Excerpts from analysts' report

DBS Vickers analysts: LIM Sue Lin & LING Lee Keng

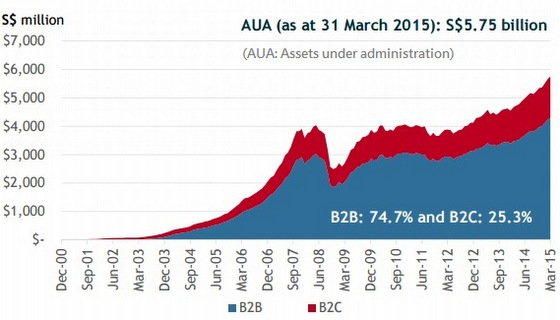

GROWING “FAST”-ER

|

|

New business initiatives to drive growth. iFAST received approval on 30 Apr 2015 from MAS to distribute bonds and ETFs in Singapore, which will allow iFAST to broaden the range of investment products that it can distribute. We believe this initiative would gradually improve iFAST’s AUA over time. Subject to regulatory approvals, iFAST is planning to launch an Online Discretionary Portfolio Management (Online DPMS) service, starting with Hong Kong, which would cater to DIY (doit-yourselves) investors who want additional help with asset allocation and automated rebalancing.

M&A is a wildcard. A wildcard to iFAST’s growth would be M&As. In addition, the successful execution of its operations in China would also support growth. Note that iFAST has earmarked about 70% of its IPO proceeds for M&A and expansion into the Chinese market.

Valuation: We use the Dividend Discount Model (DDM) as the valuation methodology for iFAST, given that it is a cash-led business, supplemented by a relatively high dividend payout. We arrive at our TP of S$1.73 (Prev S$1.60), after imputing a higher terminal growth rate of 4%, up from 2%, given its superior growth vs peers. iFAST currently trades at a cheaper 0.8x FY16F PE to growth ratio, compared to 3.6x for its overseas peers. New initiatives like the distribute of bonds and ETFs in Singapore should also boost growth in the longer term.

Key Risks to Our View: Highly regulated industry. The securities and financial services industry is highly regulated and iFAST is subject to a variety of laws and regulations across the regions it operates in. Security breaches is also a risk that could result in adverse publicity and damage to reputation.