China Sunsine Chemical Holdings is a leading specialty chemical producer of rubber accelerators, insoluble sulphur, antioxidants and other vulcanising agents. It is the world’s largest producer of rubber accelerators (essential in tyre production) and China’s biggest producer of insoluble sulphur. It serves over 1000 customers globally and more than two-thirds of the Global Top 75 tyre makers such as Bridgestone and Michelin, as well as China tyre giants such as Hangzhou Zhongce and GITI Tire. Link to StockFacts company page Link to kopi-C interview with CEO Liu Jing Fu |

||||||||||||||||||||

1. What are some notable developments and key focus areas in 2020 and after?

China Sunsine is the world’s largest producer of rubber accelerators. NextInsight file photo.• Since 1998, we have been focused on organic expansion which will continue. We have since strengthened our financial position and market leadership in the rubber chemicals industry. We are the world’s largest producer of rubber accelerators and China’s biggest insoluble sulphur producer, serving 2/3 of top global tyre makers.

China Sunsine is the world’s largest producer of rubber accelerators. NextInsight file photo.• Since 1998, we have been focused on organic expansion which will continue. We have since strengthened our financial position and market leadership in the rubber chemicals industry. We are the world’s largest producer of rubber accelerators and China’s biggest insoluble sulphur producer, serving 2/3 of top global tyre makers.

• We will leverage on the current market downturn to expand our capacity in order to benefit from the recovery when it occurs. Our expansion projects in 2020 are:

| 1) 20,000-tonne p.a. high-end fully automated Rubber Accelerator TBBS to be completed in 1H2020, with commercial production in 2H2020 2) 30,000-tonne p.a. Insoluble Sulphur project located in New Chemical Zone to be completed by end-2020 3) 30,000-tonne p.a. Antioxidant TMQ project located in Shanxian to be completed by end-2020 |

• We believe that these projects will help increase our market share, and bolster our financial position in 2021.

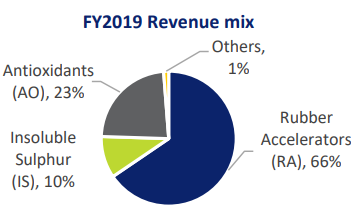

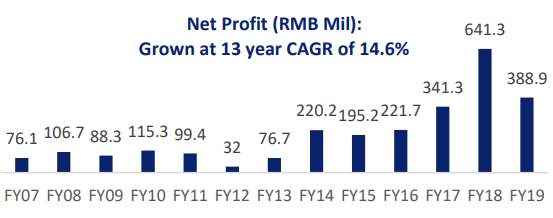

2. Describe the Group’s revenue mix and profitability track. Do you plan to maintain or grow this? • Our product mix includes three main categories (below) and we plan to continue with the current mix. Our net profit has grown at a CAGR of 14.6% since our listing 13 years ago in 2007.

• Our product mix includes three main categories (below) and we plan to continue with the current mix. Our net profit has grown at a CAGR of 14.6% since our listing 13 years ago in 2007.

| 3. China Sunsine has been battling weak average selling prices (ASP) and persistent pricing pressure in the recent months. What is the impact on the Group’s performance and how does it intend to manage this going forward? • Various factors, such as slowing economic growth, declining auto sales, intensifying market competition and low raw material prices have put pressures on ASPs. Despite this, we believe that we have several advantages over our competitors in terms of – economies of scale, superior product quality, a loyal customer base, and strong financials and balance sheet. • To reduce impact on gross margins, we have adopted a strategy of “Production and Sales Equilibrium”, which means “higher production leads to higher sales volumes, which in turn stimulates even higher production.” It aims to expand our market share and pursue long-term sustainable growth by organically increasing our capacities. |

4. The biggest challenge facing China, and the world, now is the current COVID-19 outbreak. How has the pandemic affected demand and sales in the industry?

• Rubber accelerators are essential additives in the making of tyres. Hence our business is closely interlinked with the global tyre and automobile industries.

|

Covid-19 impact |

|

“Due to COVID-19, many China tyre and rubber chemical manufacturers (including us) delayed resumption of work after the Lunar New Year holidays. Some have gradually started production. But with the global spread of COVID-19, many foreign tyre companies have suspended production. Although the Group's capacity utilisation rate remains high, we expect this wave of suspensions to affect our subsequent production plans.” |

• China’s new car sales have declined 42% YoY in the first quarter of 2020 (Source: China Association of Automobile Manufacturers). According to analysts' forecasts, full-year auto sales will shrink 13%-15% this year, before increasing for the first time in three years by 2021.

Compared to new car sales, the tyre industry may continue to see more stable sales, given only <30% of tyres are used in new cars, while the remaining 70% are used in replacement tyres.

• Over the long term, as a consumer good, tyres are expected to see steady growth, and demand will move in tandem with tyre consumption trends.

