David Yee is a shareholder of Saizen REIT

THE RECENT GREAT response to Global Logistics Trust and Mapletree Logistic Trust IPO prompted me to do a simple analysis on Singapore REITs to identify REITs that could still be undervalued.

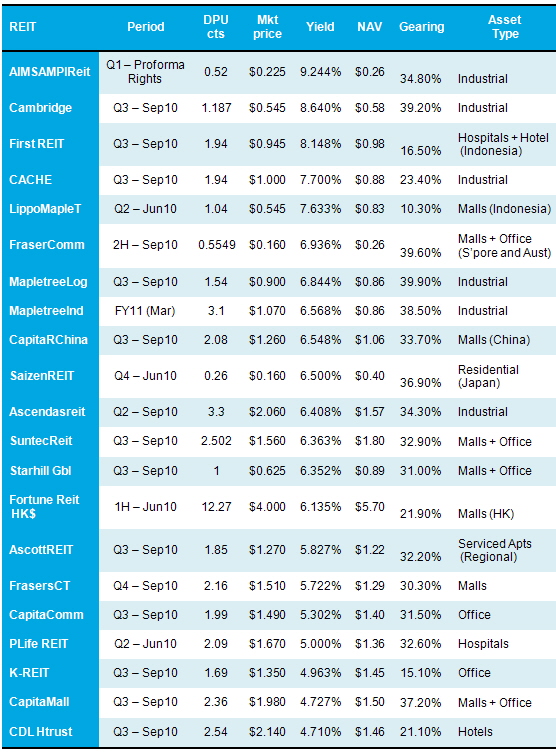

The SREIT average yield is 6.52% with the market leaders in term of asset size like A-REIT trading at a rich 30% premium to book value.

REITs that are currently trading below book value are AIMSAMPIReit, Cambridge, LippoMapletree, Suntec, Saizen, FraserComm, Fortune and Starhill Global (see table below).

The REIT that caught my attention is SAIZEN Trust.

Saizen is currently trading at steep discount to book value with a P/B ratio of only 0.40.

In simple terms, we are using $0.16 cash to purchase $0.40 in value of housing properties in Japan which are giving a yield of 9.75%. It looks very attractive compared to the near 0% fixed deposit offered by banks in Singapore.

The following are interesting facts extracted from its AGM presentation on 19 Oct:

Assets and Loan

Saizen REIT can be viewed in two parts:

- * “Healthy” part accounts for about 79% of Group assets and 91% of Group

* NAV Defaulted part accounts for about 21% of Group assets and 9% of Group

* NAV Cash flow from “Healthy” part is freely distributable to investors. - * If the YK Shintoku loan issue is resolved, this represents a “bonus” to investors.

Healthy part 91% of Group NAV = $0.364 per share still a great discount to market price $0.16

Resumption of Distribution

- FY2010 distribution of 0.26 cents per Unit, in respect of 2 months’ cashflow

- Distribution represents operational cash generated from 8 “healthy” subsidiaries (ie. excluding cash flow of YK Shintoku)

- • Distribution of cash generated from “healthy” part of the REIT is expected to continue

Annualised dividend is 1.56 cents a share, giving a 9.75% yield based on $0.16 price of Saizen units on the open market.

YK Shintoku loan

- Maturity default in November 2009

- Commenced discussions with financial institutions on potential refinancing of loan; any refinancing has to be on reasonable terms.

- Unencumbered properties of JPY 12 billion available as collateral for new loans.

- No indication of foreclosure actions to-date

- Asset manager continues to work closely with the loan servicer (including divestments)

Total Net Outstanding Loan JPY 5.3 Billion vs Unencumbered properties of JPY 12 billion.

Property operations and portfolio value

- * Property operations has been stable and is expected to remain stable

- * Average occupancy rate of 91.7% in FY2010

- * Tenant turnover improved from 22% in FY2009 to 20% in FY2010

- Overall rental reversions of contracts entered into during FY2010 were at rental rates which were marginally lower (by 4.3%) than previous rates

- Portfolio value remained stable compared with June 2009

Both Value and Rental Income are expected to remain STABLE

Divestments

- Partial and progressive divestment of YK Shintoku properties to facilitate refinancing of YK Shintoku’s loan.

- Divested 5 properties in FY2010 and a further 9 properties in FY2011to-date

- Total sale price JPY 1,953.5 million

- Sale prices were at a weighted average discount of 4% to valuation

- Assets proven to be liquid even at depth of crisis.

Divested properties were at a weighted average discount of 4% to valuation.

Assuming all properties (NTA) are to be sold in the market today, we will be getting back $0.384 cash per unit (ie $0.40 x 96%) vs $0.16 market price.

(Adjusted for Warrants = $0.32 x 96% = $0.30)

Recent story: INSIDER BUYING: HI-P, SAIZEN, BEST WORLD, TIANJIN ZHONG, etc

Article by David Yee: TECKWAH: A deep-value stock?