This post on Global Premium Hotels ("GP") is in response to a reader's request.

Brief Introduction - GP Hotels is second-biggest budget hotel chain in Singapore.

It is a spin-off from Billionaire Koh Wee Meng's Fragrance Group (also listed and still owns a majority stake in GP Hotels).

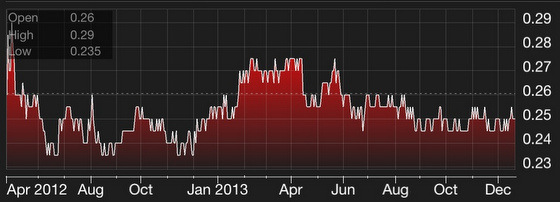

Since its listing in April 2012, GP Hotels' price has risen from the debut price of 27 cents to touch a high of 29 cents.

In 2013, GP Hotel's price hovered in a 24-27 cents range. Last Friday, it closed at 25.5 cents.

The stock has traded in a tight range since its IPO in April 2012. Chart: Bloomberg

The stock has traded in a tight range since its IPO in April 2012. Chart: BloombergGiven the strong Singapore dollar and mild fears of hotel rooms oversupply, is GP Hotels a good investment?

At 25.5 cents, GP Hotels has the following stock fundamentals:

(a) Fairly priced earnings: Trading at price-to-earnings (PE) of 14 times [annualized earnings per share (EPS) 1.8 cents]

(b) Cheaply priced assets: Trading at price-to-book (PB) of 64% [based on book value of 39.56 cents]

(c) Uncertain dividend: Dividend yield 4%. Decent but I understand there is no fixed dividend policy. The 2012 dividends are more due to promises made in the IPO prospectus, and there is no guarantee beyond that.

Dividend payout ratio 56% (meaning for every $1 earnings, GP Hotels distributed 56 cents as dividends).

Eddie Lim Chee Chong, 37, CEO of Global Premium Hotels. NextInsight file photo.Comfortable but if interest rates go up, the earnings can fluctuate significantly given the next point (d).

Eddie Lim Chee Chong, 37, CEO of Global Premium Hotels. NextInsight file photo.Comfortable but if interest rates go up, the earnings can fluctuate significantly given the next point (d). (d) Aggressive financing: GP Hotels has $479 mil of floating-rate term loans, of which $18 mil is due within a year.

Cash is $11 mil, so the deficit has to be made up by operational inflows, refinancing, capital raising.

Just to make a point how interest rate-sensitive GP Hotels' profits are -- from the FY12 Annual Report, a 50 basis point change in interest rates will lead to $1.8 mil change in profits (~10%)

(e) Insider buying: Of course, we can always make the argument that management knows best and likely more than outside passive minority investors (opmi), especially if they show their confidence in the company's outlook by putting their money where their mouths are.

Well, they have been buying. Since the release of Q3 results, billionaire Koh Wee Meng and wifey have gone on a buying spree...

Mr Koh & Ms Lim (each):

31 Oct - 1,495,000 at 25 cents

1 Nov - 505,000 at 25.16 cents

11 Nov - 1,000,000 at 25 cents

14 Nov - 1,200,000 at 25 cents

15 Nov - 650,000 at 25 cents

20 Nov - 150,000 at 25 cents

9 Dec - 2,000,000 at 25 cents

19 Dec - 450,000 at 25.5 cents

Total consideration each = $1.9 mil

A total of 14.9 mil shares were purchased from the open market, which represents 1.4% of total outstanding shares. Is GP Hotels' future really that bright?

Artist's impression of Parc Sovereign Trywhitt hotel.New hotel -- potential catalyst?

Artist's impression of Parc Sovereign Trywhitt hotel.New hotel -- potential catalyst?A new Parc Sovereign Hotel at Tyrwhitt Road is being developed and due to open by 1st half of 2014.

Again, like a number of their existing hotels, the location is decent (near Mustafa shopping center, Jalan Besar Stadium, and likely the future Bendemeer MRT station).

This 6-storey hotel (with swimming pool and F&B outlets) will add 270 rooms to the existing portfolio.

We should expect it to contribute positively to the group's results.

OCBC Investment Research believes that this new baby is going to add 17% to GP Hotels' bottom line.

Conclusion: I pass

If you want some exposure to the local economy via the mid-tier hotel industry, GP Hotels can be considered. But don't expect it to come with juicy dividends, and prepare yourself for a possible roller coaster ride due to its high leverage levels.

If you just want to ride on the MICE trend and you are looking for stability and dividends, Far East Hospitality Trust might be a better choice.

OCBC thinks GP Hotels is an asset play. In my view, with its high leverage levels and headwinds from rising labour costs and finance costs (thus potentially lower profits), I am inclined to be cautious even though management is very experienced in this business and likely able to tackle these issues.

The business will likely not fail, but that does not mean GP Hotels as an investment will not fail too. Passing over this one, what about you?