| If you’re keeping an eye on smart investors, AGT Partners should be on your radar. Its value-focused fund recently made headlines by becoming a substantial shareholder in ISOTeam—a Singapore-based specialist in building maintenance and estate upgrading that will soon launch drones that can paint the facades of buildings.  ISOTeam's adoption of AI-powered painting drones is expected to be a game-changer for Singapore’s construction and estate upgrading sector, slashing operating costs. ISOTeam's adoption of AI-powered painting drones is expected to be a game-changer for Singapore’s construction and estate upgrading sector, slashing operating costs. AGT's bet is not small. AGT's bet is not small. Via the Ginko-AGT Global Growth Fund, AGT holds 37,076,900 shares (5.24% stake) valued at around S$3.7 million currently. This move, following bets on undervalued firms like Dyna-Mac, Beng Kuang Marine and Oiltek which made strong gains, underscores AGT's knack at identifying cyclical recovery plays. |

The value-oriented fund delivered strong results in the first half of 2025: net returns of 26.3% for Class A shares and 33.7% for Class B, according to its website.

AGT's success stems from spotting multi-baggers and holding them for the long-term like Apple, TSMC, Tencent and homegrown Sheng Siong.

| "We currently own a portfolio of large, high-quality businesses with strong returns on capital, growing earnings power, and competent management that prioritizes minority shareholders' interests. These companies have sustainable competitive advantages, long track records, and entrenched industry positions, making their futures bright over the long term. "We intend to hold most of these investments forever, using periodic share price weaknesses as opportunities to add. Examples include Apple, BYD, KKR, Sheng Siong, Tencent and TSMC, among others." -- AGT shareholder letter 2Q2025 |

AGT, in its shareholder letter post-2Q2025, says it also owns promising smaller companies with interesting near-term prospects.

"These companies are often neglected and unloved by the broader investment community, resulting in possible undervaluation. While their 10-year prospects may be uncertain to us, a sufficiently high level of margin of safety can make them quite attractive investments."

It went on to describe 4 of them, very briefly:

| "We have recently invested in a major Hong Kong commercial landlord, a Malaysian offshore supply vessel owner, a Malaysian department store chain, and a Singaporean construction company. Our purchases were made at attractive valuations, with the Hong Kong landlord trading at 0.35x price-to-book and the others at 3-5x price-to-earnings multiples." |

Who might these be? Forum chat at Valuebuddies.com speculates on a few names.

Hong Kong Land is the HK commercial landlord, agree ghchua and weijian.

Parkson Retail Asia is the Malaysian department store, says ghchua but weijian doubts it as Parkson's "own retail ops and that of its tenants are both losing sales fast on a mid/high single digits YoY and I can't see anything good coming out of department stores in this part of the world."

|

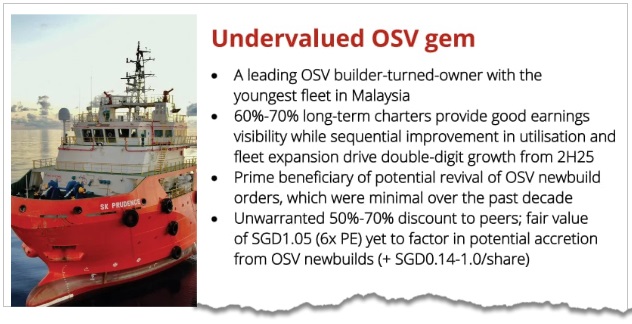

When it comes to the Malaysian OSV (offshore support vessels) owner, Singapore-listed Nam Cheong Limited is the guess of ghchua.

|

As for the Singaporean construction pick, weijian reckons it is OKP Holdings while ghchua thinks it is ISOTeam.

Well, we think it could also be Soilbuild Construction, which had an orderbook of $1.21 billion as of May 2025.

Soilbuild traded at less than ~5x P/E when the stock was below 85 cents in the several months prior to July. It started surging from July to $1.54 recently.

Bottom Line:

AGT Partners has been tracking down value plays most investors overlook.

Their willingness to bet on such stocks and wait for recovery has been paying off—proving that sometimes, the best investments are hiding in plain sight.