A reader contributed this article

|

A compelling opportunity can be found in the "sum-of-the-parts" discount of Tuan Sing Holdings. A recent Tuan Sing corporate update reveals a massive valuation gap. |

GulTech Net Profit (100% basis)

|

Year |

Net Profit |

Revenue |

YoY Change |

|

FY2024 |

59,032 |

430,495 |

-17% |

|

FY2023 |

71,181 |

506,606 |

— |

Source: annual report

Tuan Sing Group

|

Year |

Profit Attributable to Shareholders |

|

FY2024 |

2,344 |

|

FY2023 |

4,836 |

Understanding Tuan Sing

To appreciate the GulTech story, one must first look at the conglomerate that holds it.

Tuan Sing Holdings is no longer just a "property player"; it is a diversified regional investment holding company with operations across four pillars:

| • Real Estate Investment & Development: The bedrock of the company, featuring premium Singapore assets like 18 Robinson and Link@896, alongside a massive township project, Opus Bay in Batam. • Hospitality: A growing segment including the Grand Hyatt Melbourne and the newly acquired Fraser Residence River Promenade in Singapore. • Industrial & Other Investments: This is where GulTech (44.5% stake) resides. For years, it was viewed as a non-core legacy holding, but today it has become the group's hidden gem. |

GulTech: Prepping for IPO

Founded in 1988, it was actually listed on the SGX Mainboard until 2013, when Tuan Sing and its partners took it private.

In 2021, Tuan Sing sold a 13% stake to high-profile Chinese private equity firms (Yonghua Capital and Wens Capital) at a valuation of ~S$685 million.

This was a clear signal: GulTech was being groomed for a re-listing.

While a China IPO in 2023/2024 was assessed to be not favourable, the business has only grown stronger since.

Assuming GulTech generates annual net profit of approximately S$60–70m (does not factor in future growth yet) and is valued at 25× earnings at IPO, the implied equity value would be around S$1.5–1.75bn.

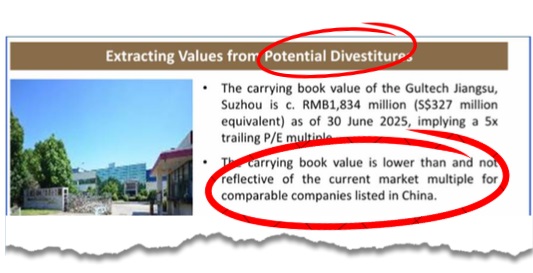

Tuan Sing's 44.5% stake would therefore be worth roughly S$670–780m, compared with the current carrying value of about S$327m.

This implies a revaluation gain of approximately S$340–450m at the associate level.

Spread across Tuan Sing's 1.25bn shares, this translates into an estimated NAV uplift of about 27–36 cents per share, which would be highly material relative to the current share price and highlights the significance of GulTech as a potential value-unlocking catalyst.

What GulTech Actually Does

The global Printed Circuit Board market has been in a solid recovery and growth phase since late 2024, accelerating in 2025 and carrying strong momentum into 2026 — largely thanks to the AI boom, EV/automotive electronics, and 5G/infrastructure demand.

GulTech is a top-tier manufacturer of printed circuit boards — the fundamental "nerve system" of modern electronics.

They specialize in high-reliability boards for:

-

Automotive: Engine controls and telematics.

-

Data Storage: SSDs and networking modules.

-

Healthcare: Infusion pumps and glucose monitors.

This, in turn, supports demand for enterprise-grade storage hardware such as SSDs and storage systems, which rely on more complex and reliable printed circuit boards.

GulTech's exposure to data-storage and infrastructure-related printed circuit boards positions it to benefit from this trend, helping to underpin more stable and resilient earnings over time, even if growth is gradual rather than abrupt.

This translates into a potential NAV uplift of S$0.27–0.36 per share.

|

|||||||||||||||

See 2022 story: TUAN SING: Spin-off to crystallise hidden value