In collaboration with SGX, DBS Vickers hosted its “Diamonds in the Rough” Corporate Day on 5 December 2016, where it showcased a group of companies in the small-mid cap space to a broad-based group of institutional investors. One of them was CNMC Goldmine Holdings.

CNMC Goldmine is principally engaged in the business of exploration, mining of gold and the processing of mined ores into gold ores. It is currently focused on the development of its flagship Sokor Gold Field Project, but has recently proposed the acquisition of a 51% stake in Pulai Mining Sdn. Bhd.

We opine that the group should trade at our 12-month TP of $0.65 (based on a blend of DCF and 14x FY17F PE), from just S$0.43 (or 9x FY17F PE) currently. |

||||

Salient Points from Management Presentation:-

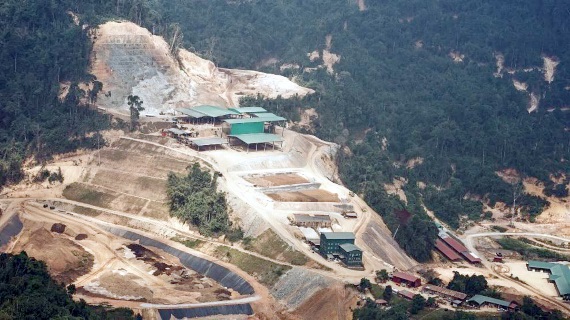

(1) Among lowest cost producers of gold globally. Having substantially reduced its all-in costs from over US$1,000/oz in 2Q13 to a record low of US$487/oz in 1Q16, CNMC currently ranks among the lowest-cost producers of gold on a global scale.  CNMC's goldmine in Kelantan. Photo: CompanyApart from expectations of a substantial but likely temporary spike in CNMC’s all-in costs in 4Q16 on the remaining payment of c.RM18m for its one-off mining licence extension fee, management remains confident of the group’s ability to keep costs low within the US$500- 700m/oz range ahead.,

CNMC's goldmine in Kelantan. Photo: CompanyApart from expectations of a substantial but likely temporary spike in CNMC’s all-in costs in 4Q16 on the remaining payment of c.RM18m for its one-off mining licence extension fee, management remains confident of the group’s ability to keep costs low within the US$500- 700m/oz range ahead.,

(2) Possible translation losses on a weaker Ringgit. With gold predominantly priced in USD and mining operations based in Malaysia (and thus incurred in ringgit), CNMC should theoretically benefit from operating leverage when the USD strengthens against the ringgit. However, as the group’s net cash of US$33.4m as at 3Q16 is mostly held in ringgit, CNMC would likely post a translation loss if the ringgit depreciates against the USD (CNMC’s reporting currency).

(3) Exposure to gold, with yield. While CNMC does not have a fixed dividend policy, the group has been paying a regular dividend since 2013 and is committed to paying dividends of up to 30% of net profit. Assuming the maintenance of a 30% dividend payout in FY17F, CNMC offers a unique exposure to gold with a prospective yield of >3%.

Questions Frequently Raised by Clients:-

(1) Success in delivering low all-in costs attributed to?  Chris Lim, CEO of CNMC Goldmine.

Chris Lim, CEO of CNMC Goldmine.

File photo.CNMC’s success in keeping all-in costs low can be largely attributed to:

(i) Open pit mining, which typically bears lower costs as opposed to other underground mining methods,

(ii) Weaker ringgit, in which the bulk of CNMC’s operating costs are denominated,

(iii) Internalisation of key gold mining processes,

(iv) Superior style of mineralisation at Sokor, which affects both production rates and leaching costs

(2) All-in sustaining costs vs all-in costs?

“All-in sustaining” cost represents the cash costs related to sustaining production over a given period and has historically been the predominant metric used in cash reporting, while "all-in” costs (which includes exploration costs) provide a more prudent and accurate representation of the true cost of producing gold over the mining lifecycle.

(3) Updates to proposed acquisition of Pulai Mining?

The group signed a conditional share subscription agreement to acquire a 51% stake in Pulai Mining Sdn Bhd on 25 Aug 2016 for a total consideration of RM13.8m. Management shared that it is currently undergoing due diligence and hopes to conclude the acquisition of the Pulai project soon.

| Key Risks to Watch Out for:- (1) Susceptibility to volatility in gold prices and mining conditions. CNMC does not engage in producer hedging and typically sells its gold ores at a slight premium to spot. We estimate that each US$10/oz decrease in gold prices could lower FY17F earnings by 1.7%. Gold output may also be hampered by bad weather. (2) No guarantees of commercially viable concentrations of gold for extraction and sale at Pulai. As a result, we have not factored in upside from Pulai in our valuations and forecasts. |

DBS Vickers' report on other companies which presented is here.