BNP Paribas: CHOW SANG SANG Started ‘Buy’

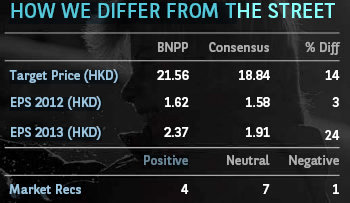

BNP Paribas has initiated coverage of Chow Sang Sang Jewelry (HK: 116) -- a fast-growing retailer of colored stones and jewelry across Greater China -- with a “Buy” recommendation and a 21.56 hkd target price.

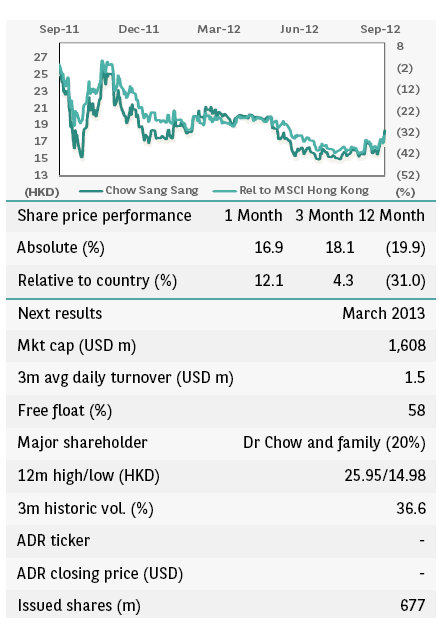

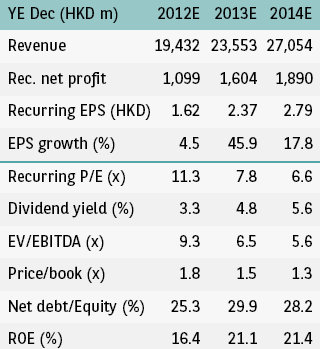

“The company saw net profit decline 11% y-o-y in the 1H12 (ended December), but we expect it to see 5% earnings growth in FY12, with a boost to gold prices from QE3 alleviating gold margin pressure.

“The company has outperformed peers so far in 2012 thanks to solid SSSG year-to-date,” BNPP said.

The research house said Chow Sang Sang’s high diamond exposure is likely to benefit from the sector product mix shift.

“It has historically lagged peers due to a self-operated expansion model, but we believe its store network is reaching economies of scale.

"As non-jewelry segments slow in growth, distortions to margins and growth should unwind and uncover underlying value.”

BNPP added that Chow Sang Sang is “attractively valued” at 7.8x FY13E P/E and 0.4 PEG.

“We value Chow Sang Sang using a blended average of EV/EBITDA and DCF.

“Our target 7.0x forward EV/EBITDA is a 25% discount to the historical average and within the range for high global mid-cap peers. “

The Hong Kong-listed jewelry retailer also benefited from an “established brand name with an improving outlook.”

Chow Sang Sang has one of the longest brand histories among Hong Kong jewelry companies with a strong brand and sizable market shares (top 3 in Hong Kong, top 15 in Mainland China).

“It is upstream-integrated, which reflects in its product quality and high proportion of diamond sales (29% of jewelry revenue in FY11) as well as gem-set sales (34% of jewelry revenue in FY11, including diamonds),” BNPP said.

Chow Sang Sang has previously lagged peers in growth due to a combination of its 100% self-operated store expansion and conservative management style, but increasing economies of scale and steady store expansion (50 PRC stores/22% of total at end-FY11) provide an attractive growth outlook for the company.

BNP added that the growing PRC market favors Hong Kong jewelry retailers.

“We are positive on Hong Kong jewelry retailers, given the strong growth outlook for the jewelry market in China and favorable landscape.

“We expect significant growth in the PRC jewelry market owing to increasing penetration, and believe Hong Kong jewelry brands’ exceptional profitability and brand equity will allow them to gain market share.”

See also:

CHOW SANG SANG, LENOVO Both ‘Outperform’

HK & PRC Retail Rundowns; CHOW SANG SANG Looking Golden

CHOW SANG SANG Sales Surge; Move Over, India?

CHOW SANG SANG Kept At ‘Buy’, HK Property Initiated ‘Outperform’

Bocom: PROPERTY Kept ‘Outperform’

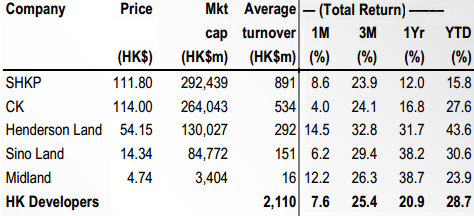

Bocom International said it is maintaining its “Outperform” call on Hong Kong-listed real estate developers.

“The solid results of SHKP (HK 16) suggested a sustainable high earnings base, well supported by rental income growth. We reiterate a ‘Buy’ rating on SHKP with a target price of 147.0 hkd, a 20% discount to NAV,” Bocom said.

The brokerage is also downgrading Midland Holdings (HK: 1200) from ‘Buy’ to ‘Neutral’, in light of potential shrinkage in transaction volume.

Mortgage tightening to slow investment demand

The Hong Kong Monetary Authority’s (HKMA) new mortgage tightening will further differentiate end-user demand from investment demand.

“As we mentioned earlier, this is a reasonable move to prevent the formation of asset bubble caused by over-leveraging without affecting the demand from first-time buyers, and is also in line with CY Leung’s thinking since his election campaign.

“In addition, the new measures reduce not only the leverage from capital inflow, but also the potential risk in case of a capital outflow,” Bocom said.

This time, HKMA differentiates the applicants by “outstanding mortgage,” rather than “owner-occupied,” which relies on the applicants’ declaration.

“This is achievable with HKMA’s new mortgage database, and has a clearer definition. Compared with increasing land supply, mortgage tightening is more effective and has an immediate impact of slowing the market,” Bocom said.

However, the brokerage said it believes the monetary environment still favors property prices in the medium term, as the positive carry remains.

“We expect the new measures will only slow down the market, but not cool it off.”

See also:

CONTAINERS & CONDOS: Latest Happenings...

PROPERTIES, PREMIUMS, PIERS: Three China Sectors Scrutinized

WEIYE: Henan's Leading Property Player Rides Hainan Boom

PROSPERITY REIT: Seeking Right Stuff In Hong Kong