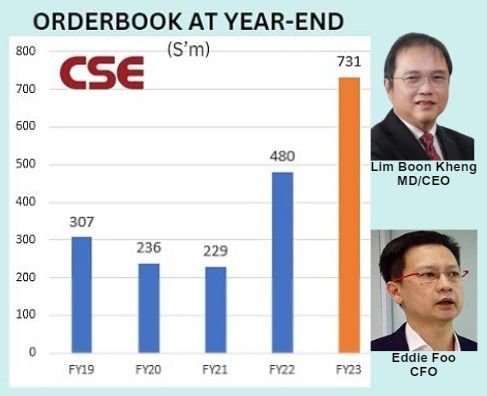

• Big shareholders sometimes have their own reasons for exiting a stock -- even when the outlook is decent, if not great. Turns out that there has been a big seller of CSE Global shares, which explains why the stock has been rangebound for quite a while. The stock at 46 cents yesterday was virtually unchanged from 12 months ago (but there was a rights issue in March 2024). • In a report today, Maybank Kim Eng says the seller has now "likely" divested its holding of Singapore-listed CSE (market cap: S$280 million) -- and thus lifted the overhang. • CSE is a "rare proxy" play -- not direct play -- on AI, data centers, and has a record orderbook. See the orderbook chart below of this systems integrator providing electrification, communications and automation solutions across various industries globally.  Electrification segment accounted for S$434 million of the FY23 orderbook. The other segments: Automation (S$192 million), Communication (S$105 million). Electrification segment accounted for S$434 million of the FY23 orderbook. The other segments: Automation (S$192 million), Communication (S$105 million).• "Electrification" -- CSE provides solutions related to power distribution and electrical control systems. This segment has been a significant driver of the company's revenue growth, particularly due to rising demand in the data centre, power, utility, and energy storage markets. • CSE counts Temasek Holdings as its No.1 shareholder and the Singapore Government as one of its clients. Read excerpts of Maybank's report below .... |

Excerpts from Maybank KE report

Analyst: Jarick Seet

Overhang cleared and positive 1H24E looming

We also believe that a substantial shareholder, who had been paring down their stake since 2023 has likely pared all their stake. This would be positive for CSE as the overhang suppressing the share price is likely gone. With better operating leverage due to strong revenue growth, CSE is on track to deliver better quarters ahead and remains one of our conviction picks as a rare proxy for electrification/AI/data centres. Maintain BUY. |

| Order win momentum likely to continue |

We expect order wins for 2Q24E to remain strong with double-digit growth YoY due to its strong pipeline of infrastructure projects from the US.

|

CSE |

|

|

Share price: |

Target: |

This will likely boost its already robust order-book, which is also a good indicator of its potential revenue going forward.

| A key beneficiary of AI boom and data centres |

CSE’s recent SGD49.2m plant extension is for the design, engineering, fabrication, installation and integration of power management systems and solutions for data centres in the US.

CSE’s recent SGD49.2m plant extension is for the design, engineering, fabrication, installation and integration of power management systems and solutions for data centres in the US.

We think its client is one of a handful of main cloud providers in the US and believe it will likely win more data centre contracts from existing and new customers.

AI technology and data centres require huge amounts of energy to develop and run and will benefit power management system integrators like CSE.

| Potential buybacks and accretive acquisitions |

CSE offers a unique opportunity to ride the upcycle in attractive growth areas.  Jarick Seet, analystIt also offers a sustainable 6.5% dividend yield.

Jarick Seet, analystIt also offers a sustainable 6.5% dividend yield.

We believe CSE has a clear multi-year growth outlook and we expect further accretive acquisitions, especially in the critical communications segment in the US and Australia, which could accelerate its growth.

There is also a strong possibility of management share buy-backs and company share buy-backs.

Full report here.