5. What measures has the Group put in place to ride out the COVID-19 pandemic?

• We are of the view that the pandemic will end eventually and the economy will recover and grow. We currently focus on two aspects.

• First, increasing domestic sales as we expect domestic demand to pick up as many industries have resumed productions. Second, reducing internal consumptions and putting in place cost-saving measures as we focus on innovation, productivity and automation in our production processes.

6. US and China have signed Phase One of their trade agreement. Do tariffs under this deal have any impact on China Sunsine’s sales?

• Generally speaking, the impact is expected to be minimal and manageable, as the US accounts for only 2% to 4% of our sales. Furthermore, in 2014, when the US raised tariffs on China’s tyres and related products, many tyre manufacturers had already set up production plants outside China to side-step the restrictions.

7. What are the factors critical to China Sunsine’s success in this competitive landscape?  Executive chairman Xu Chengqiu• We view exemplary leadership, effective strategy and the emphasis on environmental protection as our success factors. Under our Executive Chairman, Mr Xu Chengqiu, the Group has achieved healthy, steady growth over the past 20 years, and established a leading position in the rubber chemicals industry.

Executive chairman Xu Chengqiu• We view exemplary leadership, effective strategy and the emphasis on environmental protection as our success factors. Under our Executive Chairman, Mr Xu Chengqiu, the Group has achieved healthy, steady growth over the past 20 years, and established a leading position in the rubber chemicals industry.

• Next, developing an effective strategy was critical, namely, positioning the Group in the early years as a quality provider serving major tyre makers.

• Lastly, the emphasis on environmental protection has helped us stay ahead of competition. The Chinese government’s stringent environmental protection regulations forced many players that did not meet requirements to shut down. We leveraged on this opportunity to cement our position in the industry.

• Our products are well-recognised and sales had been healthy (as our utilisation rates over past few years remained close to 100% despite challenges in the industry). We have decided to continue raising capacity, so as to increase market share and strengthen our leadership position.

8. Does China Sunsine have a fixed dividend policy? The Group has a share buyback programme and has been buying shares from the market. Do you plan to continue to do so?

• Although the Company doesn’t have a fixed dividend rate, it has been paying dividends annually since its IPO in 2007. The Board reviews and discusses the dividend payout every year, taking into account factors such as cashflows, earnings, capex, future developments and overall business environment.

• In Nov 2019, we also undertook a share split of every one existing ordinary share into two shares to increase share liquidity and broaden our shareholder base.

• Our share buyback mandate remains valid and will be renewed in our upcoming AGM. As our current share price is trading at 0.7x price to book ratio, we will continue the share buyback programme at an appropriate time.

9. What do you think investors may have overlooked about China Sunsine’s business?

• Investors may not have understood our business model and the rubber chemicals industry. However, we believe that China Sunsine is a value company with sound fundamentals and prospective capacity expansion.

• The Group’s financial position and cashflows have strengthened over the years, and we believe that it is at its best ever – as at end 2019, cash balances stood at RMB1.28 billion with zero debt. Net asset value (NAV) per share was RMB 262.6 cents (S$0.51), with cash per share at RMB 131.6 cents (S$0.26), while earnings per share (EPS) was RMB 39.72 cents (S$0.078 cents).

10. What is China Sunsine’s value proposition to shareholders and potential investors?

• We believe that our value proposition is reflected in our track record, market leadership, and strong cash position. We have been profitable every year over the last two decades. The CAGRs for revenue and net profit between 2007 and 2019 were 13.0% and 14.6% respectively, with ROE levels of 15%-25% annually.

• We remain the world’s No. 1 producer of rubber accelerators, capturing market share of 20% globally and 33% in China. Leveraging on our strengths in quality, economies of scale, product range, cost, environmental and market leadership, China Sunsine continues to serve more than 1,000 customers that include the world’s global top tyre makers.

• China Sunsine maintains a high capacity utilisation rate over the last few years from robust demand. We believe that we are poised for long-term sustainable growth by way of organic expansion, with the extension of the 3 expansion projects this year, while planning for the future expansion over the next couple of years, as shown by the strategic acquisition of the 680-mu land in Shanxian last year.

Originally published on SGX website.

10 in 10 – 10 Questions in 10 Minutes with SGX-listed companies

Designed to be a short read, 10 in 10 provides insights into SGX-listed companies through a series of 10 Q&As with management. Through these Q&As, management will discuss current business objectives, key revenue drivers as well as the industry landscape. Expect to find wide-ranging topics that go beyond usual company financials. This report contains factual commentary from the company’s management and is based on publicly announced information from the company. For more, visit sgx.com/research.

For company information, visit https://www.chinasunsine.com

Click here for full year FY2019 Earnings Announcements