Excerpts from analysts' reports

OSK-DMG's target is S$1.50 for HanKore following Everbright deal

Analyst: Sarah Wong

HanKore will buy China Everbright’s (CEI) pool of 25 WWT and reusable projects of 1.892m tonnes/day design capacity for CNY5.8bn, or SGD1.2bn.

The successful merger removes deal overhang and gives the combined entity gearing headroom to pursue growth via M&As. We ascribe HanKore a 36x FY16F P/E (excluding earnings growth forecast from M&As), a premium to the 30x peer average, given its low 9% gearing. Maintain BUY, with changed SGD1.50 TP.

Purchase price higher than expected but within range of recent M&A transactions. The consideration of CNY5.8bn is higher than the initial expected figure of HKD4.0bn (or CNY3.3bn), but the price of CNY3,071/tonne of design capacity falls within typical M&A transactions prices of CNY2,500-3,000/tonne. As the merger will give HanKore distinctive state-backing advantages, we find the transaction price fairly decent.

The CNY5.8bn will be funded through the issuance of 1.94bn HanKore shares at SGD0.703 each (with adj. factor 0.889). CEI will own 78.0% of HanKore post share issuance, making the latter its subsidiary. The transaction represents a 1.56x NAV of CNY3.7bn.

OSK-DMG: "We value HanKore at a 36x FY16F P/E, higher than its state-backed peers’ average 30x, as its low gearing of 9% post consolidation places it in a prime position to acquire earnings-accretive WWT assets for longer-term growth." Photo: Company

OSK-DMG: "We value HanKore at a 36x FY16F P/E, higher than its state-backed peers’ average 30x, as its low gearing of 9% post consolidation places it in a prime position to acquire earnings-accretive WWT assets for longer-term growth." Photo: Company Merger lifts overhang; combined company to reap advantages and seek M&A-driven growth ahead. The transaction will boost HanKore’s waste water treatment (WWT) design capacity to 3.6m tonnes/day while the share issuance will lower the combined entity’s gearing to less than 9%. This may effectively give the group room to gear up for c. CNY2.6bn of funds (assume 40% gearing) for M&As that the company has intently expressed as its growth strategy in a consolidating WWT environment.

This could potentially add 1.0m tonnes/day design capacity to its portfolio, assuming transaction prices of c. CNY2,500/tonne.

Maintain BUY, TP changed to SGD1.50. Based on our proforma estimates, we forecast the combined entity to make CNY0.205 EPS in FY16F (FYE June) based on its existing assets, without taking into account any M&A, owing to the lack of information. We value HanKore at a 36x FY16F P/E, higher than its state-backed peers’ average 30x, as its low gearing of 9% post consolidation places it in a prime position to acquire earnings-accretive WWT assets for longer-term growth.

Recent story: Maybank KE: Bet on China's water sector (HANKORE, SIIC ENVIRONMENT)

CIMB starts coverage of China Merchants Holdings Pacific with $1.06 target

Analysts: Roy Chen & William Tng, CFA

We expect China Merchants Holdings Pacific's (CMH) strategic expansion to be firmly supported by its very cheap financing and the strong nationwide footprint of its parent, China Merchants Group (CMG). We expect China Merchants Holdings Pacific's (CMH) strategic expansion to be firmly supported by its very cheap financing and the strong nationwide footprint of its parent, China Merchants Group (CMG).

The company pays the highest dividend among its peers while having significant scope to further ramp up its investment returns.

The toll road operator’s recent success in exiting a nonperforming property development business has refreshed its outlook. While we expect strong expansion ahead through acquisitions, our current target price is conservatively based on the organic growth of its toll income.

We initiate coverage with an Add rating and a target price of S$1.06 based on CY14 residual income value.

A refreshed outlook: After successfully exiting a nonperforming property business in New Zealand, CMH has become a pure toll road-focused business. The toll road business rides on China’s new initiative to develop the Yangtze River economic belt.

CMH is expected to benefit from the expanding income from its toll assets in the region.

Strong parentage firmly supports future expansion: CMG is one of the largest SOEs directly under China’s State Council.

Being CMG’s largest listed vehicle in terms of stake holding (82%), CMH is a primary beneficiary of the former's wide footprint across China.

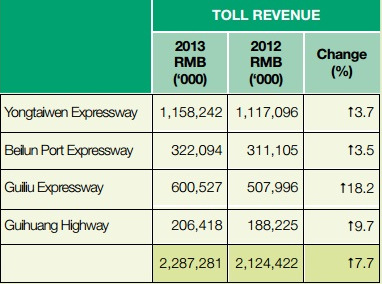

Through its toll roads arm, Huajian Highway Investment, CMG holds an investment portfolio comprising toll roads, bridges and tunnels with an aggregate length of approximately 6,700 km in 14 provinces and two municipalities. This provides CMH with plenty of options to expand its toll asset base through acquisitions.

Optimally geared, CMH is worth S$1.52: CMH has the lowest borrowing cost at c.3% (peers' at 4.5-6.0%).

This gives it unparalleled advantage to potentially ramp up its toll asset investment returns. Its net gearing level of c.21% is very docile compared to the maximum 60% that management is comfortable with. In our opinion, CMH could further ramp up its ROE from the current decent level of 12% to 16% through leveraged acquisitions of toll assets, as what it has been doing over the past few years.

With such an improved ROE, CMH would be worth S$1.52. A 7 Scts DPS (7.5% yield) is sustainable in the long term.

|