Nordic Group executive chairman Chang Yeh Hong fielding more questions after the 2Q16 results briefing.

Nordic Group executive chairman Chang Yeh Hong fielding more questions after the 2Q16 results briefing.

Photo by Leong Chan Teik

NORDIC GROUP delivered $3.1 million in net profit in 2Q this year, up 19% y-o-y, and highlighted that it is hungry for its next M&A action to grow its bottomline.

Against a depressed oil & gas sector backdrop, Nordic has done well to sustain its profitability and even growth.

Profit grew 34% in 1H2016 to $5.4 million, thanks largely to contributions by Austin Energy which was acquired in June 2015.

Notably, 1H16 net profit would have leapt 77%, excluding forex flutuations (mainy a decline in the USD versus SGD this year).

Austin Energy -- which provides insulation services to petrochemical majors in Jurong Island -- was not only the key contributor to the profit growth but also the expansion of Nordic's gross margin from 25.4% in 1H15 to a sterling 31.6% in 1H16.

| Nordic stock | 25.5 cents |

| 52-week range | 13.7-28 cents |

| PE (ttm) | 8.5 |

| Market cap | S$100.4 million |

| Shares outstanding | 393.6 million |

| Dividend yield (trailing) |

4.66% |

| 1H2016 net profit | S$5.37 m (+34%) |

| Source: Bloomberg |

Nordic has been on the prowl for another solid acquisition -- one that has strong cashflow, the nature of the business sits well among the existing businesses of Nordic, and it is not capex-intensive.

In the meantime, as Nordic's executive chairman Chang Yeh Hong impressed on the attendees at the recent 2Q results briefing, Nordic has been insulating itself against any fallout from depressed oil prices, which now is exemplified by the high-profile failure of Swiber Holdings.

An ex-banker who is only too familiar with certain implications of an industry slump, Mr Chang has directed Nordic's risk managment efforts in collecting its trade receivables, and is confident of having to report little or no impairment.

Only one business segment of Nordic is deemed to have some exposure, though that has shrunk significantly. This is the systems integration segment (which largely serves shipyards in China and Singapore) -- while Nordic's scaffolding and insulation business segments, which services the infrastructure of oil majors on Jurong Island, have rock-solid customers.

"We'll come out of this very well, compared to others because we have taken the necessary steps to avoid huge impairments," said Mr Chang. "And for the new projects we take on, we are more careful about who we do business with."  Nordic Flow Control CEO Dorcas Teo explaining how the company manages counter-party risks.

Nordic Flow Control CEO Dorcas Teo explaining how the company manages counter-party risks.

Photo by Leong Chan Teik.

But Nordic's orderbook has fallen from $39.2 million a year ago to $26.6 million as at end-June this year.

The orderbook does not include maintenance services by Nordic's scaffodling and insulation businesses, as they are contracted at unit rates and thus do not have contract values.

In steering away from the marine and oil & gas sector, the systems integration business has sought opportunities in "general industries," securing work at the Changi Airport and hospitals, for example.

| ♦ Good news: Share buyback, dividends, M&A | |

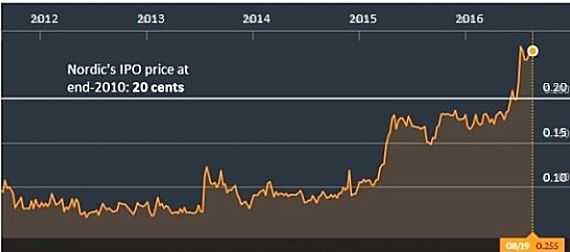

That has given Mr Chang an opportunity to point out that long-suffering investors who have held Nordic's shares since its IPO at the end of 2010 would have (finally) made a profit -- 50% or so. This includes the 3.37 cents a share paid as dividends since IPO. Last year, Nordic upped the attractiveness of its dividends by adopting a policy of paying 40% of its earnings as dividends.  After languishing for a few years at around 10 cents and lower, Nordic's share price started a steep ascent around the start of 2015. It closed at 25.5 cents last Friday. Chart: BloombergLong-time shareholders have now reaped the reward of holding Nordic shares through a long depressed period when Nordic's previously dominant business (systems integration) slid with the rapid decline of the global shipbuilding industry. After languishing for a few years at around 10 cents and lower, Nordic's share price started a steep ascent around the start of 2015. It closed at 25.5 cents last Friday. Chart: BloombergLong-time shareholders have now reaped the reward of holding Nordic shares through a long depressed period when Nordic's previously dominant business (systems integration) slid with the rapid decline of the global shipbuilding industry.Its recovery began with the acquisition of Multiheight Scaffolding in 2012 and was cemented by the acquisition of Austin Energy last year. Mr Chang signalled that it's imperative for Nordic to search for its next target in order to grow its bottomline: "It's a pillar of growth for us. In this climate, there are M&A targets. It's mainly a question of price." |

The Powerpoint slides used in the 2Q2016 results briefing are here.