Yuanta initiates on CHINA HYPERMARKETS, positive view on industry, consolidation key

Top recommendations:

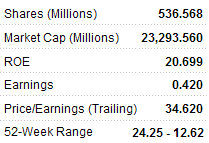

Wumart Stores (HK: 8277); BUY; target price: 19.9 hkd

Yuanta says it likes Wumart -- which operates convenience stores, supermarkets and hypermarkets in northern China -- due to its operating efficiency and believes the company is well-positioned for future expansion, with the brokerage forecasting earnings CAGR of 23% for 2010-12.

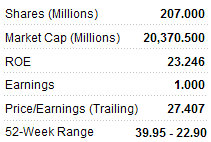

Lianhua (HK: 980); HOLD; target price: 35.0 hkd

Although Lianhua offers investors exposure to the growth potential of China’s retail spending, Yuanta says it has a conservative outlook on its lack of operational leverage and consolidation synergy.

“Industry consolidation should continue, which we believe will lead to a sector re-rating. We are positive on the outlook for hypermarkets, but we believe supermarket growth could be hampered by fierce competition,” the brokerage added.

Initiating coverage of China’s hypermarket industry: Yuanta says it holds a “positive view” on the industry and anticipates key players will continue to expand both organically and through M&As over the next few years.

“We also believe the nature of the business offers a defensive buffer, given increasing inflation concerns in China.”

Steady industry growth ahead: Yuanta forecasts retail sales CAGR of 10% from 2010-13 will continue to outpace consumer expenditure, which should see a 9% CAGR over the same period, on the back of government policy support and changes to consumer behavior, in addition to macroeconomic tailwinds.

Value lies in consolidation: “We anticipate consolidation in the industry will continue, and based on historical trends, M&As should lead to a sector re-rating. We expect national players such as CRE (HK: 291; not rated) and RT-Mart (non-listed) to take the lead, with local players in prime locations likely M&A targets.”

Margin expansion story: The brokerage added that leading companies should see margin expansion on the back of 1) product mix improvements; and 2) consolidation and expansion, which should lead to economies of scale.

See also: FIRST CAPITAMALLS, NOW PRC PEERS? 10 A-Shr Developers Also Eyeing HK

UOB says four HK-listed firms major beneficiaries of supportive TEXTILE policies from Beijing

CNBM (HK: 3323), Sinoma (HK: 1893), Dongyue (HK: 189) and Lumena (HK: 67) are all well-positioned to thrive as the market is expected to reach one trln yuan by 2015.

The China Textile Industry Association (CTIA) is working with relevant government departments jointly drafting the country’s "Twelfth Five-year Plan” for the textile industry. The plan, to be introduced later this year, will mark a potential market size of one trillion yuan by 2015.

UOB Kay Hian said that to guide the healthy development of the industry, CTIA has clearly started the key long term development areas by to be in place by 2020, including filtration, geotextile, medical, agricultural and composite material products, all key areas of textile producers.

Catalysts include: Supportive government policies for textiles and ongoing energy-saving and environmentally friendly policies.

The brokerage added that Dongyue is one of the major producers of polytetrafluoroethene (PTFE) in China, while Lumena is the only producer of polyphenylene sulfide (PPS) in China.

“We maintain the view that CNBM, Sinoma, Dongyue and Lumena are the key beneficiaries of the China’s continuous policies on energy saving and environmentally friendly policies.”

CNBM (HK: 3323; BUY), Current price/target price: HK$15.22/16.00, Market Cap: US$5.8 bln, 52-week Hi/Lo: HK$16.70/5.44

Sinoma (HK: 1893: BUY), Current price/target price: HK$7.12/9.50, Market Cap: US$1.1 bln, 52-week Hi/Lo: HK$8.47/3.87

Dongyue (HK: 189; not rated), Current price/target price: HK$9.00/N.R., Market Cap: US$2.5 bln, 52-week Hi/Lo: HK$9.54/1.42

Lumena (HK: 67; not rated), Current price/target price: HK$3.69/N.R., Market Cap: US$2.9 bln, 52-week Hi/Lo: HK$4.52/1.68

See also: CHINA GAOXIAN, FORELAND, CHINA FIBRETECH, TAISAN: What CIMB Found Out...