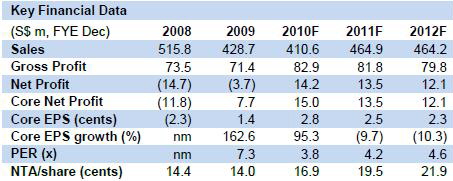

SIAS Research says ‘increase exposure’ to Roxy-Pacific

Update: Roxy-Pacific Holdings announced its financial year 2010 second quarter results on 4th August 2010.

We maintain our Increase Exposure rating on the counter, based on an intrinsic value of S$0.450 - representing an upside of 42.9% over its last traded price of S$0.315.

Key Developments:

• The Company has outperformed our earlier expectations. Total revenue and net profit after tax for 2Q2010 were recorded at S$55.4m and S$12.9m respectively – representing impressive YoY increases of 27% (revenue) and 37% (NPAT).

On a QoQ basis, Roxy also improved on their bottom line performance by growing NPAT 43% over 1Q2010.

• Roxy’s robust quarterly performance was achieved on the back of a 25% increase in revenue from its Property Development segment as well as a substantial 145% uptick in top line from their Property Investment segment.

Roxy’s Hotel Ownership segment also reported a 27% increase in revenue for the last quarter.

• We like Roxy’s robust balance sheet position as total assets expanded 8% from S$425.5m as at end-2009 to S$461.4m at 30th June 2010. Over the same period, the Company’s total debt figure also grew from S$250.4m to S$270.1m. That said, both the Company’s valuation metrics - NAV and RNAV - picked up in the second quarter of 2010.

Outlook:

With the Singapore government expecting economic growth of 13% to 15% in 2010, we believe that Roxy will benefit from a robust Singapore property and tourism market.

In addition, the Company has a substantial holding of unrecognized pre-sale revenue to be accounted for going forward. At its current price, we believe that Roxy is still significantly undervalued.

KEVIN SCULLY: Innotek delivers a good set of Q2-2010 results with net profit higher by 26% to S$6.59mn....six month net profit is up 143.3% to S$10.41mn

Innotek delivered a good set of Q2-2010 results with revenue higher by 19% to S$110.5mn and net profit higher by 26% to S$6.25mn. For the half year, to June 30, 2010, Innotek saw revenue rise 16% to S$204.1mn while net profit was higher by 143.4% to S$10.4mn.

The strong Q1 and Q2 2010 was expected and highlighted by management at their FY2009 briefing.

The results on an annualised basis are likely to come in 20-30% higher than my initial forecasts of S$15mn for 2010.

The stock remains in my Stock Picks for both the growth and dividend portfolios and remains about 50-60% below my fair value.

Read more about my revised estimates and price target in My Stock Picks section. Investors should note that Innotek is not a trading stock....its meant to be held for the dividend yield and as they dont pay an interim dividend - investors have to wait till early 2011 for the dividend.

Key points to note:

a) the strong pace of recovery in Q1 and Q2 are not sustainable and business should return to more normal growth rates.

b) management are guiding that H2-2010 will be better than H2-2009. Innotek made S$5.18mn in H2-2009 - so we can expect similar profit levels into the second half of 2010.

c) Cash position remains strong with gross cash of S$98mn down from S$109mn but the value of treasury shares has also increased from $7.0mn to S$11.2mn

d) Receivables and payables have increased and match quite nicely.

e) EPS for the six months is S$0.04 compared to S$0.016 while NTA has remained flat at S$0.85.

Kevin Scully is the executive chairman of NRA Capital (www.nracapital.com)

NRA CAPITAL maintains ‘buy’ and 21-c fair value for ASTI

Analyst: Jacky Lee

Ahead of expectations. Despite 2Q10 sales coming in 18% below our expectation, ASTI has delivered 2Q10 net profits of $1.8m, in excess of our forecast of S$1.5m due to higher-than-expected margins expansion and interest and investment income. These however were slightly offset by higher-than expected operating cost.

♦ Sales declined 7% yoy to S$95.6m in 2Q10 due to softer demand for its distribution and services business (-28% yoy) mainly as a result of the deferment of the telecommunication infrastructure projects in China. While business from equipment and manufacturing continued to show strong recovery, sales of backend equipment solutions & technologies (BEST) increased 87% yoy but was flat qoq to form 37% of total sales.

♦ Gross margins expanded by 7.1% pts yoy to 22% in 2Q10, due mainly to higher contribution from BEST division, which generated higher margins. However, EBITDA margins only increased by 1% pt yoy to 4.8% due mainly to the surge in administrative expenses as we believe the increase was partially due to an out-of-court settlement cost. Including a S$0.3m forex loss, higher interest income and lower financial expenses, net profit turned around from S$1.7m loss to S$1.8m profit.

♦ Improving Balance sheet. Despite the fact that its cash conversion cycle increased by 16 days to 135 days as compared to the previous quarter, ASTI generated S$11.3m positive cash flow due mainly to an improvement in working capital. As a result, the group ended the quarter with an 8% net gearing, down significant from 22% qoq.

♦ Near term outlook remain robust. According to the June report of the SEMI, semiconductor equipment sales are expected to grow by 104% in year 2010 and a further 9% increase in 2011. These past 12 consecutive months of Book-to-Bill ratios over 1, indicate the consistent customer demand and the group is working hard to fulfill orders (the longer cycle in the past 15 years was in year 1999 and 2000 after the Asian financial crisis, when there was 23 consecutive months of Book-to-Bill ratios over 1). Management expects the BEST business to continue to be stable in the second half.

♦ Maintain Buy recommendation. We have fine-tuned our FY10-12 profit forecasts by 2 to -2% to factor lower sales but higher margins. We believe the group still has room to improve its earnings. Maintain Buy and fair value remains S$0.21, still based on 1.2x