, driving MMT’s fleet utilisation to over 80% in 1H24, up from 50% in 2021. ■ We expect MMT to achieve net profit growth of 22%/70% in FY24F/25F from execution of larger-scale decom. projects and high-margin cable-lay orders. ■ The stock trades at a 33% discount to global peers’ 2025F P/E. We initiate on MMT with an Add call and TP of S$0.20, based on 11x 2025F P/E. |

Mermaid's subsea IRM (inspection, repair and maintenance business segment is a core contributor while decommissioning is a strongly emerging business.

Mermaid's subsea IRM (inspection, repair and maintenance business segment is a core contributor while decommissioning is a strongly emerging business.

Rebound in orderbook to 11-year high

Mermaid Maritime (MMT) is a subsea services provider for the offshore oil & gas (O&G) industry worldwide.

| Mermaid Maritime | |

| Share price: 16 c | Target: 20 c |

As per the company’s 2Q24 presentation, it owns a fleet of 7 vessels (including 3 saturation diving support vessels (DSVs)) and 14 ROVs with around 47 third-party vessels chartered for projects in Southeast Asia, Middle East (ME), West Africa and North Sea.

Over 2020-1H24, MMT grew its OB four-fold to US$976m, primarily on new larger-scale decommissioning contracts in Thailand and North Sea.

It also renewed key subsea inspection, repair and maintenance (IRM) contracts in the ME at higher values.

"We forecast MMT's net profit to grow by 22% yoy in FY24F and 70% yoy in FY25F. Despite scheduled dry-docking of two subsea vessels in 2025F, the company's high-margin cable-laying projects and the operational efficiencies gained from deploying new vessels like the Hilong 106 and Huan Qiu 1200 for decommissioning work should cushion the impact, in our view." -- CGS International |

Tight global vessel supply is driving higher subsea fleet utilisation

The global subsea vessel market is experiencing a supply crunch due to rising demand from O&G exploration and minimal newbuild orders.

Clarksons data show that only 3 DSVs have been delivered since 2023, with 1 more on order.

MMT has one of the largest DSV fleets (3 owned + 1 chartered) in the world, and improved utilisation of its IRM vessels to 80% in 1H24 from 50% in 2021.

High global rig utilisation, which is expected to stay above 90% till 2028F, according to Westwood’s Riglogix, puts MMT in a good position to capitalise on the sustained demand for subsea services, in our view.

Ageing oil & gas fields to catalyse large-scale decom. spend

With nearly 2,600 platforms in APAC and more than 1,300 wells in the UK Continental Shelf set to retire over the next decade (according to Wood Mackenzie and North Sea Transition Authority), we see multi-year industry tailwinds for MMT.

Mermaid has been ramping up its Transportation & Installation (including decom.) segment since 2021 and added 3 large vessels on charter in YTD 2024.

The segment’s share of revenues rose to 60% in 2Q24 from 6% in 2021 on execution of large-scale orders won in 2023.

We expect operational efficiencies in decom. projects and high-margin cable-lay order wins to cushion the net profit impact from two subsea IRM vessels going into dry-dock in 2025F

| Initiate with a TP of S$0.20 We initiate coverage on MMT with an Add call for its strategic position of benefiting from the global subsea vessel supply crunch.  Meghana Kande, analystOur TP is based on 11x 2025F P/E, a c.15% discount to global peers given MMT’s smaller scale. Meghana Kande, analystOur TP is based on 11x 2025F P/E, a c.15% discount to global peers given MMT’s smaller scale. Key catalysts: order wins, higher-than-expected day rates and fleet utilisation, fleet expansion and M&A announcements. Downside risks include escalation of geopolitical tension in the Middle East, poor weather and prolonged dry-dock impacting vessel utilisation, and order cancellations. |

Full report here.