|

Has there ever been a Singapore-listed company whose earnings leapt 100X in a reporting period?

Its stock price has, accordingly, swung up some 3,350% year-to-date (ie from 4 cents to $1.38), taking its market cap from S$22 million to S$758 million. That magnitude of upswing is likely to be unprecedented on SGX. All this has to do with Medtecs’ business boom during this Covid-19 pandemic as it supplies a wide range of personal protective equipment to Asia, Europe and the US. |

Medtecs produces a wide range of personal protective equipment.

Medtecs produces a wide range of personal protective equipment.

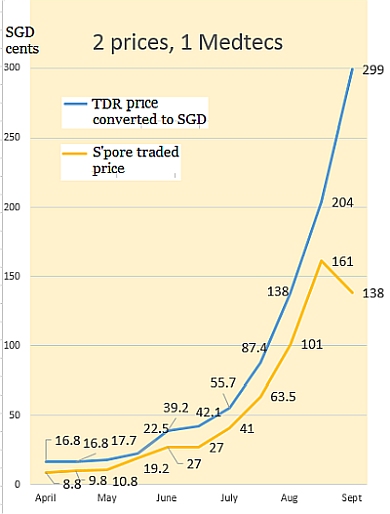

But a major disconnect has emerged between the trading price of Medtecs shares listed on SGX and Medtecs’ Taiwan Depository Receipts (TDR) listed in Taiwan.

One TDR stands for one Medtecs share.

You would expect them to trade at approximately the same value.

Nah, it hasn’t been happening, and it has diverged even more now, as the chart shows.  2 data points per month: Prices taken at start and middle of months, except Sept which has a single price point (4 Sept).Why? Is it because Taiwanese buyers have more feeling and conviction for Medtecs?

2 data points per month: Prices taken at start and middle of months, except Sept which has a single price point (4 Sept).Why? Is it because Taiwanese buyers have more feeling and conviction for Medtecs?

After all, Medtecs is a Taiwanese company with its HQ in Taiwan, while it operates not just in Taiwan but also the Philippines, Cambodia and China.

Perhaps also, Taiwanese investors have their fingers closer to the pulse of this industry as there are several similar businesses listed in Taiwan.

Additionally, listed companies give basic monthly updates that help investors form a view of their business performance.

And the PPE industry has been clearly headed up.

Still, can one argue that Taiwanese investors are over-enthusiastic and over-paying?

For an answer, we turn to Medtecs' guidance on 11 Aug 2020 in its 1H20 results statement:

| "Looking ahead to the second half of the year, due to long-term supply contracts and a steady stream of new orders, barring unforeseen circumstances, the Group's revenue and profit is expected to exceed that of the first half of the year." |

Based on the guidance, there can be many ways to project what 2H profit would be. Two possible scenarios are:

Scenario #1: As a base case, we conservatively assume 2H is equal to (instead of exceeding) 1H profit. Then we have

In SGD terms, it is S$108 million (ie, FY20 PE of 7 based on the last traded share price of S$1.38). Scenario #2: We assume 3Q and 4Q profits are the same as 2Q (US$35 million). Then we have:

In SGD terms, it is S$150 million (ie, FY20 PE of 5.0 based on a share price of S$1.38). |

In Scenario #1, the valuation can be said to closer to being cheap than to being expensive.

Is Scenario #2 reasonable or over-optimistic? Or, to some people, is it actually conservative?

Looking to the glove industry, we know that average selling prices of gloves has been rising from month to month since 2Q.

The same supply-demand forces are at work in the PPE industry.

Thus you can make the case for assuming 3Q and 4Q profitability of Medtecs to be more or less on par with its 2Q profit.

However, that remains an assumption because:

| • There is much less clarity about ASP trends in the PPE industry compared to the glove industry, where numerous analyst reports have tracked changes in ASPs. • There is a wide range of products that Medtecs produces, with some items like shoe covers earning pennies. Furthermore, Medtecs has two other smaller business segments (hospital services and trading/distribution). |

With glove stocks trading in the 20-30 PE range, can Medtecs be valued in the same range?

Normally, the professionals -- ie analysts -- do the job of informing and enlightening the investing public, usually with some guidance on financial performance metrics from the management of the listco.

Well, no report on Medtecs has come out as yet, and likely Medtecs' management has been too busy to chip in.

If that's the case, its stock price is not going to reflect the business value adequately but instead rise and fall with trading sentiment and news headlines and pernicious elements such as shortists and manipulators.

What would help, in the short-term, is a business update from management next month (October) or November along with some basic financial performance figures for 3Q.

Such an update will surely trigger a re-calibration of the market valuation of Medtecs, just as the Aug update did.

|

Remember, much of the above discussion was premised on the Medtecs guidance of 11 Aug 2020.

It's a bland guidance. Turns out that 2Q delivered US$35 million, far exceeding the US$3.7 million of 1Q. |

Beyond profits, the jump in cashflow that Medtecs enjoys points to interesting opportunities.

In 1H20, the operating cashflow surged to US$25.6 million while it spent about US$4 million on capex.

Dividends are pretty much a given (a small 0.85 US cent/share interim dividend has already been declared) but the company will have to demonstrate wisdom in deploying its new cash firepower.

This is where it can build a more solid base for a future where PPE demand will be dialed back as and when Covid-19 is tamed.

This demand change likely will be gradual because governments will rebuild their PPE inventory. And in the back of everyone's minds is a fear that Disease X may emerge.