Excerpts from analysts' report

HSBC Global Research analysts: Pratik Burman Ray, CFA, Kristy Lee and Utkarsh Rastogi

|

|

Dividend yield and spread suggests sector is attractive post sell-down: With a prospective dividend yield of 6.8% (vs. historical average: 5.9%) and a spread of 390bps over 10-year government bonds (vs. historical average: 360bps) – the highest seen in the past three-plus years – the sector looks attractive in our view. We are also comforted that 10- year government bond yields are already 2.9% (marginally higher than 15-year historic average) and our rates strategists are projecting only a marginal increase to 3.1% by 2Q2016.

Improved debt metrics have largely de-risked the sector: The sector is less dependent on short-term debt (c10% of total debt), and over the past 2 years, debt maturity profiles have been extended by 15% to 3.67 years, and proportion of floating rate debt reduced to 21% (from 25%). The majority of the sector remains Singapore-centric with debt largely SGD-denominated (or hedged back to SGD). The improved debt metrics have substantially de-risked the sector and along with it risks of a sharp spike in required yields and spreads.

Implied valuation of underlying assets, an equally relevant metric, makes our investment case stronger: S-REITs under our coverage are trading at RNAV discounts of 2-33% with steeper discounts for the more ‘economically-sensitive’ office and hospitality REITs, resulting in a large disconnect between implied valuation of REIT-held assets and recently transacted prices in the physical market.  While the growth outlook is lacklustre, we expect asset prices to remain mostly firm given investment demand, and thus see this disconnect as extreme.

While the growth outlook is lacklustre, we expect asset prices to remain mostly firm given investment demand, and thus see this disconnect as extreme.

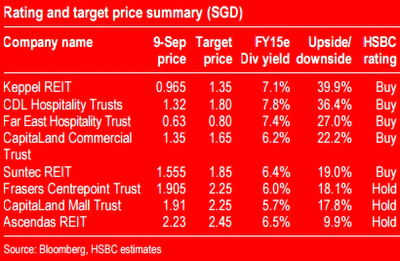

Preferred picks – CCT, FEHT, KREIT and CDREIT: Our preferred picks are in the office and hospitality sectors where dislocations are most acute. Our preferred picks offer the highest upside and are trading at yields of 6.2-7.8% and discounts to RNAV of 20-33% – levels not seen in over three years. Sector risks: higher-than-expected interest rates and managers overpaying for acquisitions.