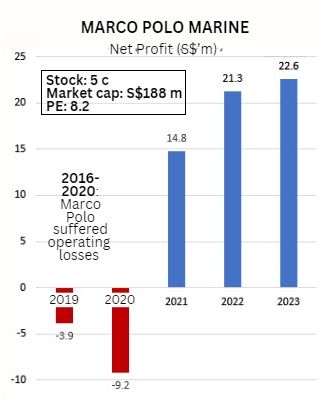

| • Marine-related companies are enjoying pretty good times, with three being highlighted in UOB Kay Hian's recent report Offshore Marine – Singapore 2024, Outlook Remains Bright. • One of them, Marco Polo Marine, has just got a nice upgrade to its stock price target. And why not when it had just reported a S$23 million net profit (+5.8% y-o-y) for FY 23 (ended 30 Sept). Its adjusted profit, excluding one-offs, was even better at S$25 million (+83% y-o-y). Plus it declared a dividend, a small one, its first in nearly 10 years. • Its performance in recent years is the stuff of a good comeback story. 5 years of bleeding and huge debts. White knights riding to its rescue. Then a multi-year rise in profit on industry tailwinds.  • Another stock loved by UOB KH is Seatrium, formed from the merger in 2023 of Sembcorp Marine and Keppel Offshore & Marine. Well, will it prove to be a comeback story as well? The merged entity is expected to report losses this year, its third successive year of losses. • In contrast, Yangzijiang Shipbuilding has been a relatively steady performer. It too gets a "buy" rating. Read more below about the bad kid made good -- Marco Polo. |

UOB KH analyst: Adrian Loh

Marco Polo Marine (MPM SP, BUY, Target: $0.066)

• Results well above expectations. In late-Oct 23, MPM reported FY23 core earnings of S$25m (+83% yoy), 50% higher than our estimate of S$16m due to its gross margin expanding by 4ppt as a result of higher utilisation rates and favourable charter rates for offshore supply vessels (OSVs).  From a low of 1 cent in 2020, the stock has touched 5 cents now. Revenue from its ship chartering and shipyards segments increased by 47% and 48% yoy respectively due to higher average utilisation and charter rates for its fleet of OSVs, higher contract values for repair projects and the commencement of new ship-building projects.

From a low of 1 cent in 2020, the stock has touched 5 cents now. Revenue from its ship chartering and shipyards segments increased by 47% and 48% yoy respectively due to higher average utilisation and charter rates for its fleet of OSVs, higher contract values for repair projects and the commencement of new ship-building projects.

• First DPS since 2012. Reflecting its confidence, the company announced its first DPS since 2012 of S$0.001/share.

This is supported by its strong net cash position which increased by 21% yoy to S$61m (around 30% of market cap).

• Bullish outlook. MPM forecasts that its OSV utilisation rate will remain relatively robust amid positive demand-supply dynamics.

In addition, OSV charter rates are expected to appreciate in the coming year.

Adrian Loh, analyst• After its results, we raise our target price by 10% to S$0.066 due to earnings upgrades. Adrian Loh, analyst• After its results, we raise our target price by 10% to S$0.066 due to earnings upgrades.Maintain BUY. We value MPM at 1.3x FY24F P/B, in line with +2SD to its historical five-year average on the back of higher charter and utilisation rates. |