Excerpts from analysts' reports

OSK-DMG initiates coverage of BreadTalk with a $2.00 target price

Analysts: James Koh & Juliana Cai

♦ Multiple dough for growth. BreadTalk Group (BreadTalk) operates a multi-format food and beverage (F&B) business, which has created various avenues of growth for the company. In our view, most of its brands are well-known and are market leaders in their respective categories. For example, the company’s new JV with Minor International (MINT TB, BUY, TP: THB40.00) would be a key driver for its expansion in Thailand, especially for its Din Tai Fung franchise.

OSK-DMG initiates coverage of BreadTalk with a $2.00 target price

Analysts: James Koh & Juliana Cai

|

|

♦ Multiple dough for growth. BreadTalk Group (BreadTalk) operates a multi-format food and beverage (F&B) business, which has created various avenues of growth for the company. In our view, most of its brands are well-known and are market leaders in their respective categories. For example, the company’s new JV with Minor International (MINT TB, BUY, TP: THB40.00) would be a key driver for its expansion in Thailand, especially for its Din Tai Fung franchise.

♦ Regional footprint appeals to potential acquirers. BreadTalk has more than 850 outlets under its umbrella. This includes more than 400 outlets in China, where it has presence in 57 cities. We believe this network is difficult to replicate and holds substantial appeal for potential acquirers. Minor International’s 11% investment in the company is a testament to that – and any further corporate action would be a bonus for BreadTalk shareholders.

Photo credit: http://gurkhason.wordpress.com

Photo credit: http://gurkhason.wordpress.com

Photo credit: http://gurkhason.wordpress.com♦ Substantial upside for margin improvements. Since listing in 2003, it has grown its number of outlets at an unprecedented pace to 850 from 28 in 11 years. We believe capex expenses and start-up costs have weighed down on profitability and a moderation of these expenses, as well as greater business scale in China, would present substantial upside for its net margin to improve from 2.5% currently.

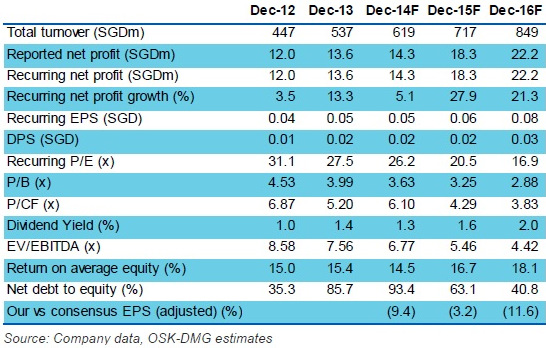

♦ Time to roll in the dough, initiate with BUY. Our SGD2.00 TP is based on a 7.5x FY15F EV/ EBITDA, a methodology we believe better reflects underlying cash earnings. Even then, this is almost a 50% discount to regional peers which are trading at an average of a 14.4x EV/EBITDA. Our SOP cross-check, which leans heavily on the replacement cost for its retail network, derives a value of SGD1.76/share.

Recent story: @ BreadTalk’s AGM: 12 Quick Things I Learned

Recent story: @ BreadTalk’s AGM: 12 Quick Things I Learned