Excerpts from today's analysts' reports

Lim & Tan Securities says now is a buying opportunity for Hi-P International

BlackBerry Z10. Photo: BlackBerryHi-P’s major customer Blackberry has been strengthening in the past 4 trading days by close to 10% after RBC Capital Market and Society Generale analysts raised expectations for shipments of new Blackberry 10 devices (Z10 and Q10 ) from 2.7mln units to 3.5mln units after channel checks revealed better than expected sales numbers.

BlackBerry Z10. Photo: BlackBerryHi-P’s major customer Blackberry has been strengthening in the past 4 trading days by close to 10% after RBC Capital Market and Society Generale analysts raised expectations for shipments of new Blackberry 10 devices (Z10 and Q10 ) from 2.7mln units to 3.5mln units after channel checks revealed better than expected sales numbers.

Lim & Tan Securities says now is a buying opportunity for Hi-P International

BlackBerry Z10. Photo: BlackBerryHi-P’s major customer Blackberry has been strengthening in the past 4 trading days by close to 10% after RBC Capital Market and Society Generale analysts raised expectations for shipments of new Blackberry 10 devices (Z10 and Q10 ) from 2.7mln units to 3.5mln units after channel checks revealed better than expected sales numbers. Hi-P’s share price has pulled back by 11% since peaking in May ’13, in line with the market’s decline.

Besides declining in sympathy with the market, we believe the cessation of its share buy back program also caused some market concerns.

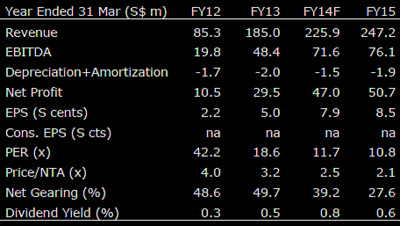

We see the recent pull-back as another opportunity to buy the stock as we believe that the better than expected recovery of Blackberry and Apple coupled with new contributions from Nike and Amazon would see a strong rebound in the company’s profit this year by 177% to $50mln, putting its forward PE at an undemanding 12x against historical average of 15x.

Maintain BUY.

Recent story: HI-P INTERNATIONAL: Upgrades by CIMB & OSK on 1Q2013 net profit jump

Recent story: HI-P INTERNATIONAL: Upgrades by CIMB & OSK on 1Q2013 net profit jump

OCBC Investment Research maintains buy call on United Envirotech

Analysts: Carey Wong & Andy Wong

United Envirotech Ltd (UEL) has recently announced the establishment of a US$300m MTN (medium-term note) programme, where it may from time to time issue medium-term notes.

United Envirotech Ltd (UEL) has recently announced the establishment of a US$300m MTN (medium-term note) programme, where it may from time to time issue medium-term notes.

Analysts: Carey Wong & Andy Wong

United Envirotech Ltd (UEL) has recently announced the establishment of a US$300m MTN (medium-term note) programme, where it may from time to time issue medium-term notes.Getting ready for more investments: According to management, the main rationale for the MTN programme is to get ready its funding to cater for the still-buoyant waste-water treatment industry in China.

This as it continues to see growing demand for membrane-based water and waste-water treatment services, driven by stricter discharge limits imposed by the Chinese government and the shortage of water supply in various parts of the mainland.

This as it continues to see growing demand for membrane-based water and waste-water treatment services, driven by stricter discharge limits imposed by the Chinese government and the shortage of water supply in various parts of the mainland.

Project wins will act as catalyst: Since we had recently revised our estimates after its FY13 results, we opt not to change anything for now.

Hence our fair value remains unchanged at S$1.03 (still based on 13x FY14F EPS). But we do see potential catalyst coming from project wins. Maintain BUY.

Recent story: UNITED ENVIROTECH has record FY13, CHASEN bags 7 projects

Hence our fair value remains unchanged at S$1.03 (still based on 13x FY14F EPS). But we do see potential catalyst coming from project wins. Maintain BUY.

Recent story: UNITED ENVIROTECH has record FY13, CHASEN bags 7 projects