• Analysts and industry insiders are highlighting that the semiconductory industry is poised for recovery in 2024 and beyond. This comes after a year-long decline due to factors including weak user demand and bloated inventory.   • With that positive industry backdrop, CGS-CIMB today put out its recommendations on semicon-related stocks to buy. Read on.... |

Excerpts of CGS-CIMB report

Analyst: William Tng, CFA

Semiconductor Sector to recover further in 2025F

Upgrade sector from Neutral to Overweight

William Tng, analystWe upgrade the semicon sector from Neutral previously to Overweight as we look towards FY25F prospects.

William Tng, analystWe upgrade the semicon sector from Neutral previously to Overweight as we look towards FY25F prospects.

In our view, suppliers supporting the semicon industry would continue to benefit from trade diversion into Malaysia, given the ongoing US-China geopolitical tensions.

In our view, the tech sector should also benefit from the semicon industry recovery, which is expected to gather strength in 2025F.

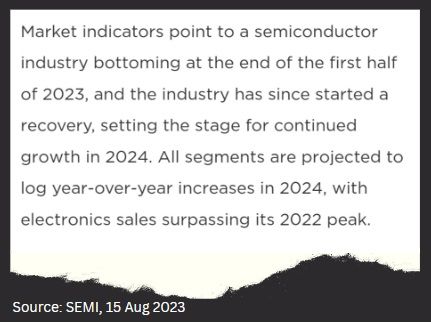

We note that industry forecaster IDC has called the bottom for the semicon industry on 14 Nov 2023 and projects a 20.2% yoy growth in global semicon revenue in 2024F.

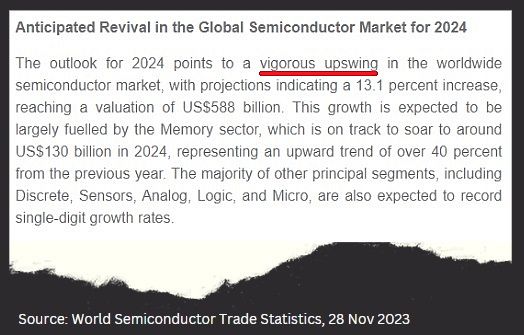

In its latest Semiconductor Market Forecast published on 28 Nov 2023, the World Semiconductor Trade Statistics (WSTS) projected that global semicon sales should fall 9.4% yoy to US$520bn in 2023F but recover 13.1% yoy to US$588bn in 2024F.

(Previously on 6 Jun 2023, WSTS projected that global semicon sales could fall 10.3% yoy in 2023F, followed by a 11.8% yoy increase in 2024F.) See page 10 for sector upside and downside risks.

| AEM (Add, TP: S$3.76) – 2H24F recovery; we expect stronger FY25F We use an unchanged FY25F 11.3x P/E multiple, its 5-year (FY19-23F) average, to value AEM, leading to a S$3.76 TP.

Downside risks include further pushback in the delivery timeline for customers’ testing equipment, weaker-than-expected recovery for the semiconductor industry and slower global economic growth, reducing customer demand for AEM’s contract manufacturing subsidiary. Potential re-rating catalysts include stronger-than expected orders from its major customer and a ramp-up in orders from new customers. |

||||

| Frencken (Add, TP: S$1.37) – diversified revenue base We reiterate our Add call on Frencken as it seems to be seeing a nascent recovery among its semicon customers, in our view, leading to a potential resumption in double-digit core EPS growth in FY24-25F.

Given the better-than-expected 3Q23 net profit due to stronger gross and net profit margins, we raise our gross profit margin assumption for FY23F by 0.03% pt, leading to a 6.9% increase in our FY23F EPS forecast. Our FY24-25F forecasts are unchanged. Potential re-rating catalysts: a less severe slowdown in its semicon business segment, better cost controls, and greater concessions from customers on cost pass-throughs. Downside risks: further cost escalations affecting its net profit negatively, and further weakening in demand for its semicon business segment. |

||||

| UMS (Add, TP: S$1.49) – earnings growth + dividend yield We reiterate Add on UMS, given its potential for EPS growth (average of 18.1% over FY24- 25F) and initial success in customer diversification.

Re-rating catalysts: securing more new customers and further orders from new customers for its new Penang plant, improving factory utilisation rates, return of orders for aircraft components benefitting its aerospace division, and better-than-expected cost management. Downside risks include negative impact from its key customer’s loss of sales to China, slower-than-expected rate of return of orders from customers, and UMS’s failure to secure enough orders for its Penang plant, or an increase in price competition as other suppliers in Penang also ramp up efforts to secure business with semicon companies that have recently expanded there. |

||||

Full report here.