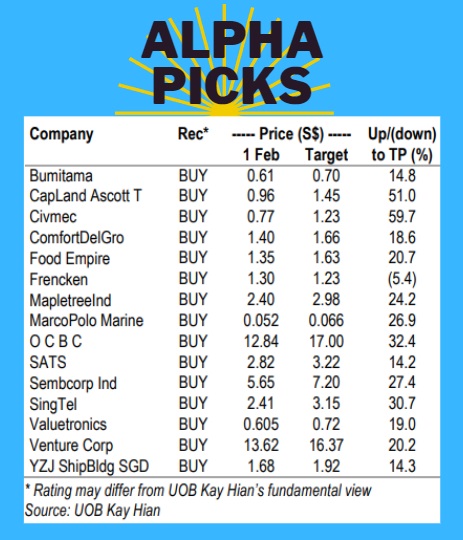

| • UOB Kay Hian puts out the monthly performance of its "alpha picks" portfolio. It has done decently, outperforming the FSSTI in 11 out of the past 12 months. • In today's report, UOB KH adds Yangzijiang Shipbuilding (finally!) to its portfolio while removing Seatrium (finally!). While it's a big-cap with a broad suite of capabilities, Seatrium lacks attractive valuations. (See: Would you buy a big-cap S'pore stock on forecast 54X PE?) • A star performer, on the other hand, is Food Empire (+19.5% month-on-month).  Vietnam is a key market for Food Empire's instant coffee. Vietnam is a key market for Food Empire's instant coffee. UOB KH says a catalyst is its proposed dual listing in HK. Well, some investors are skeptical given how Singapore companies have done aftter their HK dual listings. Probably better reasons are Food Empire's current valuation of 10X 2023F PE and 9X2024F. Still attractive even after the run-up? UOB KH's target price is $1.63. |

Excerpts from UOB KH report:

| For Feb 24, we add Yangzijiang Shipbuilding (YZJ) as we see dividend upside and potential earnings upgrades from its upcoming results and remove Seatrium (STM) as uncertainty over the size of its 2023 write-offs may weigh in the short term. |

• Reviewing our picks in January. Our portfolio performance was mainly dragged by STM (-15.3% mom) and Frencken (-3.7% mom).

A S$250m contract cancellation and profit warning by STM led to its share price retreat, while Frencken followed the weakness in US technology stocks as profit-taking took place after Big Tech’s earnings release.

This was largely offset by Food Empire (FEH, +19.5% mom), which rallied in response to the company’s proposed dual listing on the HKEX, and SembCorp Industries (SCI, +6.8% mom) with its continued news on acquisitions underlining its medium- and long-term growth potential.

ACTION

• Adding YZJ and removing STM. For Feb 24, we include YZJ in our portfolio with its 2023 results on 28 Feb 24 likely to see higher order win guidance, higher dividends and better shipbuilding margins.

We remove Seatrium due to uncertainty over the size of its 2023 write-offs potentially weighing on its share price in the short term.

• Strong 2023 results expected on 28 Feb 24. YZJ will report its 2023 results on 28 Feb 24 with the key items to look forward to being new guidance for higher order wins, better shipbuilding margins and freight rates (especially given the terrorist disruptions in the Red Sea) and higher yoy dividend. • Started off the year with a big order. On 17 Jan 24, YZJ reported a new order for six 13,000TEU containerships which are methanol dual-fuelled vessels.  Adrian Loh, analyst No order size was given; however, using order compass from Asian yards, each vessel is likely to cost US$130-150m, implying a US$700-900m order win. Adrian Loh, analyst No order size was given; however, using order compass from Asian yards, each vessel is likely to cost US$130-150m, implying a US$700-900m order win. Importantly, these six containerships will be delivered from 2027 onwards which underlines the company’s revenue visibility for 2027 and into 2028. • We have a BUY recommendation on the stock with a PE-based target price of S$1.92. Our target PE multiple of 10.1x, applied to an aggregate of our 2023 and 2024 EPS forecast, is 1.5SD above YZJ’s past five-year average of 6.8x. We view this as fair given: a) the company’s earnings growth in 2023 and 2024, b) sustainability of its earnings due to its US$15b orderbook at present, and c) earnings visibility into 2027 and 2028. Share Price Catalysts • Events: a) Better capital management initiatives, b) new order win announcements, and c) safe and efficient execution of orderbook. • Timeline: 3-6 months. |

Full report here.