See its dividend track record:

• Analysts have recognized the potential of the stock. They turned even more bullish after a visit to Food Empire's operations in Vietnam last week. • See excerpts of 3 reports below ... |

Excerpts from UOB KH report

Analysts: John Cheong & Heidi Mo

Site Visit In Vietnam Reinforces Our Positive View; Raise Target Price By 10%

|

• Site visit highlights significant improvement vs two years ago.

Food Empire Holdings (FEH) hosted a site visit to its Vietnam operations on 10-11 Sep 25, showcasing the scale-up of its local manufacturing facilities and distribution network. |

||||

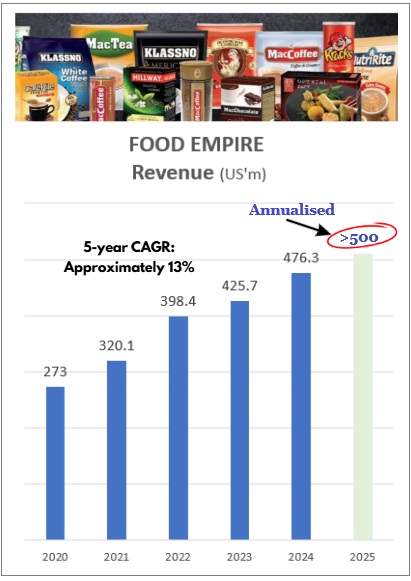

• Strong execution evident in market share gains and revenue growth. MacCoffee, FEH’s flagship coffee brand in Vietnam, increased its market share by 2ppt to 15% in 2024.

Revenue from Vietnam surged >30% yoy to US$76m, more than 3x the industry growth rate.

This stems from FEH’s ability to localise its product range and leverage marketing initiatives that resonate with traditional retail channels, where the bulk of Vietnamese consumers still shop.

"New products such as ready-to-drink (RTD) CaféPHỐ iced milk coffee have been well received, while its instant bubble tea, launched two years ago, continues to gain traction as a niche category." -- UOB KH |

• Expect above-industry growth via regular new product launches and unique marketing initiatives. FEH Vietnam is on track to achieve another record year with >30% revenue growth to US$100m in 2025.

Growth will be supported by two upcoming RTD launches in 2026, continued innovation across instant beverages, and a deepened presence in traditional retail channels.

With the RTD beverage market in Vietnam (around US$5b) about 10x the instant beverage segment (around US$500m), FEH has significant headroom to sustain above-industry growth.

Valuation/Recommendation

• Maintain BUY with a 10% higher PE-based target price of S$3.00 (S$2.73 previously), pegged to a higher 18.7x 2026F PE (17x 2026F PE previously), or 1.5SD above FEH’s long-term mean.

At 16.4x 2026F PE, FEH still trades at a deep 34% discount to regional peers’ average of 24.8x.

For UOB KH report, click here.  Sudeep Nair has been CEO since 2012 while Executive Chairman Tan Wang Cheow is the founder of the Group and took the company public in 2000.

Sudeep Nair has been CEO since 2012 while Executive Chairman Tan Wang Cheow is the founder of the Group and took the company public in 2000.

| DBS Research says ... |

FEH hosted a two-day analyst visit to Ho Chi Minh City, which included a factory tour, store checks across traditional trade outlets, and meetings with the local management team.

We identified three key drivers of FEH’s success in Vietnam.

° First, a culture that rewards innovation, which has led to tangible efficiency gains at the factory level, through multiple process improvements.

° Second, the company directly employs a large and growing sales force, enabling strong relationships with traditional trade channels. FEH has also introduced customer acquisition representatives focused on product trials and increasing sales per outlet.

° Third, strong brand equity built on taste and brand awareness translates to prominent in-store visibility for CaféPHỐ.

Despite per-serving prices that are about 41% higher than the local G7 competitor brand, CaféPHỐ brand continues to sustain volume growth.

For DBS report, click here.

|

Full Maybank report here.